Trend of the Week: After Binance eliminated BTC trading fees, BTC volumes surged to all time highs.

Price Movements: Solana ecosystem tokens have disproportionately struggled amid several network setbacks.

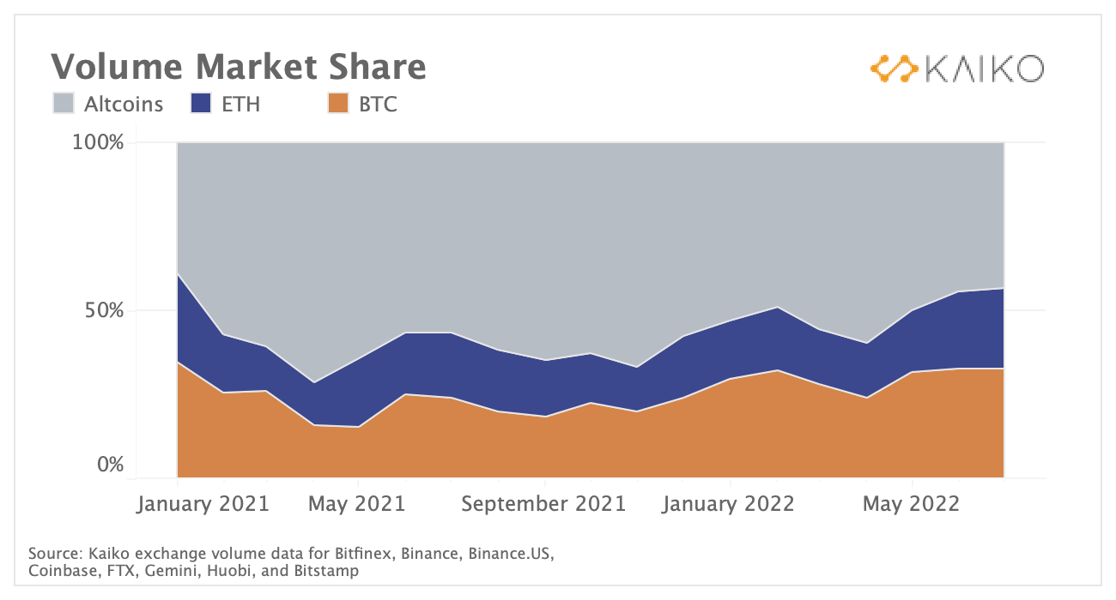

Market Liquidity: Altcoin volumes aggregated across the biggest exchanges have fallen to just 43% of total volumes, from a peak of 71% last year.

