Bitcoin entered 2025 with strong momentum, extending the structural uptrend established in 2024, repeatedly achieving new highs. While the year has not been without setbacks, price action and market microstructure continue to point to a maturing asset class.

From J.P. Morgan to Vanguard, major incumbents have moved from skepticism to selective participation, reflecting changing liquidity conditions, declining volatility, and evolving demand from market participants. Throughout this debrief, we:

Analyze how banks have changed their strategies;

Explain the catalysts behind this change;

Observe the evolution of regulation.

Banks' Tone has Changed in Light of Bitcoin Maturation

Flows are no longer dominated by unknown, Satoshi-era holders, but increasingly driven by identifiable participants such as ETFs, asset managers, and corporate treasuries.

Throughout much of 2025, the market demonstrated its improved ability to absorb sustained distribution from large holders, while minimizing price impact. Even as whales reduced exposure, deeper order books and improved market depth allowed prices to remain resilient, underscoring how far execution conditions have progressed.

Namely, in October and November this resilience was meaningfully tested, ultimately pushing prices back below the $100k level. These events, however, did less to undermine the broader thesis than to highlight it. Bitcoin’s ability to withstand prolonged selling pressure before reacting to external shocks illustrates a market increasingly shaped by institutional liquidity, tighter spreads, and a more stable investor base. In this context, volatility compression is not an anomaly, but a signal of maturation, and a key reason why traditional institutions can no longer afford to stay on the sidelines.

Banks are Changing their Strategy

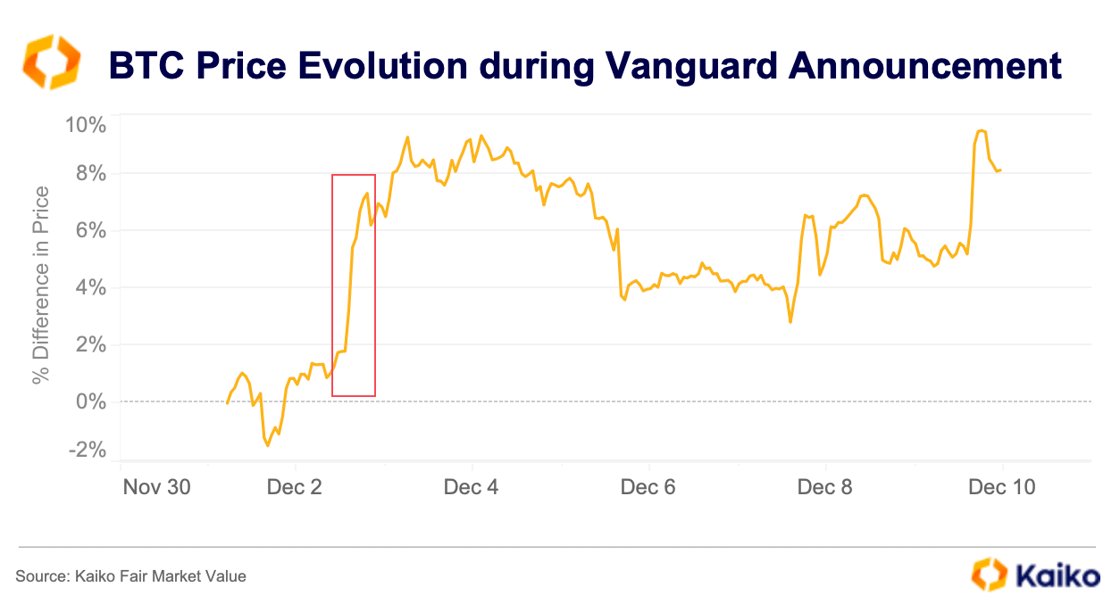

Vanguard's entry into the crypto industry in early December marks a new symbolic turning point for the institutional adoption of assets and products long considered marginal by large, traditional institutions. Vanguard, one of the world's largest asset managers, is now allowing trading on its platform of ETFs and mutual funds composed primarily of specific cryptocurrencies, including Bitcoin, ETH, XRP, and SOL.

This new offering marks a clear break with Vanguard's traditionally conservative, Bogle-inspired approach, which emphasizes steady, broadly diversified, and long-term investments, and a deep skepticism towards speculative and highly volatile assets. For Vanguard's loyal user base, the availability of cryptocurrency-related instruments like Bitcoin and ETH on the platform represents much more than a simple product range expansion. It reflects the growing integration of digital assets into the institutional toolkit and Vanguard's commitment to meeting the expectations of a new generation of investors, offering insights into long-term market and portfolio construction trends.

