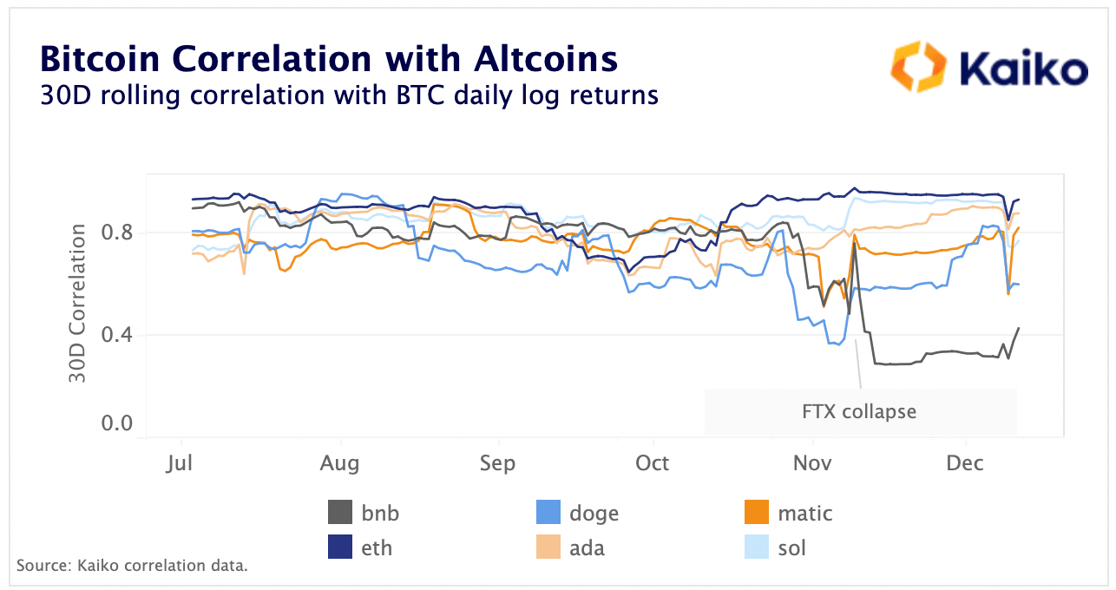

Price Movements: BTC's correlation with BNB has dropped significantly since FTX's collapse, a sign that Binance's token is diverging from wider markets.