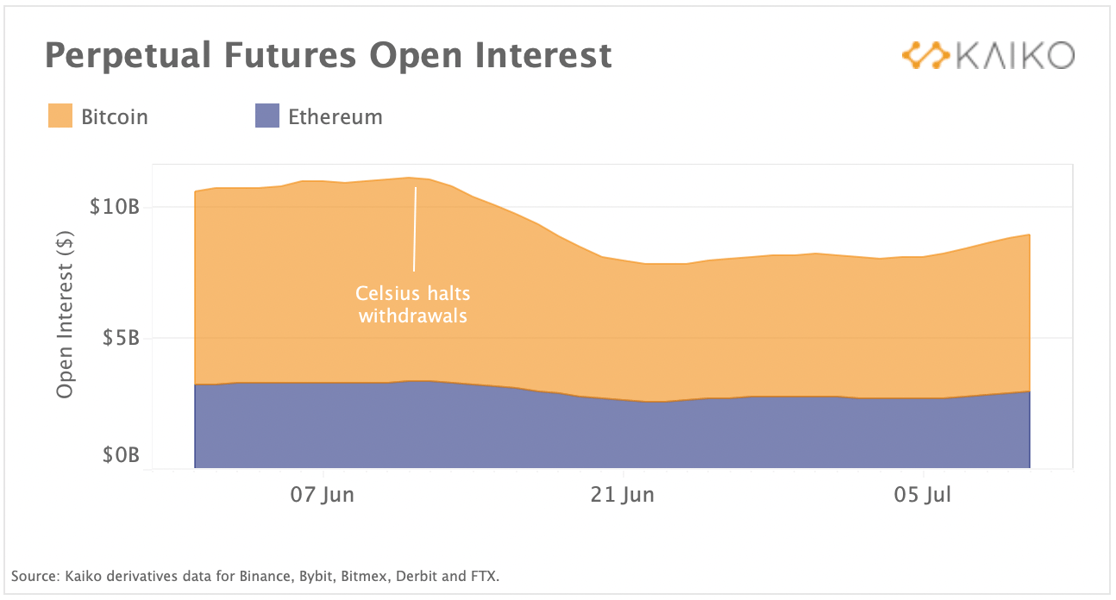

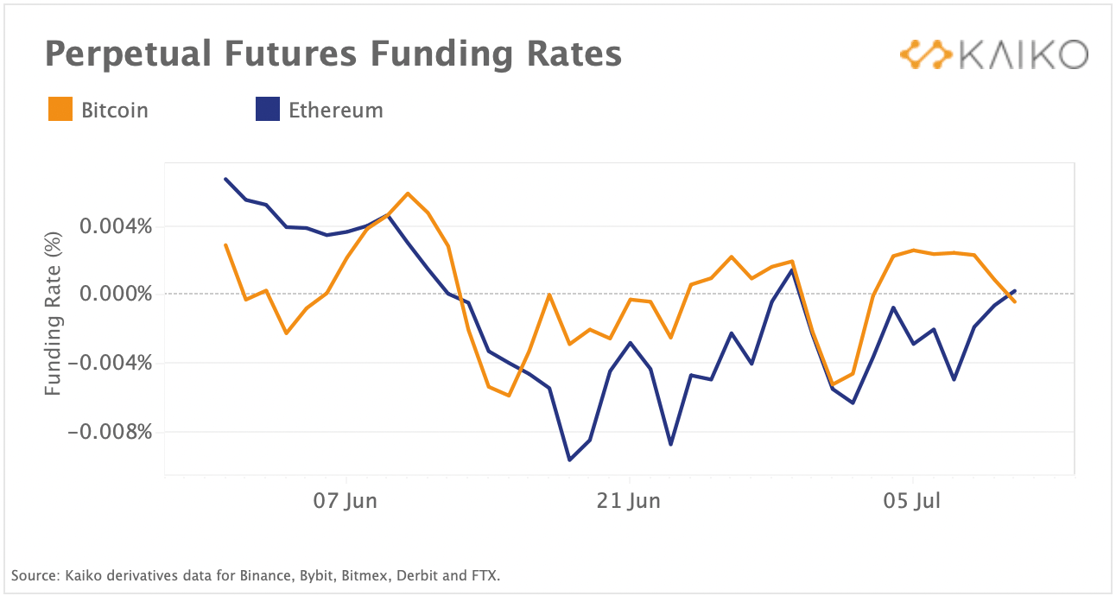

Derivatives: Open interest has recovered slightly in July and funding rates re-set to neutral.