The price of BTC was also sensitive to Vanguard's announcement, as can be seen in the graph below.

Vanguard's case is not isolated, and we have witnessed in recent months, even years, a shift in mindset regarding the perception of the crypto industry and the new offerings created by traditional banks. One of the most striking examples of this change in opinion is undoubtedly that of Jamie Dimon, CEO of J.P. Morgan. After years of criticizing Bitcoin, comparing it to a "pet rock" and even calling it a "fraud" in 2017, Dimon has recently softened his stance. While he remains skeptical of Bitcoin as a currency or store of value, he now acknowledges that crypto, blockchain technology, and stablecoins are indeed "real", meaning they offer concrete applications and industrial value for finance.

For several years, J.P. Morgan has been actively investing in its own blockchain-based infrastructure, notably through Onyx and the JPM Coin, with a clear focus on services tailored to its institutional clients. By appropriating these technological building blocks while remaining within a highly regulated framework, the bank is paving the way for a gradual integration of digital assets into traditional finance, and foreshadows profound transformations in the cryptocurrency ecosystem, where large institutions could play an increasing role in volumes, infrastructure standards, and product definition.

Similarly, Larry Fink, once skeptical of cryptocurrencies, says his views have changed following the strong rise of BlackRock's Bitcoin IBIT ETF, prompting him to support Bitcoin as an asset and, more importantly, tokenization as a major opportunity to reshape traditional finance.

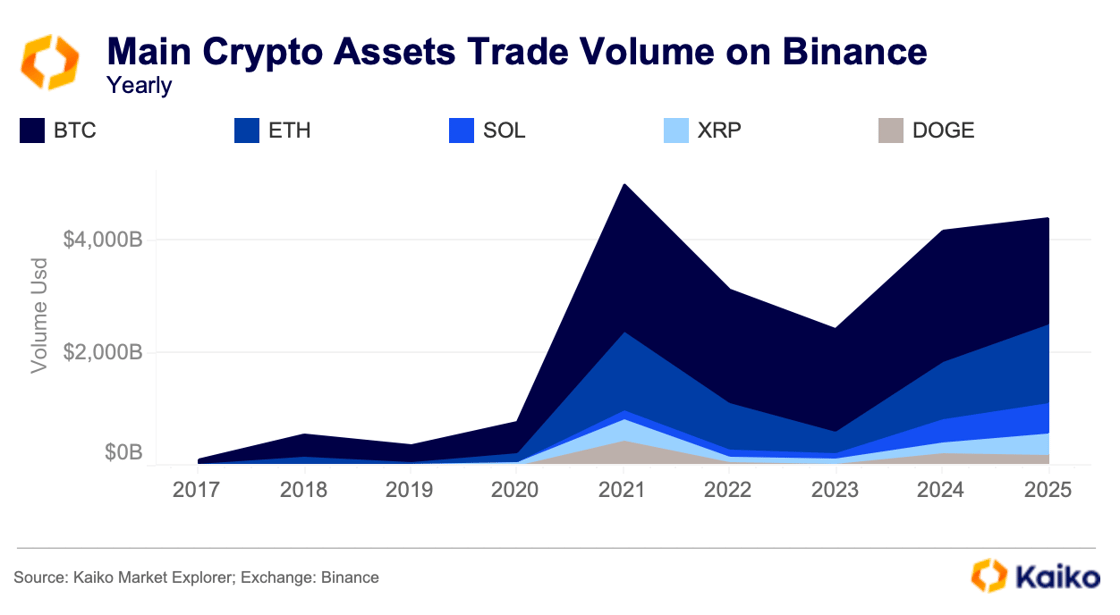

These banks can no longer ignore retail and institutional clients whose need for crypto services is increasing considerably each year. Specifically, if we look at the U.S. Dollar trading volumes on Binance, we can see they have moved from just a few million in 2017, to over $4T in 2025.

In Europe, this transition is also accelerating. The BPCE Group, one of the largest banking groups in France, has just launched a new crypto offering integrated directly into its banking apps through its specialized subsidiary, Hexarq. Specifically, retail customers can now open a dedicated digital asset account, and buy, sell, and hold several major cryptocurrencies (Bitcoin, Ether, Solana, and USDC) from the same interface as their current account. At the European level, BPCE is among the very first major banking groups to do so and joins the select group of banks currently offering this type of service, alongside BBVA.

