Trend of the Week: Tether's market cap has plummeted amid a reportedly sharp increase in bearish bets.

Price Movements: BTC dipped below $20k while ETH held steady above $1k as credit contagion continued to roil markets.

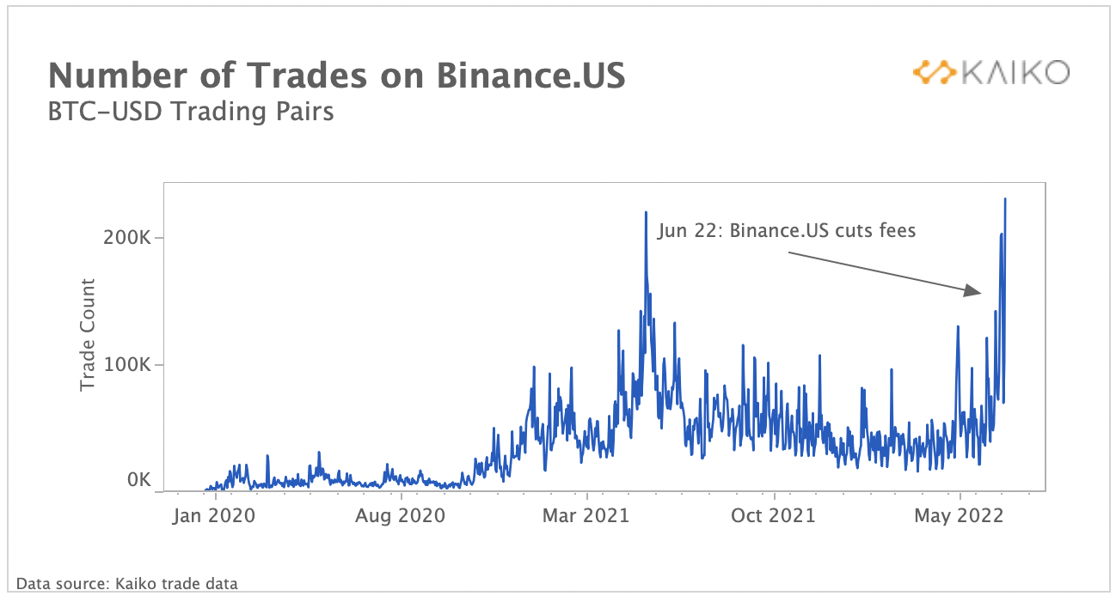

Market Liquidity: Binance.US processed a record number of transactions after eliminating BTC trading fees.

Derivatives: The ratio of inverse to linear perpetual futures has plummeted.

Macro Trends: GBTC shares widen to record discount following ETF rejection.

Trend of the Week

USDT open interest surges following UST collapse, suggesting a rise in bearish bets.

The largest stablecoin by market cap, Tether’s USDT, has seen steady outflows over the past two months with its market cap tumbling by over 20% from $83bn to $64bn. During previous periods of market volatility, USDT often traded at a premium as traders flocked into assets perceived as more stable, however this appears to have changed after Terra’s collapse. USDT has been trading at a continued discount for over 60 days since early May up from a cumulative 48 days during the whole of 2021.

This has fueled speculation that professional traders are massively shorting USDT, doubting the quality of its reserves and anticipating a worsening environment for risk assets. Short traders typically benefit if the value of the asset declines. In the case of USDT, the trade could be highly lucrative as it offers limited downside (USDT can’t go much above $1) but massive upside potential if the peg breaks. Traders have several ways to short Tether: they can either borrow USDT and sell it, hoping to buy it at a lower price in the future, or they can turn to derivatives products such as perpetual futures.