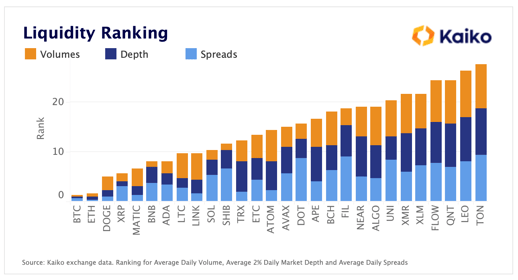

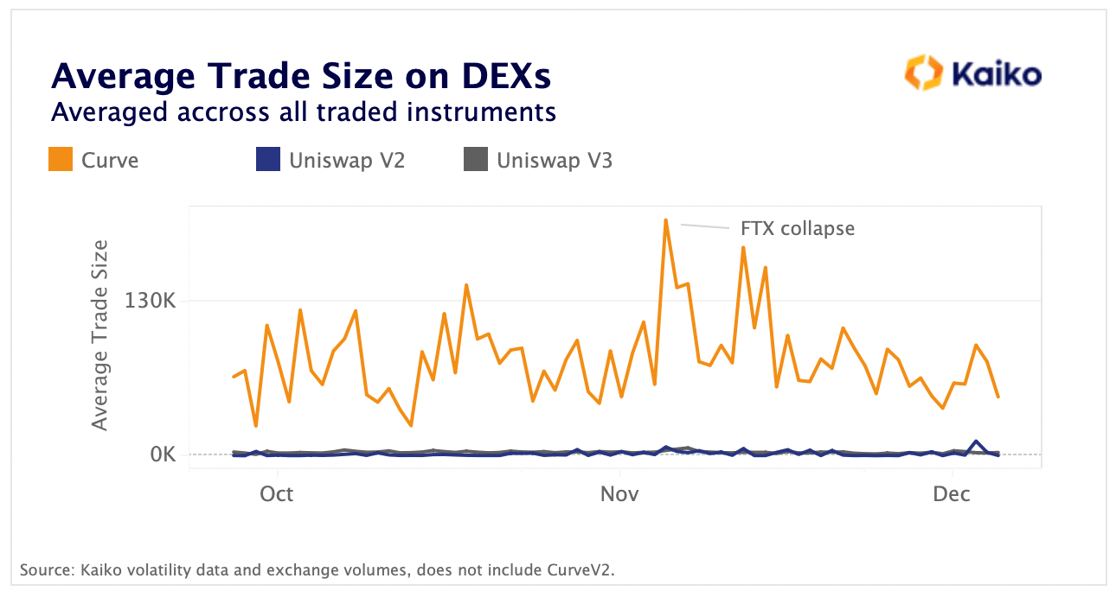

Market Liquidity: Curve, the DEX optimized for stablecoin swaps, is still mostly used by whale traders.

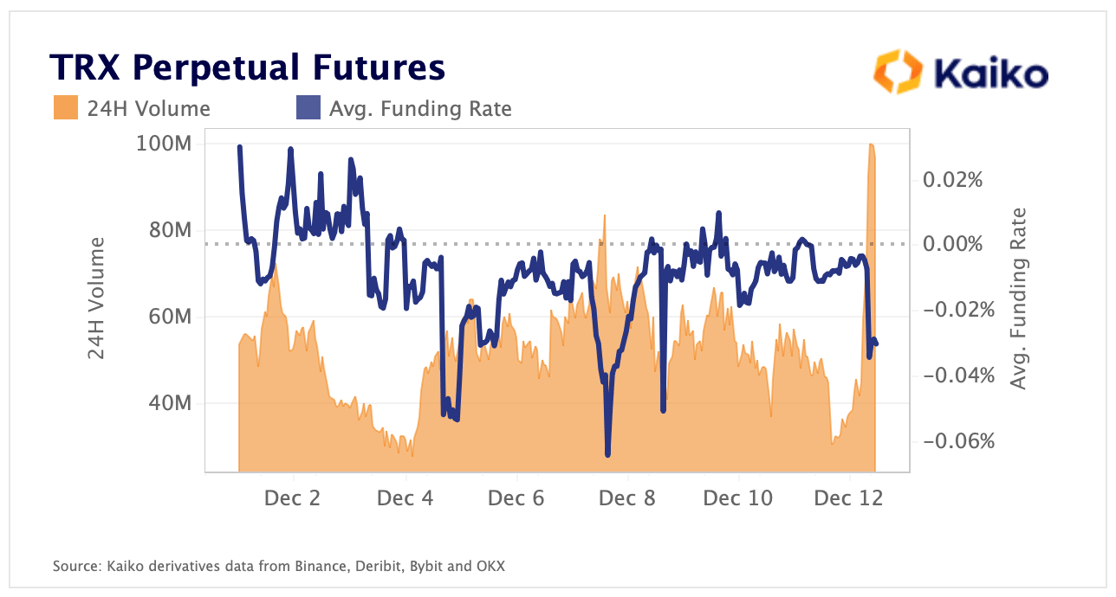

Derivatives: Tron futures skew bearish after the network's native stablecoin, USDD, depegged to $.97.