The Explanations for this Change in Mindset

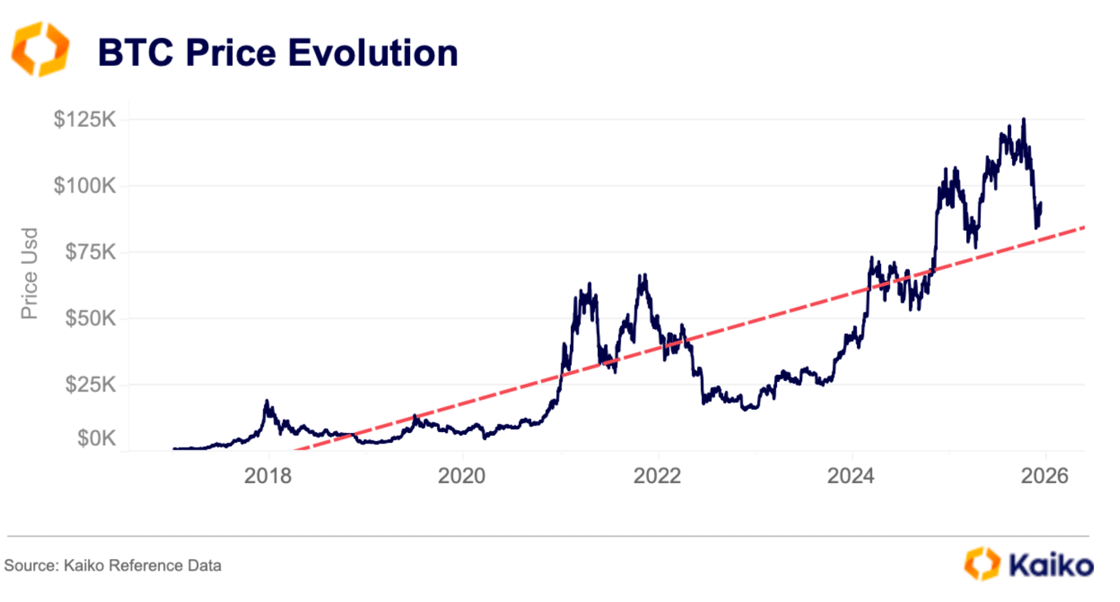

The long-term upward trend of BTC acts as an accelerator for banks, as it transforms crypto from a purely speculative subject into a sustainable asset class that clients want to integrate into their portfolios.

The chart below highlights a structurally bullish trend in Bitcoin's price over the period, despite occasional sharp corrections. In recent years crypto markets have been marked by significant shocks such as the FTX crash in 2022, which drastically increased volatility at that time.

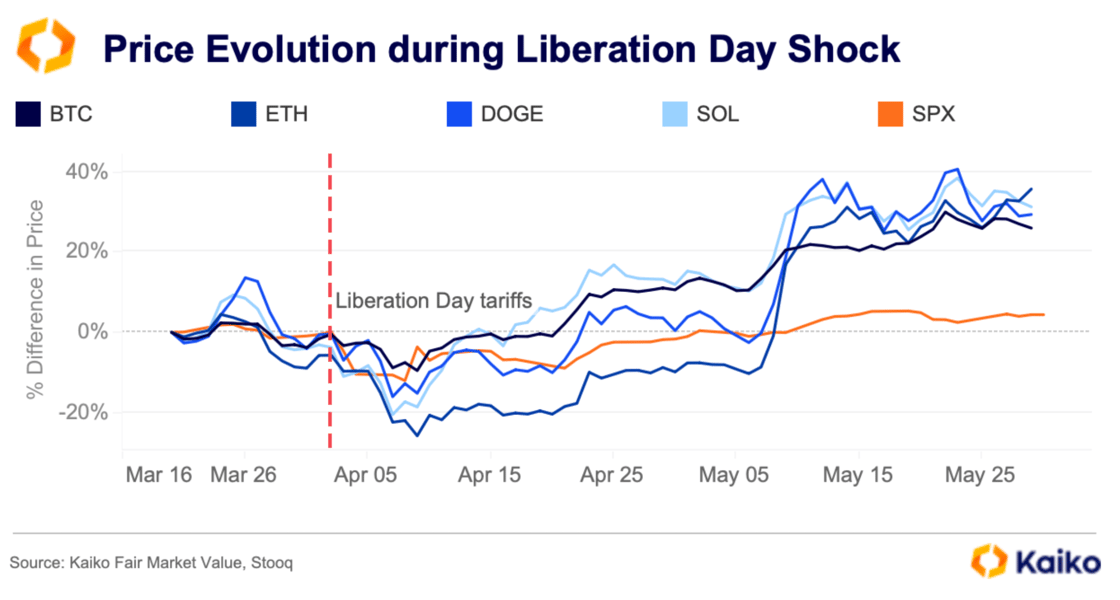

From there, we then looked at the resilience of key assets during major market crashes, such as the one that followed Trump's tariff announcements. We observed that the crypto market was initially driven by the stock market decline, but nevertheless recovered more quickly and strongly than the equity benchmark.