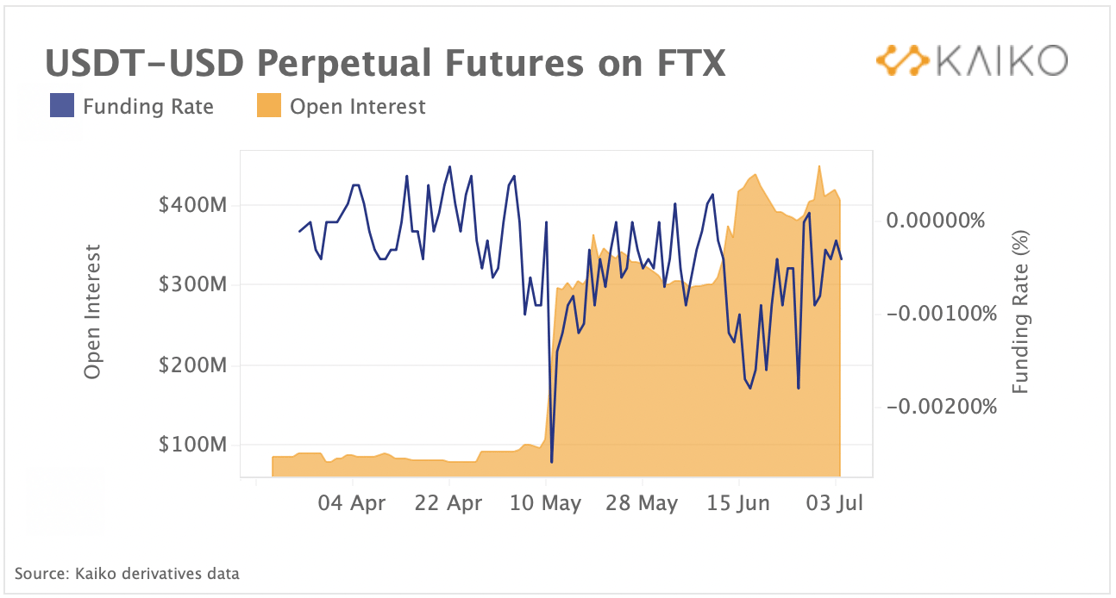

Above we chart the open interest and funding rates of USDT-USD perpetual futures contracts on FTX. Open interest rises if more perpetual futures contracts are entered into, whether long or short. We observe that the amount of open interest has surged three-fold right after Terra’s collapse in May and further spiked in June after Celsius halted withdrawals. To gain an insight into the directionality of these future bets we can look at the funding rates, which should be negative if the majority of bets were short. Funding rates have been mostly negative over the past two months, signalling a bearish bias among traders.

Price Movements

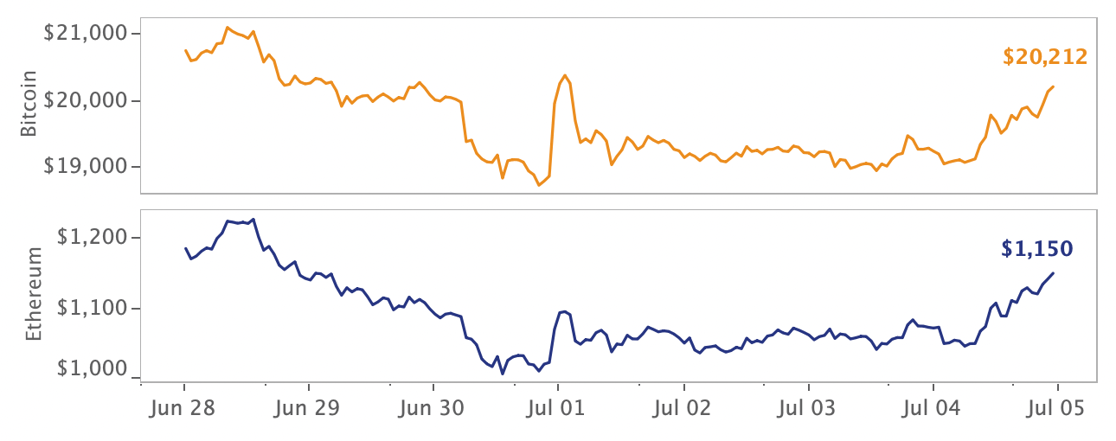

Bitcoin fails to hold above $20k as credit contagion spreads.