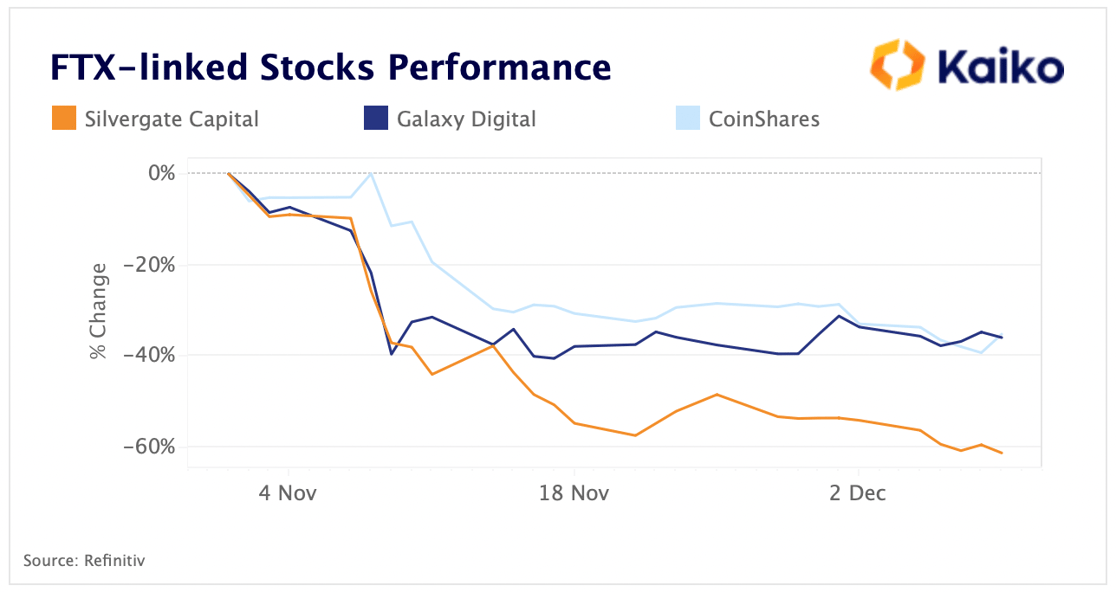

Macro Trends: Silvergate Bank, which processed transactions for FTX, has seen its share price tank 60% since the collapse.

The Kaiko research team has extensively covered the FTX collapse. In our upcoming webinar, we will dive deep into the data we used and discuss how liquidity analysis can prevent the next black swan event. Register below:

Terra collapse returns to the spotlight amid FTX probe.