We also observed a sustained increase in Bitcoin’s 1% market depth. This is an important indicator of market maturation from a banking perspective, as rising liquidity improves execution reliability for both institutional and retail participants.

As illustrated in the chart below, market depth trended higher between 2021 and 2025, despite a pronounced, but temporary, drop during the October 10th market crash. Notably, depth has since recovered to normal levels, even as long-term holders have distributed sizable positions. As highlighted in BTC Unfazed by Billion Dollar Sale, the market’s ability to absorb Galaxy’s approximately $9bn (80k BTC) sale with limited price impact underscores how much execution conditions have improved.

All of this matters for institutions, flows are increasingly driven by identifiable, balance-sheet-backed buyers (corporate treasuries and spot ETFs) rather than unknown, Satoshi-era positioning, making supply/demand easier to discern and large trades less destabilizing. This shift from crypto native flow to institutional participation has not only led to deeper orderbooks that can absorb large trades with less price impact, but also contributed to volatility compression.

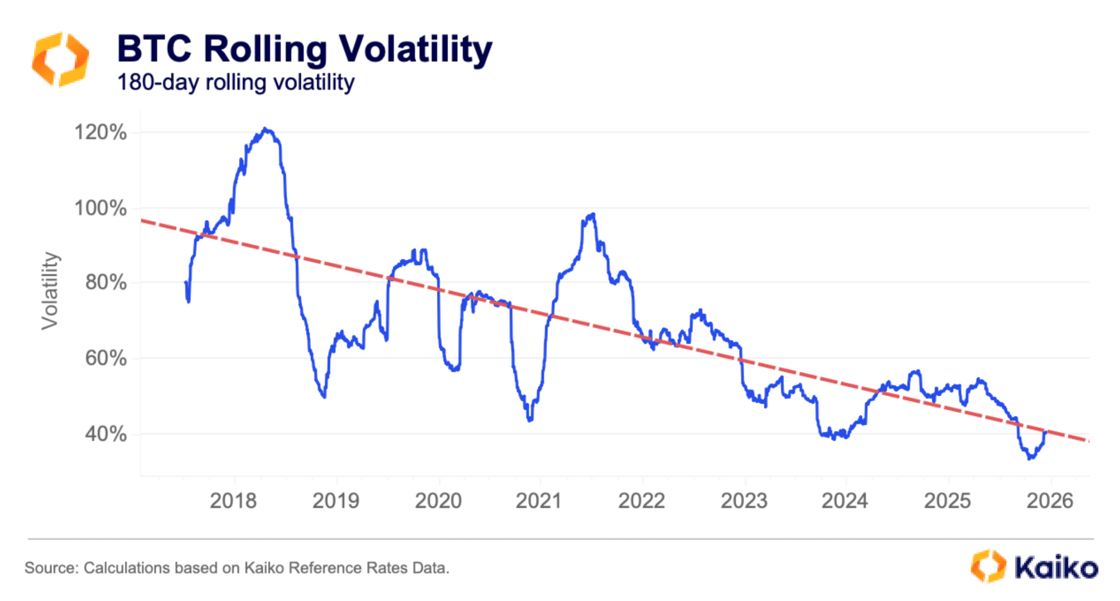

One of the most compelling arguments for institutional adoption of Bitcoin lies in the significant reduction of its volatility over time. The 180-day rolling volatility chart reveals a dramatic stabilization trend: Bitcoin's volatility peaked at approximately 120% in 2018 during the height of the previous market cycle, but has steadily declined to around 35-40% by late 2025.

Beyond the shift away from cyclical crypto investors, the entry of pension funds, asset managers, and corporate treasuries has created a more balanced mix of investors with different time horizons. We also noticed the launch of spot Bitcoin ETFs in early 2024 that provided traditional investors with compliant access channels, spreading ownership across a broader base. After multiple cycles, Bitcoin has demonstrated resilience through various macro environments, reducing uncertainty premiums.

While Bitcoin's current 35-40% annualized volatility remains higher than traditional assets like equities or bonds, it now falls within a range that many institutional risk frameworks can accommodate, particularly for alternative asset allocations. This volatility compression has been instrumental in shifting the narrative from Bitcoin as a purely speculative asset, to a legitimate portfolio diversifier, directly enabling the strategic pivots we're seeing from institutions like Vanguard and J.P. Morgan.