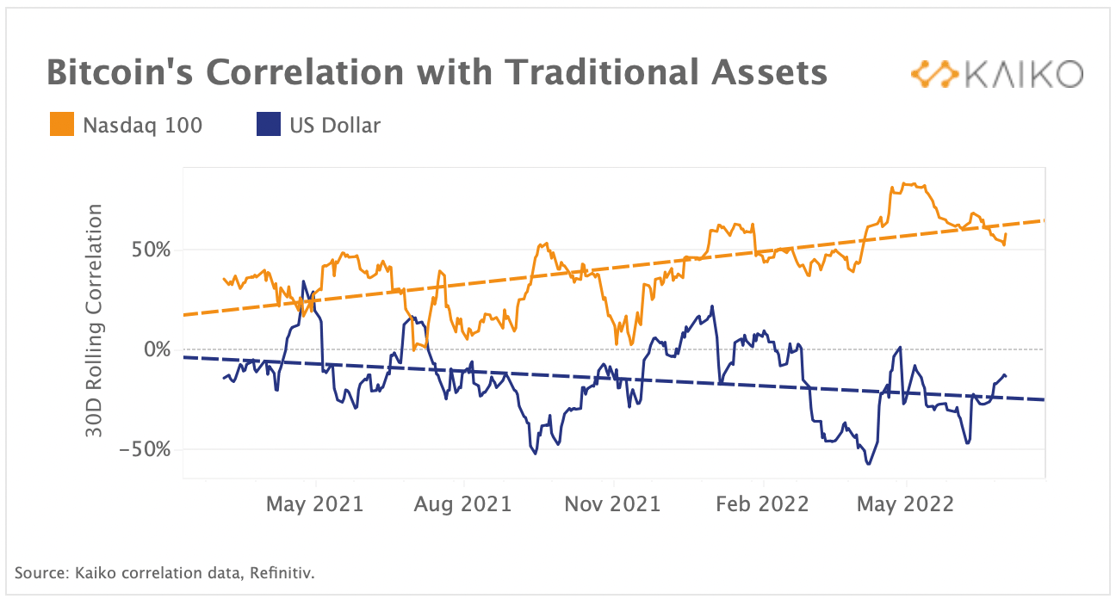

Macro Trends: Bitcoin's inverse correlation with USD has deepened throughout 2022 as the greenback hits 20-year highs.

Trend of the Week

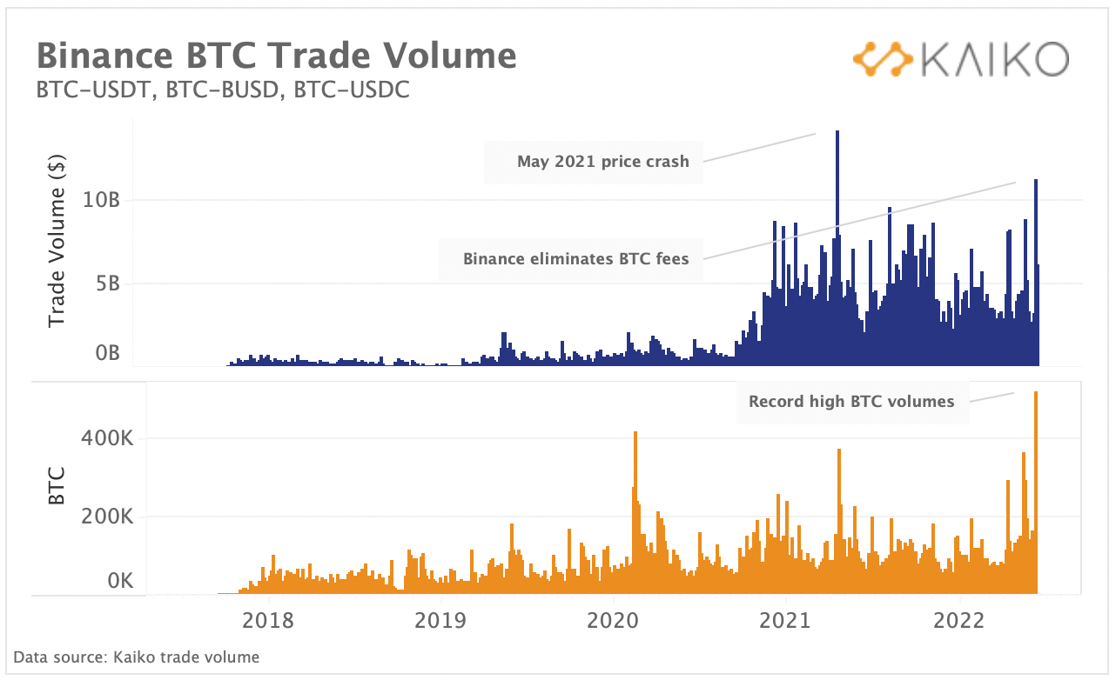

Binance BTC volume breaks all time highs after fee elimination.

Last week, Binance removed fees for 13 bitcoin trading pairs to celebrate the exchange's five-year anniversary. The market's reaction was instantaneous. Within minutes, BTC trade volume started surging across the top pairs, later that day breaking all time highs (denominated in BTC) with more than 500,000 BTC exchanged across the BTC-USDT, BTC-USDC, and BTC-BUSD pairs. This amounted to the equivalent of $11.3bn traded, the second highest volume day (denominated in $) ever recorded, second only to May 19th, 2021, the day of a historic price crash.