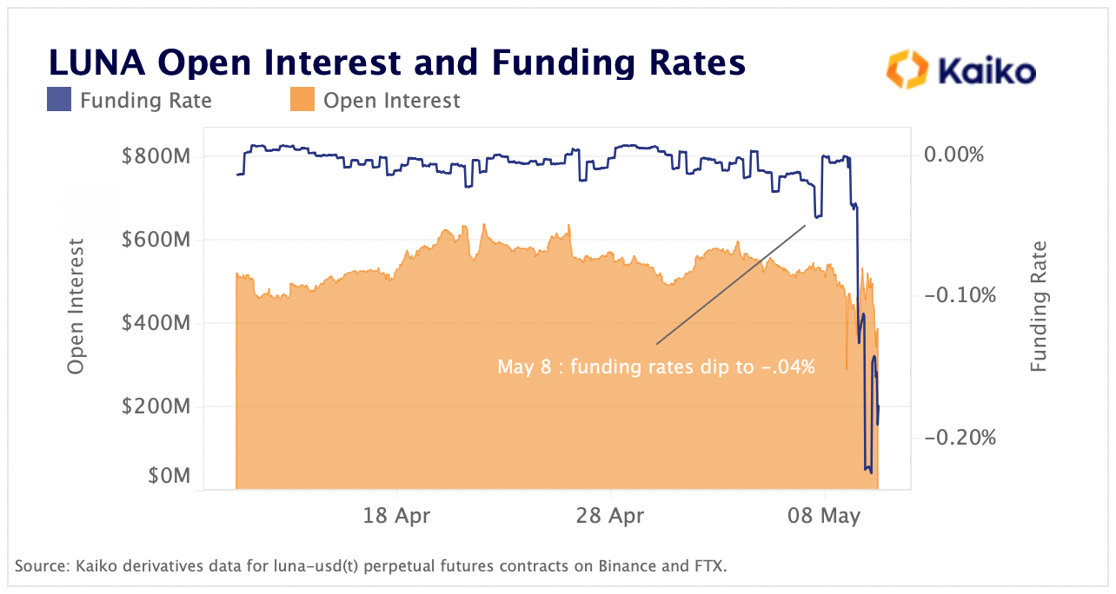

The New York Times reported last week that federal prosecutors are investigating whether Sam Bankman-Fried manipulated the prices of LUNA and UST. While the details of the investigation are light, an examination of the LUNA and UST perpetual futures on the two largest markets, Binance and FTX, does not show a strong increase in open interest or growing short bias in the weeks leading up to the collapse. This suggests that a manipulation event was not coordinated over a long time interval, although it does not rule out the possibility of a rapid shorting attack.

Luna/UST began spiralling on the evening of May 9, thus any manipulation attempt would need to be apparent in the data before this date.

Throughout April 2022, LUNA's open interest and funding rates were volatile, suggesting traders lacked direction and took both short and long bets. Open interest increased by over 30% in early April before declining by over 20% at the end of the month and funding rates oscillated between positive and negative levels. On May 8th, funding rates dipped to -.04%, although open interest barely budged.

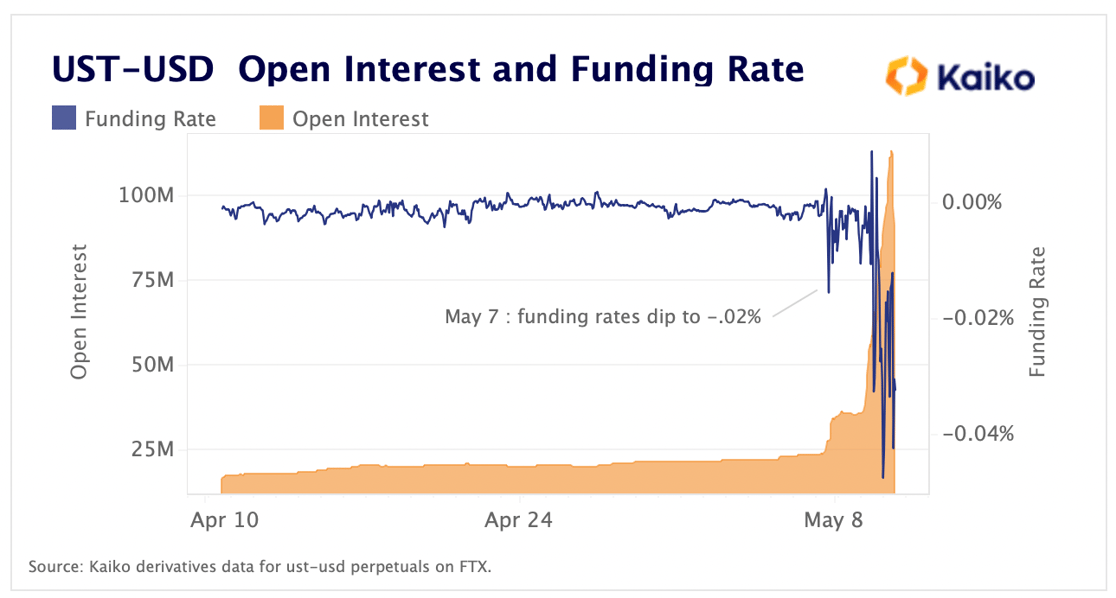

We observe a similar trend on UST perpetual futures markets, which only traded on FTX. Open interest on the UST-USD contract increased slowly and steadily, from $15-20mn at the beginning of April to $23mn just before UST began to depeg. On May 7, there was a $10mn increase in OI and funding rates flipped negative, which could be interpreted as a relatively modest initial warning sign.

By May 9, open interest and funding rates for both LUNA and UST were extremely short biased as the stablecoin started to publicly unravel, which makes it hard to determine whether a single entity was behind a manipulation. While the data does not point to a coordinated manipulation in the weeks before UST's collapse, this doesn't rule out possible nefarious on-chain behavior.

View our full investigation of the Terra collapse here and our investigation of on-chain DEX activity here.

Price Movements

Markets trade flat ahead of FTX congressional hearings.

