This week's deep dive examines the troubles facing Gemini, Genesis, and Digital Currency Group, with a particular focus on Gemini USD. In case you missed it, this week Kaiko Research released its Q4 report, covering the most important stories from last quarter.

The fall of the FTX and Alameda house of cards built atop a seemingly innocuous token – FTT – has raised skepticism about centralized exchanges and the tokens that they issue. Attention was first turned to Binance, BNB, and BUSD; as a result, BUSD’s market cap fell from $23.5bn to $16.5bn in just 90 days, though Binance has seemingly passed its stress test. Attention has now turned to Gemini, Genesis, and Digital Currency Group (DCG).

The new year opened on a combative note, with Gemini cofounder Cameron Winkelvoss tweeting an open letter to DCG CEO Barry Silbert, claiming that DCG owes Genesis (DCG’s subsidiary) $1.675bn, and Genesis owes Gemini $900mn that it took in from the Gemini Earn program. Genesis, and thus Gemini Earn, halted withdrawals on November 16, with Gemini claiming the halt was due to a liquidity issue at Genesis.

Given the troubles facing these parties, it is worth examining both Gemini and its stablecoin, GUSD, to consider its systemic importance and potential to depeg.

Gemini

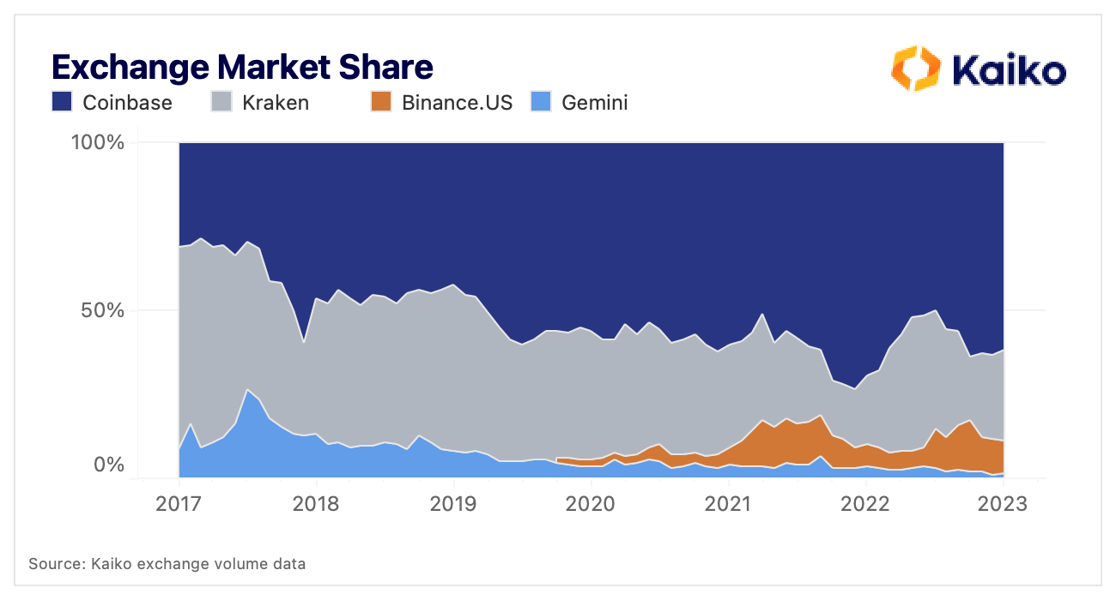

Gemini was once one of the largest U.S.-based exchanges, with volumes roughly on par with its main competitors: Kraken and Coinbase. For example, in July 2017, Gemini commanded 26% of volume amongst this group, compared to 44% for Kraken and 30% for Coinbase. From there began a steady downtrend in market share, exacerbated by new entrants like Binance.US. In December 2022, Gemini held just 1.2% of market share compared to its competitors while Binance.US claimed over 10%.