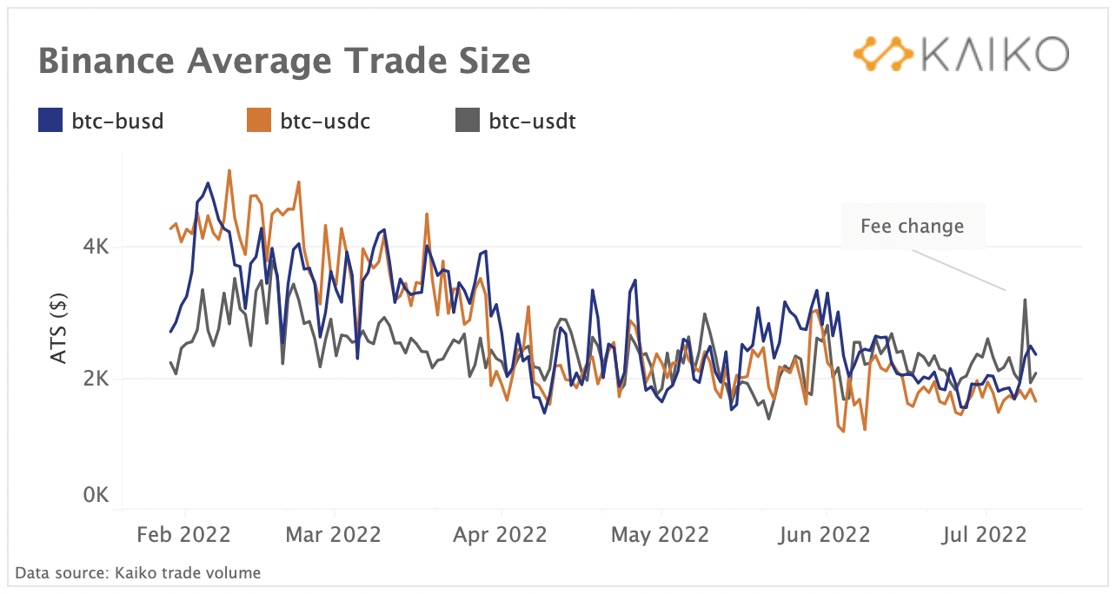

Yet, it soon became clear that a lot of the activity was likely wash trading; zero fees enabled traders to reach VIP levels with minimal risk. Binance's CEO soon announced that they would remove all incentives to wash trade and exclude BTC trades from VIP calculations. Looking at the average trade size after the fee change, we can observe a sharp spike for the BTC-USDT and BTC-BUSD pair, evidence that on average traders were placing larger orders starting July 8th.

Overall, the longterm trend shows that average trade sizes have fallen considerably since the start of the year. For the BTC-USDC and BTC-BUSD pairs, the average trade size was around $4k in February, and today it hovers around $2k, despite a slight bump thanks to the fee elimination. BTC-USDT trade sizes have since reverted. Ultimately, trading fees are a powerful incentive against wash trading and market manipulation and it will be interesting to see if other exchanges follow Binance's suit.

Price Movements

Bitcoin stages modest recovery despite continued contagion.