Crypto markets traded flat as the industry gears up for two congressional hearings on FTX’s implosion, in which SBF is expected to testify. In another FTX contagion twist, the crypto media world was shaken after Axios reported that The Block had been secretly funded by Alameda Research, raising questions about their editorial independence. Meanwhile, Do Kwon, the internationally wanted co-founder of the Terra network, has reportedly moved to Serbia.

Smaller Layer 1s offer mixed returns since the Merge.

Alternative Layer 1s have been a mixed bag following the Merge, as TVL on most chains has slumped. For reference, ETH is down 22% in this timeframe with relatively little volatility. Fantom (FTM), meanwhile, has been highly volatile, gaining 25% in a day amidst rumors that DeFi pioneer Andre Cronje would be returning to the chain following his departure earlier this year. FTM subsequently lost these gains before again spiking following a blog post from Cronje that revealed Fantom Foundation’s financials, including a theoretical 30-year runway based on non-FTM holdings, including stablecoins and other crypto assets.

Radix (XRD), a lesser-known Layer 1, surged 50% in a matter of days ahead of its conference unveiling future development on the network; it has since given back nearly all of these gains. NEAR provides an example of an alternative Layer 1 with few positive catalysts, and is down nearly 65% in the past two months. ETH, FTM, NEAR, and XRD are down 65%, 89%, 90%, and 85% this year, respectively.

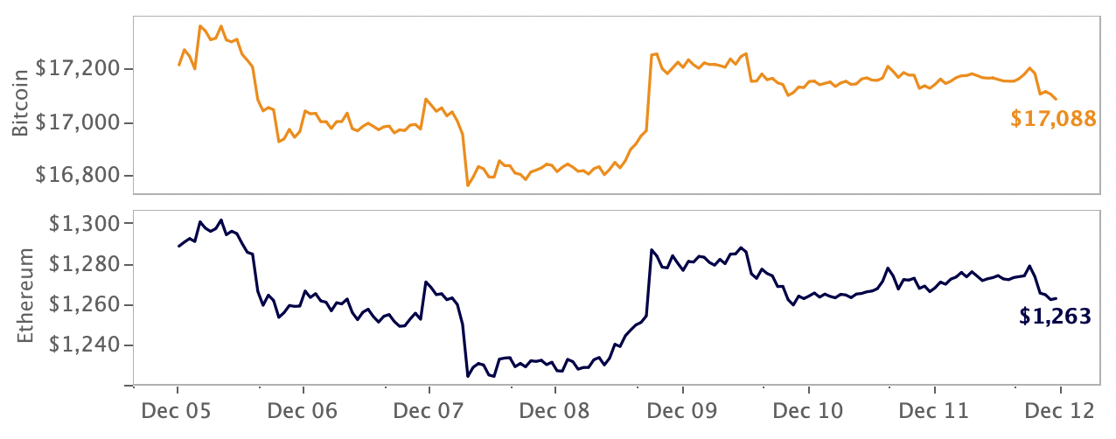

BTC's correlation with BNB diverges from other altcoins.

During market crashes, crypto correlations typically strengthen across the board. BTC's correlation with BNB has thus been a clear outlier, dropping to a weak positive correlation of .4, its lowest level since 2020. Binance has made a strong push over the past month promoting proof of reserves, which could be boosting confidence in the exchange, which has a spillover effect on the price of BNB. Meanwhile, BTC's price has stayed stagnant. For comparison, BTC's correlation with the altcoins DOGE, MATIC, ADA, and SOL has remained steadily positive into December.