During the 2021 bull market, exchanges began to offer a wider range of products to retail users, the most problematic being high yields on token deposits, often advertised as “Earn”. As I wrote back in June, as “prices remain low, volumes decrease, hedge funds unwind, and fees compress, exchanges will be put to the test. Those that have enough volume and spent responsibly through the bull market will likely be able to weather the storm, while those that played fast and loose with risky staking products and investments may go under.”

Right now, it appears that Gemini’s immediate problems are isolated to its Earn program and its relationship with Genesis. GUSD was a focal point of the Earn program, with Gemini advertising 8% yields on the stablecoin: the highest of any token. 2022 drilled home the lesson that if yield looks too good to be true, it probably is. So let’s examine GUSD to see if there could be more problems lurking beneath the surface.

GUSD

GUSD is a USD stablecoin issued by Gemini that is 1:1 backed with cash deposits at banks (including Silvergate), money-market funds, and U.S. Treasury bills. The auditing firm BPM conducts monthly attestations regarding GUSD’s backing. Additionally, Gemini is regulated by the notoriously stringent New York Department of Financial Services (NYDFS) and GUSD is thus subject to specific NYDFS guidance on stablecoins that governs backing, redeemability, reserves, and attestations.

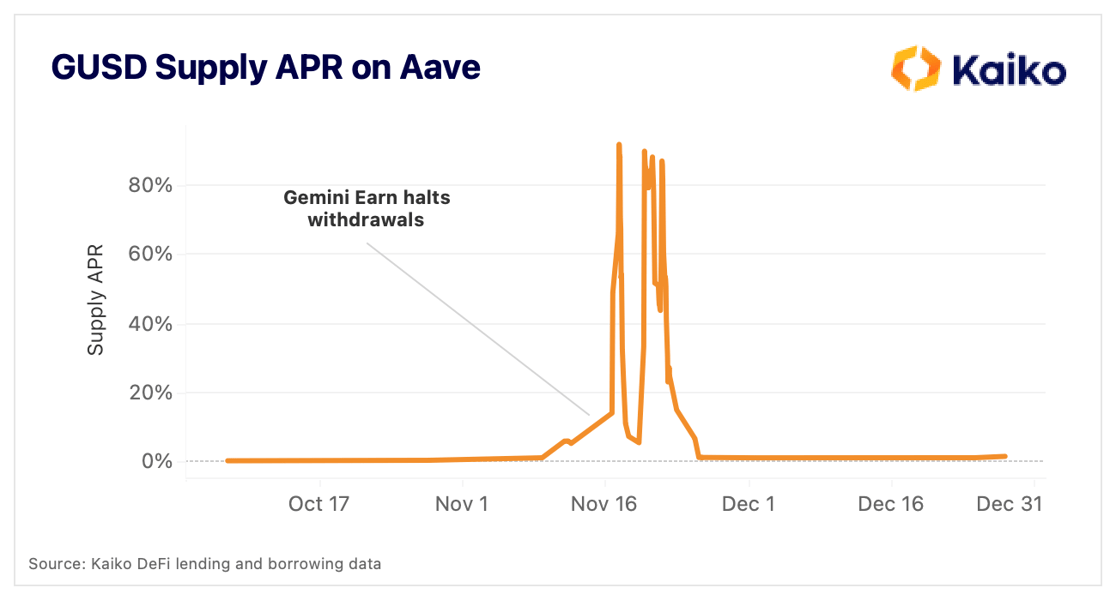

Despite these safeguards, GUSD was heavily shorted as Gemini halted withdrawals, as shown below by the GUSD supply APR on Aave nearly hitting 90% as users borrowed GUSD. (This mechanism is discussed in more detail in a previous Deep Dive.) Clearly the market interpreted Gemini’s troubles as a potential problem for GUSD, too.

Why would Gemini, or any exchange, go through the effort of issuing and maintaining backing for a stablecoin? Because the issuer can earn yield on the assets they hold that are backing the stablecoin; as of its last attestation, Gemini held $234mn of Treasury bills to back GUSD, along with $72mn in money-market funds and $293mn in cash deposits.