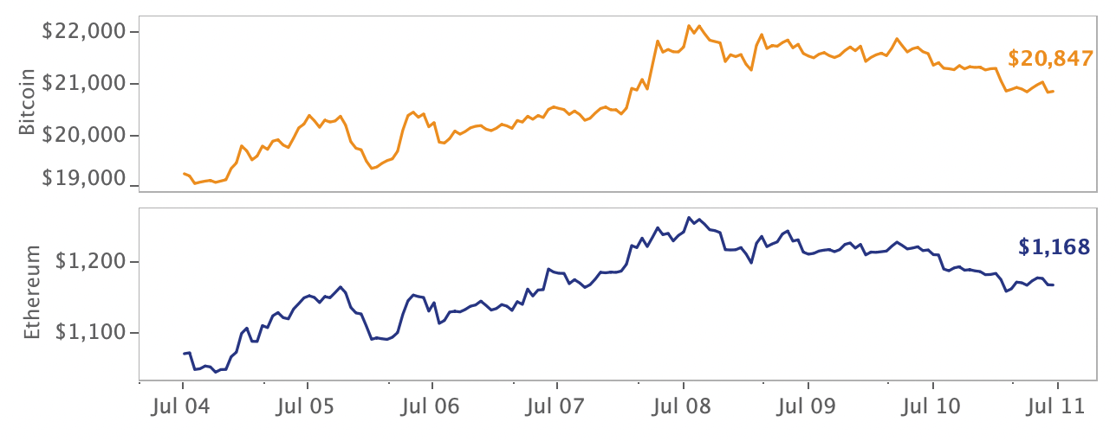

Crypto markets staged a modest recovery last week despite a new round of entities claiming exposure to 3AC’s meltdown. Both Blockchain.com and Deribit revealed they are creditors of the beleaguered hedge fund, while Voyager Digital officially filed for bankruptcy, with reportedly 60% of their loan book granted to the fund. The Celsius saga further deepened this week after a pseudonymous DeFi asset manager filed a suit claiming the lender had not paid them for their services. The suit alleges extremely poor risk management and no hedging for client funds deployed in high-risk DeFi protocols managed by an external asset manager. While the crypto market contagion remains ongoing, BTC managed to close the week above $20k and ETH above $1.1k.

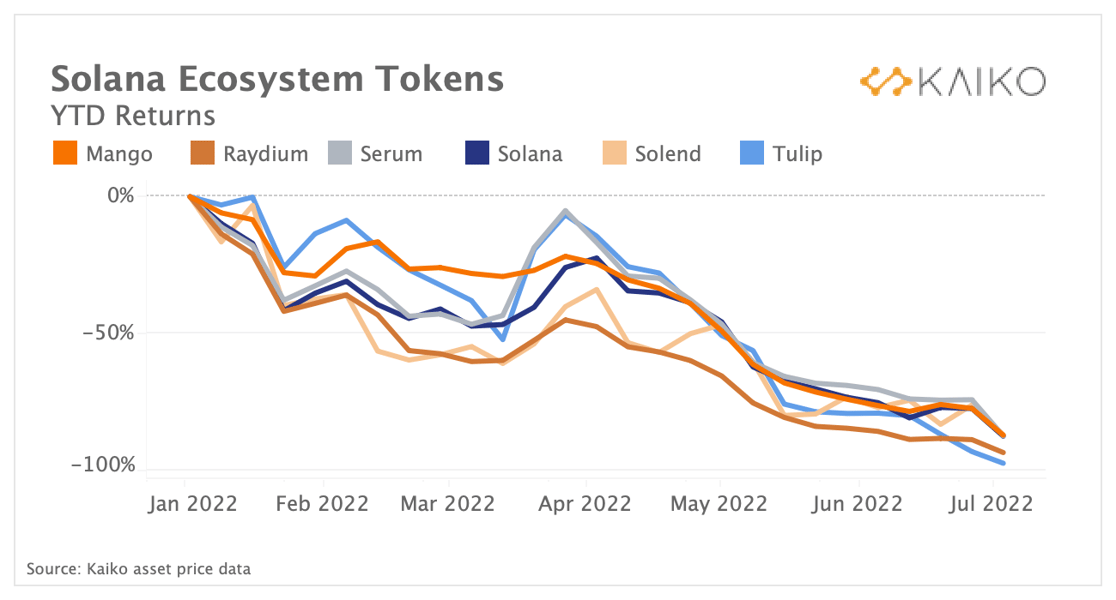

Solana ecosystem struggles.

Solana, one of the top alternative Layer 1 blockchains, has had a particularly difficult year marked by multiple network halts and decreasing usage. According to Solscan, daily transactions at the beginning of the year hovered around 80mn; this figure has decreased to 35mn. This has been reflected in the price action for tokens of most of the major Solana protocols. Tulip, the top yield aggregation protocol, has dropped nearly 98%, while Raydium, the second largest DEX by TVL according to DeFiLlama, is down almost 95%.

Solana’s SOL token has fared the same as many of the protocols built on it; Serum (DEX), Solend (lending), and Mango (derivatives trading) are all down over 85% on the year. Just last week the network faced further complications after a SOL investor filed a lawsuit alleging the token is an unregistered security that has only benefitted insiders.