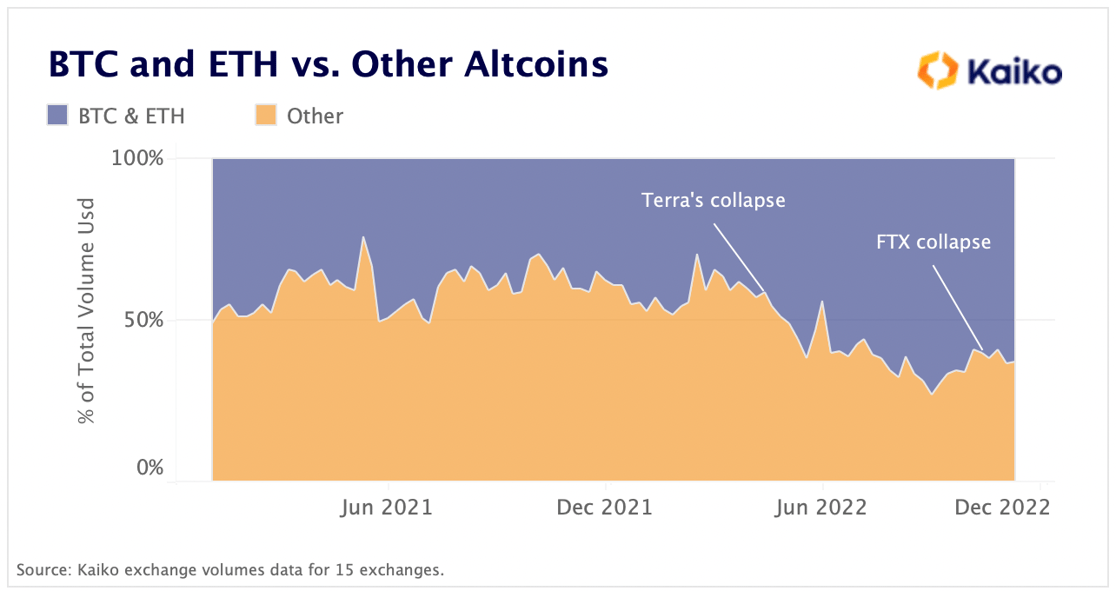

The share of altcoin trade volumes on top centralized exchanges remained relatively resilient, hovering around 37% following the FTX collapse. Typically, in times of market uncertainty traders rotate into the most liquid crypto assets — BTC and ETH — which leads to a decline in the market share of higher-beta altcoins. In the months following Terra's implosion, the share of altcoin trade volume relative to BTC and ETH tumbled from 59% to 27%. However, altcoins kept their ground in November following the collapse of FTX, suggesting much of the de-risking has already taken place over the summer. The trend in trading volumes mirrors the relative stability of BTC's dominance as measured by its market cap relative to other cryptos.

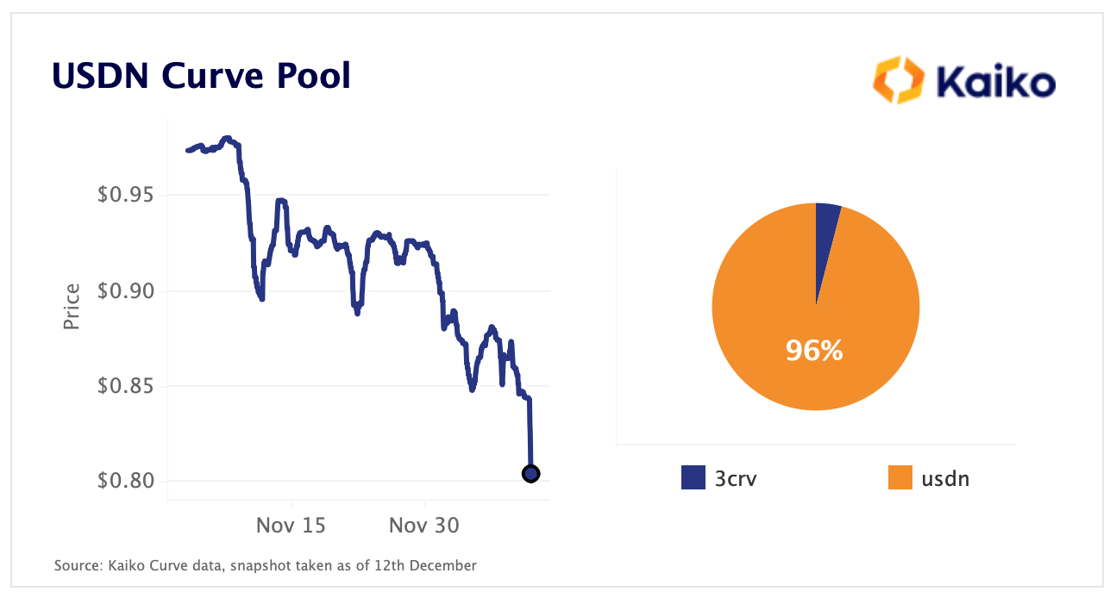

Curve is still used mostly by whale traders.