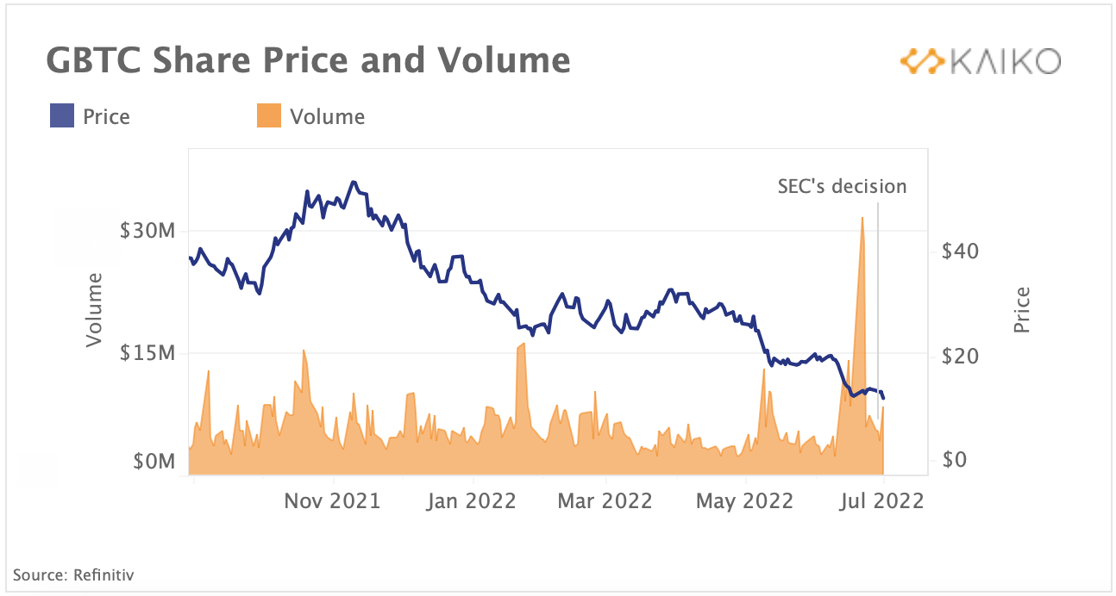

Last week saw the close of Q2, a quarter which was one of the most volatile in crypto's recent history. The industry experienced its own version of a credit crisis as contagion spread across the ecosystem. Over the past week, Voyager Digital and Vauld were the latest lenders to suspend services, Three Arrows Capital filed for bankruptcy and FTX entered into a takeover deal with BlockFi that could be worth up to $240m. Meanwhile, the SEC rejected Grayscale's attempt to convert its Bitcoin Trust into a spot ETF, resulting in the GBTC discount widening to all time highs. Bitcoin closed the month under the key support level of $20k as selling pressure mounted amid a record unwinding of leverage.

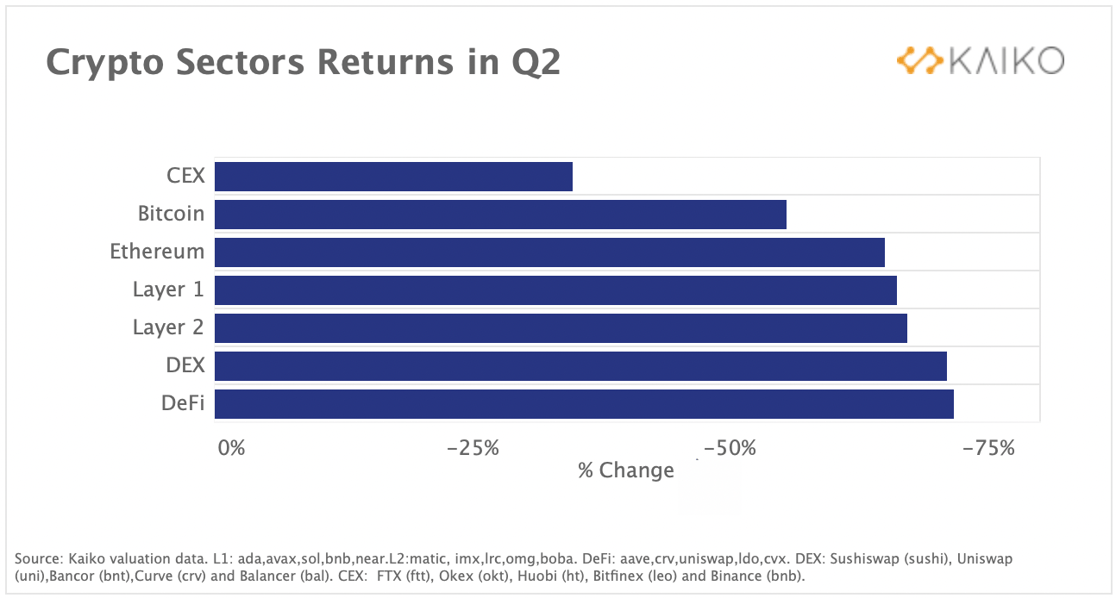

DeFi tokens are the worst performers in Q2.