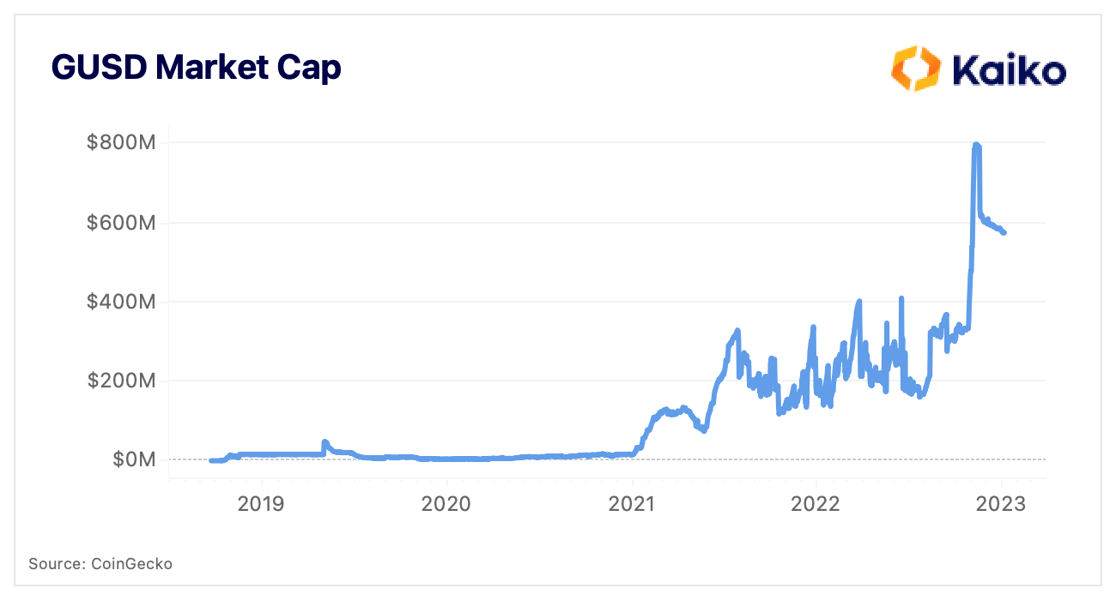

For nearly all of the latest bull run, GUSD’s market cap hovered around $200mn; in October it jumped to nearly $800mn because of a deal with MakerDAO, to be discussed below.

This all points to a relatively safe stablecoin, but let’s dig deeper into the data, beginning with centralized exchanges and then moving to DeFi.