Curve, the decentralized exchange optimized for stablecoin swaps, has experienced a remarkable surge in usage over the past year, with trade volumes recently soaring past all time highs. Yet, when looking at the average trade size, we can observe that the exchange is still mostly used by whale traders. The average trade size across all stablecoin liquidity pools was around $50k as of December. During FTX's collapse, average trade size on Curve V1 hit $200k. This stands in sharp contrast to the DEX Uniswap V3, where average trade size is between $3k and $7k across all pools. On centralized exchanges like Coinbase, average trade sizes are typically between $2k and $4k.

Aave wBTC borrows hit all-time high in November.

Borrows of wBTC from Aave V2 hit $375mn in November, far surpassing the previous monthly high (set in May) of $218mn. This surge in wBTC borrowing came as the industry became increasingly aware of Alameda’s involvement with the token, as one of the highest volume merchants. Merchants are responsible for sending BTC to a custodian (BitGo) who then sends newly minted wBTC to the merchant, or vice versa; for more on wBTC see our previous Deep Dive. This mechanism means that wBTC is likely not at risk because of FTX/Alameda’s collapse, though this did not stop fear from spreading, causing wBTC to deviate slightly from BTC’s price.

It is likely that the increased borrowing of wBTC was due to shorting of the token (by depositing a stablecoin like USDC and borrowing wBTC, a user would profit from wBTC’s price dropping) or by users looking to arbitrage the token. As a result of increased borrowing, wBTC’s supply APY surged to all-time highs of just over 0.3%, though it has since dropped closer to normal levels.

Supply APY fluctuates based on the amount of a certain asset deposited, and how much of the deposited asset is being borrowed. Assets with low borrows relative to supply (known as utilization rate) will have a low supply APY, and this increases as utilization rate increases. wBTC has historically had the lowest supply APY of any asset on Aave V2, and even amidst this increase the rate remains low relative to other assets (ETH is currently over 1.5% APY).

USDN depegs following Korean exchanges warning.

Another algorithmic stablecoin, USDN, lost its peg last week after a collection of South Korean exchanges issued a warning to investors regarding WAVES, the native token of the Waves blockchain on which USDN is built and which USDN uses as collateral. One of the exchanges in the association, Upbit, announced that the platform is looking to suspend the WAVES/KRW and WAVES/BTC pairs and added that it will monitor the token over a period of the next two weeks to determine its next course of action. The Curve pool for the USDN stablecoin became extremely imbalanced last week as investors looked to cash out from USDN. As of this morning, USDN makes up a staggering 96% of its Curve pool and trades at 80 cents on the dollar as it failed to regain its peg.

Derivatives

Tron futures bearish after USDD stablecoin depegs

Tron’s stablecoin USDD has depegged and is trading at below $0.97, its lowest level since June. Tron’s USDD originally followed the same model as Terra’s UST, but following the collapse of Terra earlier this year the stablecoin pivoted to an overcollateralized approach, and is now reportedly backed with a collateral ratio of 200%. This hasn’t stopped fears around the Tron ecosystem as a whole suffering as a result of a USDD depeg: perpetual futures investors piled in to short Tron’s token, TRX. Over the past day, 24h volume has surged from $50m to $100m, and funding rates dipped negative.

Tron founder Justin Sun resorted to Twitter to quell fears of another Terra-esque event, mimicking Do Kwon’s “deploying more capital - steady lads” tweet, announcing he had swapped $770k worth of USDD in an effort to shore up its peg.