Kaiko Market Reports

Data-driven commentary on June's most significant market events

Altcoins lose market share during latest downturn.

The volume market share for altcoins, defined as everything except BTC and ETH, has declined from a peak of 71% in April 2021 to just 43% now. In that same time, ETH and BTC both doubled their market share from 13% to 24% and 16% to 33%, respectively. This reflects the typical bear market narrative in which traders and investors turn away from more speculative tokens and towards the two most established. BTC and ETH volumes have also been bolstered by a variety of events, including the Terra collapse and Celsius’s troubles with Lido Staked Ether. Most recently, Binance and Binance.US removed trading fees for BTC pairs; as the world’s largest exchange this will likely have a noticeable impact on total volume market share.

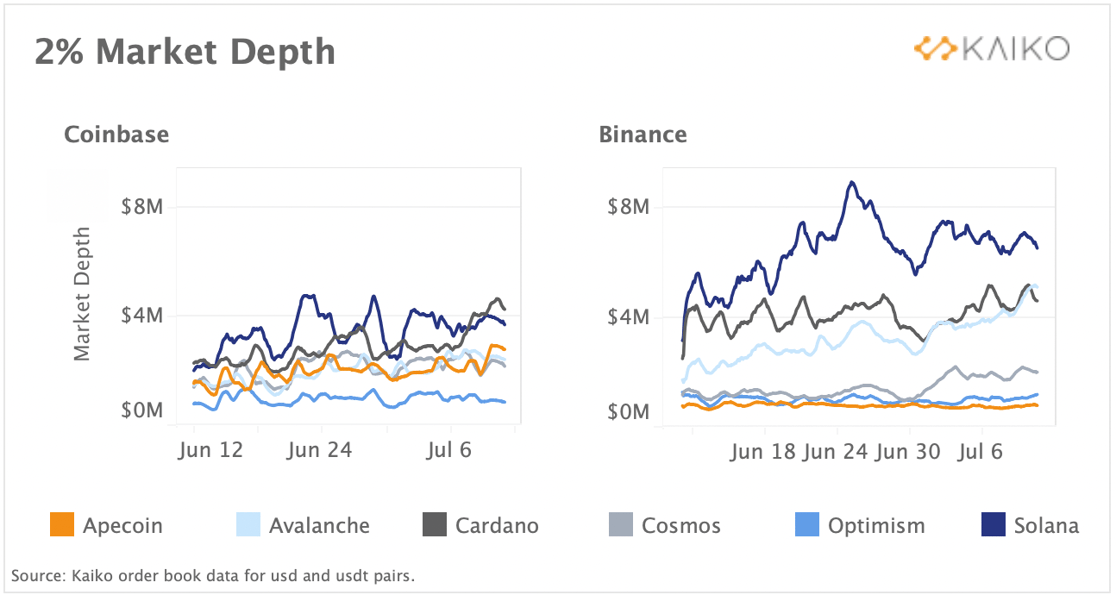

While overall trading activity for altcoins has fallen relative to BTC and ETH, market depth for some of the higher-caps has increased on both Coinbase and Binance for both USD and USDT markets. 2% market depth is denominated in USD(T) and shows a steady increase since the worst of the market contagion, which suggests that market makers are rebuilding their positions after the recent period of volatility. The amount of bid and asks on SOL-USD(T) order books has increased by over 50% since mid-June on both Coinbase and Binance. Cardano’s ADA market depth has also risen despite ADA losing nearly 20% of its value since mid-June. Depth for the newly-launched Optimism (OP) token held relatively steady even though the token is down 15%. Cosmos’s ATOM, Avalanche’s AVAX and Apecoin’s APE also saw an improvement of liquidity partly supported by an increase in price since mid-June.