Centralized Exchanges

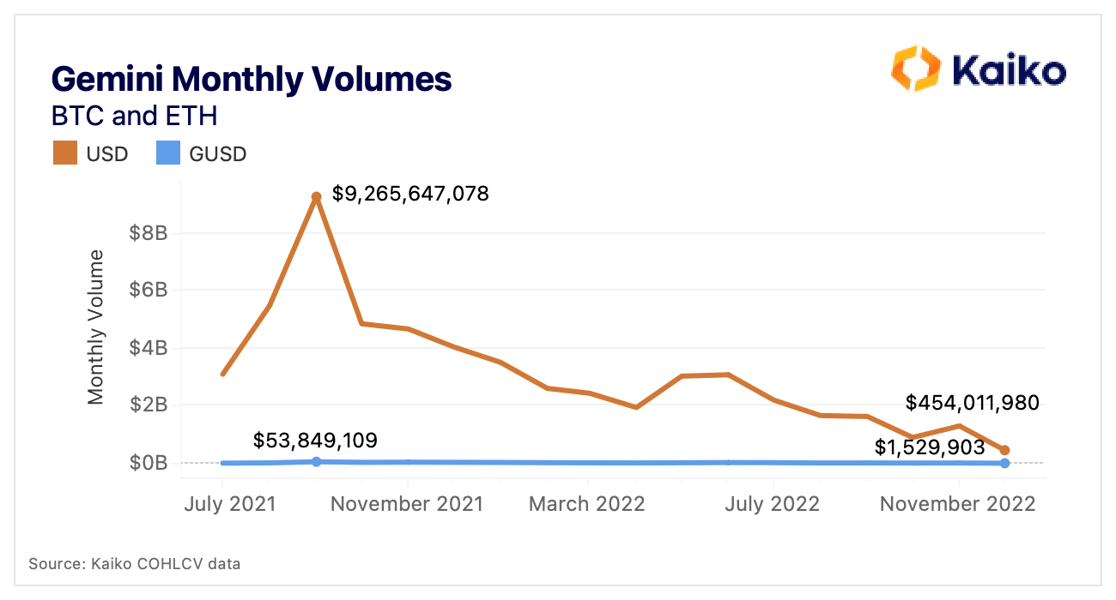

Because an exchange can earn revenue on the assets it holds to back its stablecoin, it follows that an exchange would want its stablecoin to grow as large as possible. One way to achieve this is to have it used in trading, as is the case with Binance’s BUSD. As discussed in our Q4 report, BUSD now holds a 38% market share of BTC and ETH trading on Binance relative to USDT. Additionally, spreads for USDT and BUSD pairs on Binance are nearly identical, suggesting that the exchange is engaging market makers to make BUSD trading more attractive. This is decidedly not the case on Gemini, where USD pairs of BTC and ETH regularly do 100-300x more volume than their GUSD equivalents.

There is no GUSD-USD pair on Gemini, instead users are able to directly redeem their stablecoin for USD. Elsewhere, there is extremely limited GUSD liquidity, with Coinbase the only major exchange to offer a GUSD-USD(T) pair.

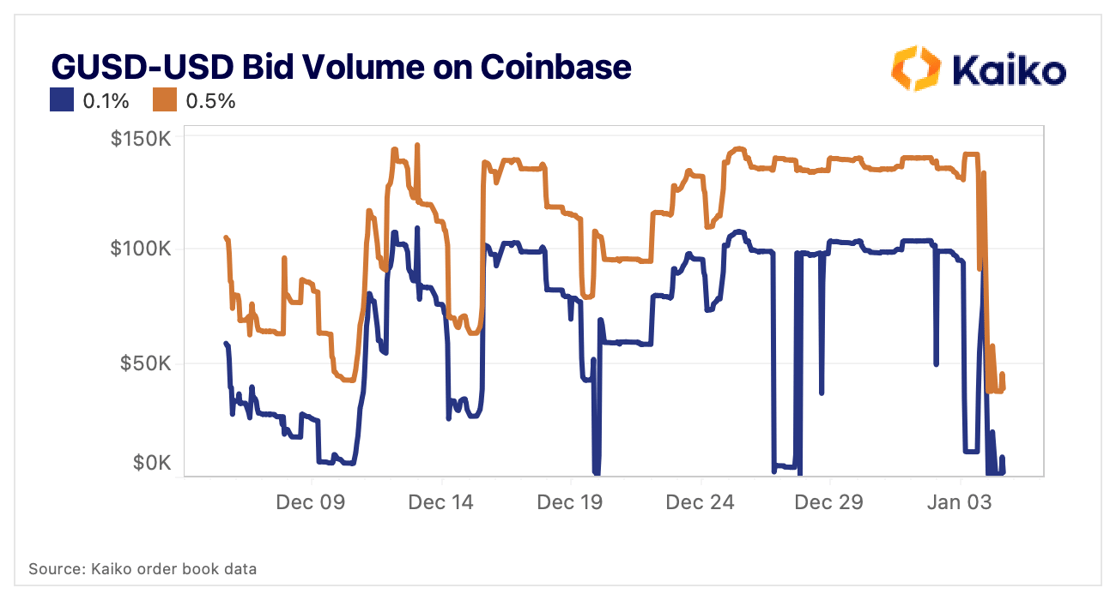

Similar to most stablecoin-stablecoin pairs, nearly all liquidity is in a tight range around the mid-price of $1. The above chart shows that the volume of bids within 0.1% of the mid-price has nearly hit 0 multiple times in the past month, and in the past couple days bid volume 0.5% from the mid-price has fallen from $140k to $40k.