Macro Trends

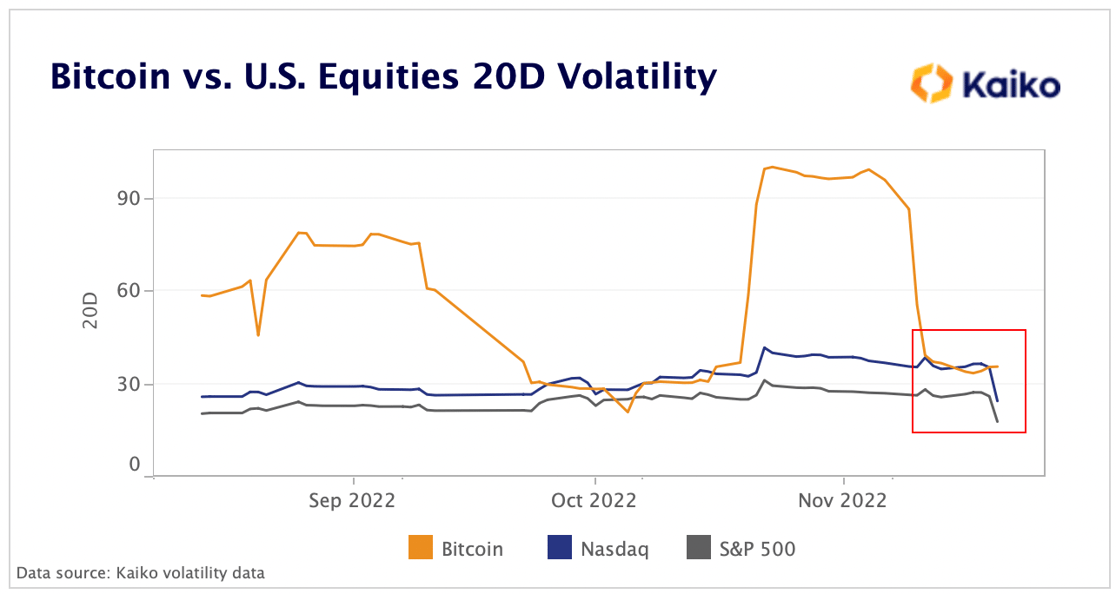

Crypto short term volatility subdues to equal stocks

November was a black swan month for crypto as an asset class as it underwent another episode of a contagion crisis that has plagued crypto all year. This was reflected in the 20D volatility spread between BTC and stocks, as BTC's 20d volatility peaked as high as 3x the volatility of stocks. The good news for crypto is that volatility seems to have subdued for the moment as BTC’s volatility has plummeted to equal the Nasdaq. The only decoupling catalysts crypto has experienced this year have been negative events such as FTX or Three Arrows Capital and aside from these major incidents its price action remains tied to macro events.

Silvergate's share price tanks 60% since FTX Collapse.

Silvergate Bank, the largest crypto bank in the U.S. and one of the few allowing customers to move fiat currencies onto crypto exchanges, has lost a whopping 60% of its value since the start of November. Earlier this year, Silvergate managed more than $16bn in assets, up from less than $1bn in 2019. For context, Galaxy Digital and CoinShares, which both had a multi-million exposure to the fallen exchange, are also down 35% but have seen their share prices stabilize in December.

Silverbank has been criticised for accepting FTX and Alameda deposits and processing wire transfers for companies and individuals to the exchange. Other regulated lenders with ties to the crypto industry such as Provident Bancorp and Signature Bank announced losses and plans to significantly reduce their crypto exposure. Historically, financial institutions have avoided crypto, with only a handful of lenders offering custody, transaction processing and large-scale dollar deposits for crypto companies.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-Dec-12-2022-10-15-30-7115-AM.png?upscale=true&width=1116&upscale=true&name=image%20(5)-Dec-12-2022-10-15-30-7115-AM.png)

.png?upscale=true&width=1116&upscale=true&name=image%20(4).png)

%20(1).png?upscale=true&width=1116&upscale=true&name=image%20(3)%20(1).png)