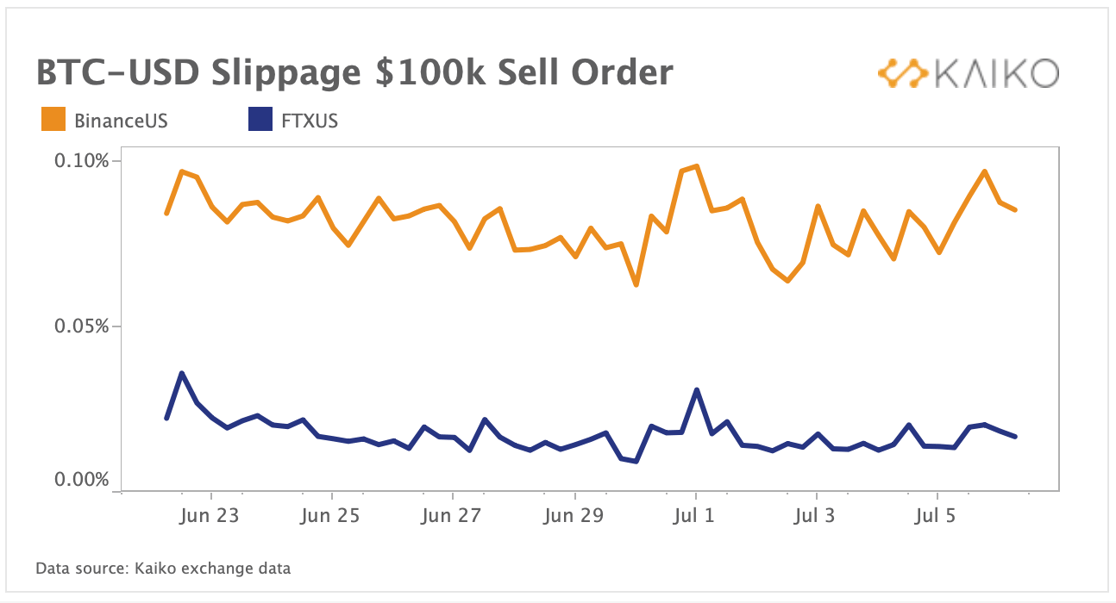

Traders face higher slippage on Binance.US vs. FTX.US.

The introduction of zero fee trading on both Binance.US and Binance has brought into play an interesting market dynamic whereby traders will weigh zero fees with more indirect fees on an exchange such as slippage. In some cases a trader will prefer to pay a maker and taker fee in order to avoid high slippage costs from less liquid exchanges. On Binance Global, liquidity is not an issue, but on the much smaller Binance.US, we can observe that despite no fees, price slippage remains high.

Above we’ve charted the simulated slippage on a $100k sell order on BTC-USD pairs for the US arms of FTX and Binance and can see that slippage on a $100k order is nearly 5 times the cost compared to FTX.US. In order to make an apples to apples comparison it’s important to look at the trading fees on FTX.US for BTC pairs, which include a higher taker fee on the >$1mn 30D volume fee tier at 0.15%. FTX.US slippage ranges from 0.01% to 0.02%, added on to 0.15% of taker fees leaving a simulated fee of about 0.17%. Binance.US slippage on the other hand was more volatile in the last couple of weeks, ranging from 0.06% to 0.10%, but with zero taker fees for BTC trades the total comes in significantly cheaper than FTX.US, despite the higher slippage on Binance.US.

After Binance.US eliminated fees, there was a near instant effect on market depth, with a sharp increase in 2% depth across all BTC fiat/stable pairs.

There was a spike in the week following the announcement before a return to more normal levels, though the BTC-USD pair has since surged to new highs. BTC-USDT depth has also increased significantly, while BUSD and USDC are on a more gradual trend upwards. Market makers may increasingly provide liquidity on Binance.US if the exchange’s volume market share continues to grow.

Derivatives

Open interest inches upwards as funding rates re-set to neutral.

The amount of open Bitcoin and Ether perpetual futures contracts has recovered slightly in early July after dropping double digits last month. Bitcoin perpetual futures open interest rose 11% to $6bn since the start of this month partly supported by a 7.6% increase in prices. Ether’s open interest also rose albeit at a slower pace and is up 7% to around $3bn. The increase was mainly driven by rising open positions on the two largest derivatives exchanges, FTX and Binance.