Decentralized Exchanges

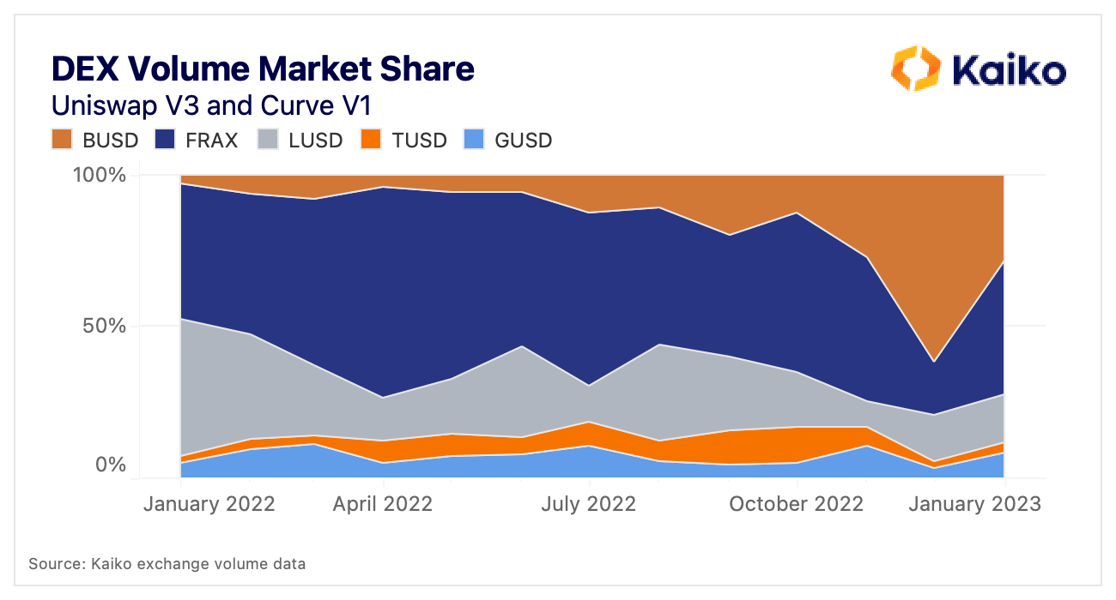

Given GUSD’s limited use on CEXs, it stands to reason that it might be more widely used in DeFi. This would be similar to USDC, whose trading volume on CEXs has fallen while its importance in DeFi has grown. However, GUSD is not heavily used in DeFi, with lower Uniswap volumes than LUSD, FRAX, and BUSD and comparable volumes to TUSD. (USDC has been excluded as its volumes are magnitudes larger than these five stablecoins'.)