Trust through Regulation

Regulation continues to evolve in the crypto industry, which is reassuring for banks, themselves subject to significant regulatory expectations. This regulation reduces legal uncertainty and provides a clear framework on topics such as stablecoins, reserves, and governance. As a result, banks can offer services with greater transparency regarding obligations and responsibilities, thereby fostering capital inflows, innovation, and competition.

In Europe, we find MiCA, the regulatory framework governing crypto-assets. It establishes common rules across the EU for token issuance, exchange activity, and customer protection, with requirements for transparency, governance, and compliance. More recently in the United States, the GENIUS Act, adopted on July 17, 2025, primarily targets stablecoins by creating a federal framework.

More specifically with regard to banks, there is a fundamental difference when comparing the prudential approaches of the European Union and the United States regarding their' exposure to crypto-assets. The EU, through Capital Requirements Regulation 3 (CRR 3) and its Article 501d, already in force since July 2024, closely aligns with the Basel Committee's SCO60 standard, whose implementation deadline is 2026 (even though this deadline is being questioned with regards to the positioning of the U.K. and the U.S.). This standard establishes the first global prudential framework governing banks' exposure to crypto-assets. Its objective is to ensure consistent capital treatment and uniform risk management across jurisdictions, thereby preserving financial stability while allowing controlled bank participation in crypto markets.

The United States rejects this system, which the Trump administration considers "anti-competitive" and "anti-innovation”. This divergence is set to fragment global standards, increase cross-border supervision, and create a potential competitive advantage for U.S. banks subject to lighter capital requirements. You can learn more about this from a previous Kaiko report that goes into more detail.

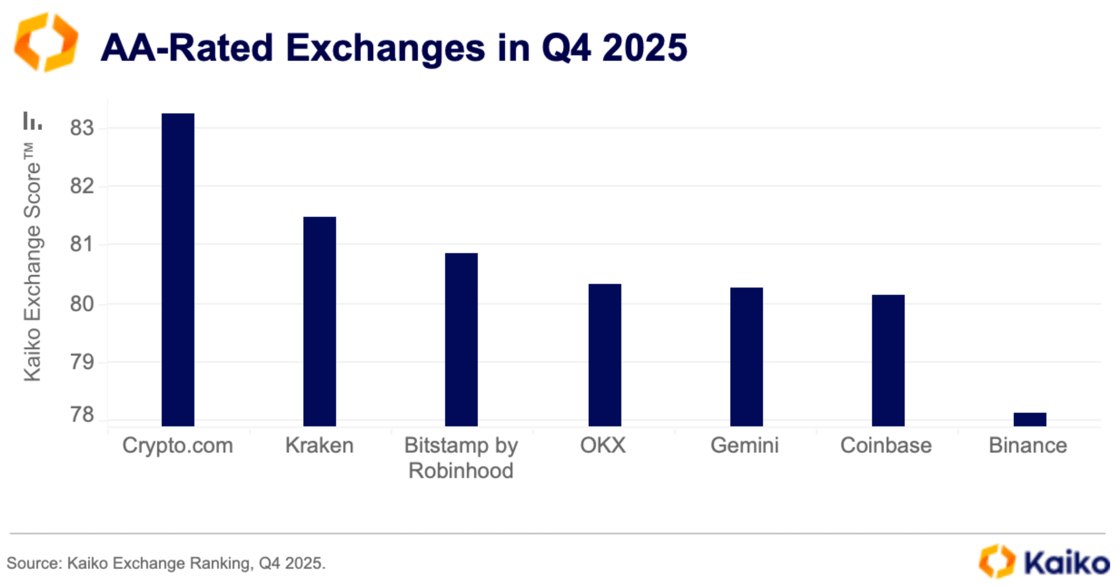

Similarly, the institutionalization of the market also depends on the governance of the platforms on which these services rely, since cryptocurrency price discovery still primarily takes place on exchange platforms. In our Kaiko Exchange Ranking Report (Q4 2025), we highlight a turning point where platforms affiliated with public markets tend to demonstrate higher standards. This is because the transparency, governance, control, and accountability requirements imposed by a listing translate directly into measurable improvements in ranking criteria (particularly in governance, but also in security).

As frameworks like MiCA reduce legal uncertainty, the quality of exchange governance becomes a key driver of trust for regulated entities such as banks, which seek infrastructures aligned with their own prudential and compliance obligations.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

To manage your subscription with Kaiko Premium Research, cancel, or update your payment method, click here.

.png?upscale=true&width=1200&upscale=true&name=data%20debrief%20(1).png)