Both Bitcoin and Ether funding rates, averaged across five exchanges, reset to neutral as global risk sentiment saw some recovery last week. Negative funding rates suggest that more traders are entering short positions and have a bearish bias and vice versa. Funding rates have been mostly negative since early June on mounting contagion fears. Sentiment was particularly bearish around altcoins with Ether funding rates falling to their lowest level in almost a year last month.

Overall, the increase in open interest suggests that new capital is entering the market following a period of strong volatility over the past month. However, risk sentiment remains fragile due to rising macro uncertainty following the Fed's surprise 75bps rate hike last month.

Macro Trends

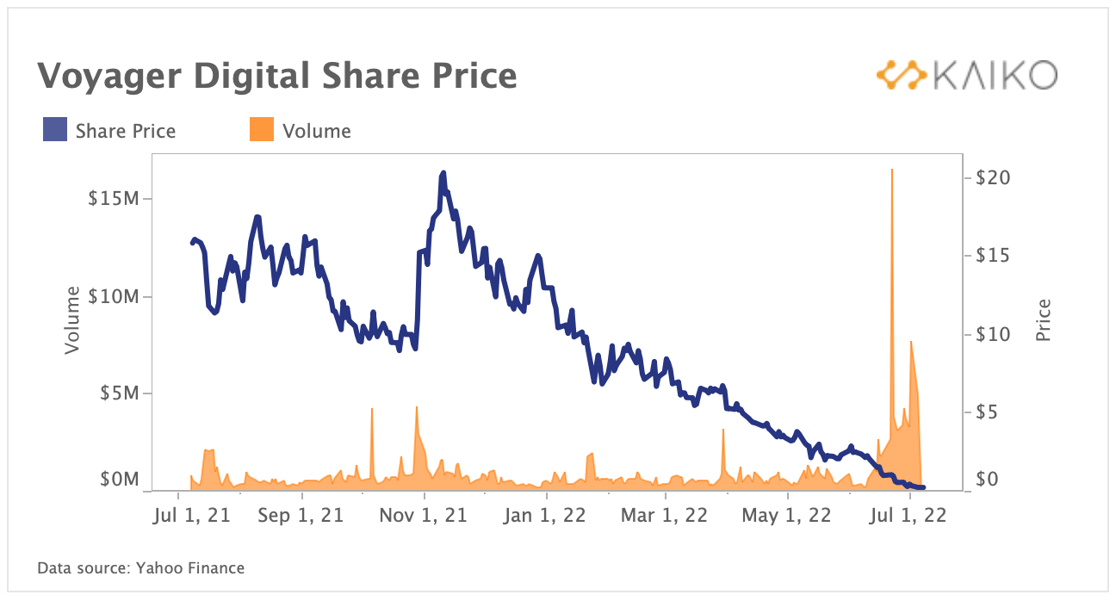

Voyager Digital files for bankruptcy as shares plummet.

Public company Voyager Digital is the latest domino to fall in the crypto credit crisis, filing for chapter 11 bankruptcy last week. The Toronto Stock Exchange soon paused trading for the company's shares, which are down 99% since their peak in March 2021. The lending firm and brokerage blamed their struggles on prolonged volatility and contagion, however it has been rumoured they lent Three Arrows Capital, a hedge fund at the heart of the contagion, $650m with little to no collateral. The bankruptcy filing comes after the broker suspended all activity on the platform and after Alameda Research had extended a $500m line of credit in order to see it through this liquidity crisis. Alameda had also invested $75m and owned 9% of Voyager shares, which look in dire straits in light of the bankruptcy filing.

Bitcoin’s correlation with the U.S. Dollar is falling.

Bitcoin’s correlation with the US Dollar has been on a downward trend over the past year, averaging -.3 in Q2, up from nearly zero a year ago. This has been mirrored by Bitcoin’s rising correlation with tech equities. The U.S. Dollar index (DXY) is up 1.8% last week as the Euro - which accounts for nearly 60% of the index, sank to a 20-year low amid mounting recession fears in Europe. The EUR/USD has been closing on parity, which is an important psychological threshold and if broken, could inject volatility in the market. Overall, the Dollar has outperformed most asset classes YTD, benefiting from safe-haven flows amid global risk aversion.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-2.png?upscale=true&width=1116&upscale=true&name=image%20(6)-2.png)