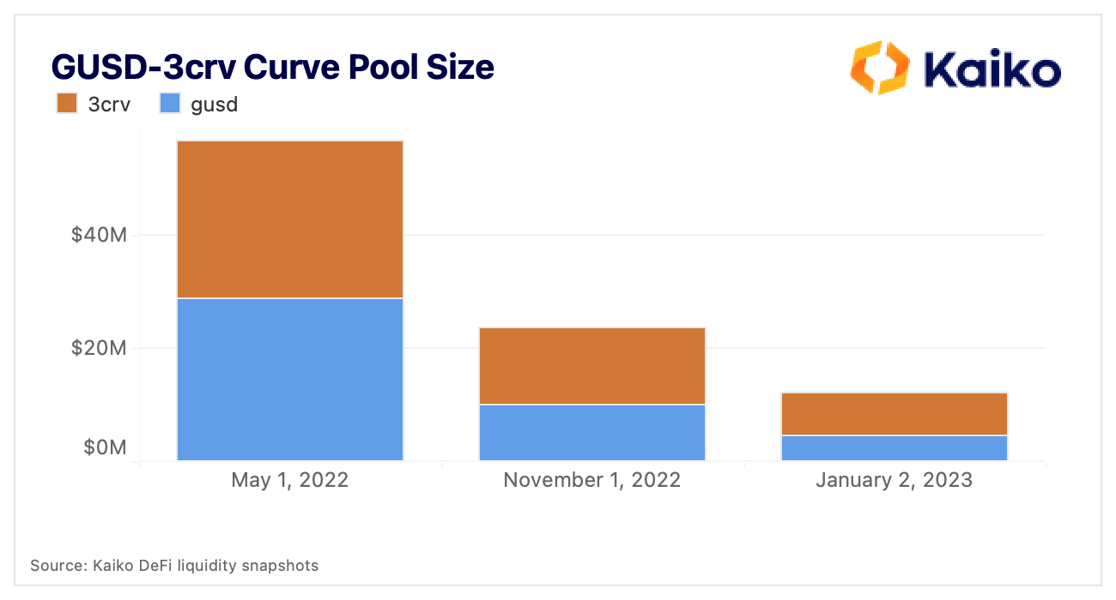

Looking at Curve, GUSD liquidity has shrunk significantly since the Terra crash, dropping from $30mn in May to $10mn in November to just over $4mn now. As discussed in our previous Deep Dive, Curve pools provide a useful barometer of stablecoin sentiment, and the makeup of the pool does not point to a flight from GUSD, which made up over 50% of the pool in May and now makes up just 32%.

If there were panic around GUSD, we would expect to see its share of the pool increase as users swapped out of GUSD for USDT, USDC, or DAI.

GUSD'S Use Case

Given that GUSD isn’t really used on centralized or decentralized exchanges, what is it used for? At the moment, its primary use case is in the MakerDAO Peg Stability Module (PSM), a reserve that helps the protocol maintain DAI’s USD peg. In his proposal to MakerDAO, Tyler Winkelvoss, cofounder of Gemini, stated that Gemini’s goal was to increase GUSD’s usage on chain. Gemini agreed to contribute “to MakerDAO a fixed rate of 1.25% (annualized rate, calculated and paid on a monthly basis) for any GUSD present in the PSM, as long as the average monthly balance on the last day of the month is over $100m GUSD.”

Currently, over 490mn GUSD is held in the PSM, which represents about 85% of GUSD’s market cap. Recent MakerDAO governance discussions have raised concerns about GUSD’s heavy reliance on the PSM and Gemini holding GUSD reserves at Silvergate, a crypto-focused bank that took a $718mn loss liquidatingits debt last quarter to cover $8.1bn in withdrawals. Its shares are down over 40% today.

Conclusion

Overall, there is little GUSD liquidity available on either centralized or decentralized exchanges and GUSD is only redeemable on Gemini. Despite some fears surrounding Gemini and GUSD, it has not lost its peg. The worst case scenario would involve troubles at Gemini that cause a delay in redemptions. Given the illiquidity of GUSD and the fear that this would generate, in this scenario it would not be surprising to see GUSD temporarily deviate from its peg and return once redemptions resume. But GUSD is small and not systemically important in centralized exchanges or DeFi; even a significant depegging would be unlikely to rattle DAI.

Unlike FTX/Alameda and FTT, GUSD doesn’t appear to be propping up any entity or pose any serious risk to Gemini’s solvency. Its growth has been slow and its acceptance into MakerDAO (and largest jump in market cap) came following a robust debate in one of DeFi’s most active DAOs.

On this note, MakerDAO will have to reassess whether the risk of holding GUSD in the PSM outweighs the benefits. From my perspective, holding GUSD is akin to holding GUSD’s underlying assets with additional risk related to Gemini. Given MakerDAO’s innovative investments in real world assets, it seems possible that the community may opt to move on from GUSD in favor of new pilot projects.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.