Despite crypto markets broadly registering one of the most bearish quarters ever, not all sectors have suffered equally. We compare the market performance of five simulated portfolios and observe that DeFi tokens have been the worst performers following the collapse of Terra. Since the start of Q2, the sector has experienced a sharp drop in total value locked. Sector-wise, centralised exchanges have performed better than Bitcoin and Ethereum, bolstered by strong moves by FTX to save distressed crypto companies.

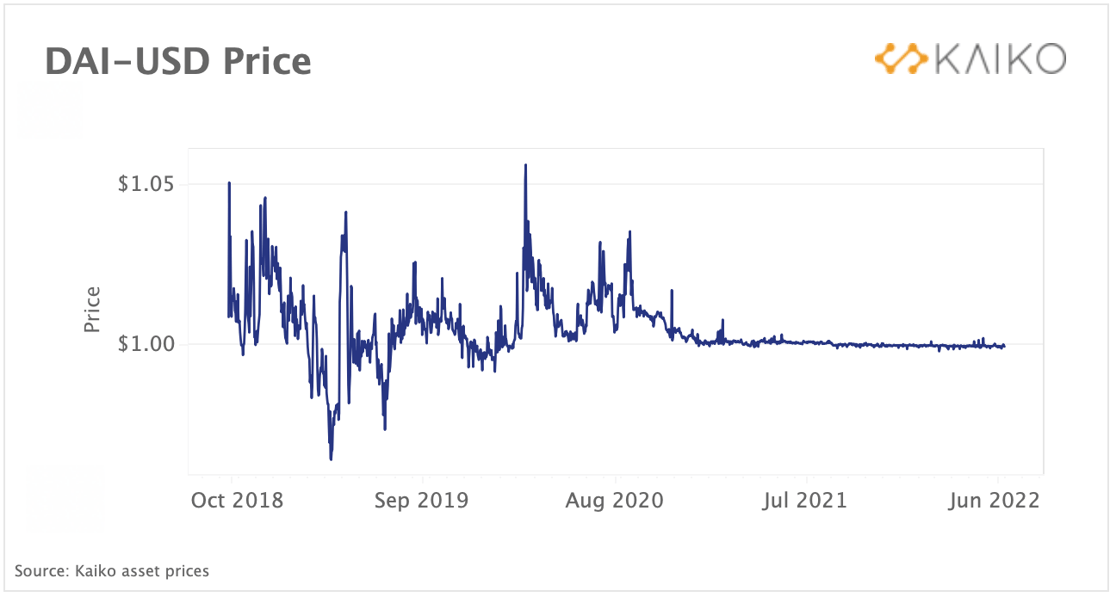

MakerDAO considers US bond investment with DAI treasury.

MakerDAO, the issuer of the decentralized stablecoin DAI, is voting on whether to allocate $500m of their treasury to invest in US Treasury bills and bonds. The governance vote is particularly interesting considering that DAI’s main differentiator from other large stablecoins is the protocol's decentralisation. Adding U.S. government-backed bonds to their treasury would effectively link the decentralized protocol to the centralized financial industry. The vote comes at a time where stability among stablecoins is being prioritized by both issuers and investors. Moving away from a model of a crypto-collateralized stablecoins towards a fiat-backed model is a quick way to ensure stability, but it arguably comes at a cost of decentralisation. As we’ve charted above, DAI has been one of the least volatile stablecoins in recent times, whereas the likes of Tether is trading at a persistent discount since UST's collapse.

Kaiko Market Reports

Data-driven commentary on June's most significant market events

Binance.US processes a record number of trades after fee cut.

The US affiliate of the largest crypto exchange Binance has processed a record number of over 230K trades in early July, exceeding its previous all-time high reached during the May 2021 selloff. The increase comes after the exchange introduced zero-fee trading for Bitcoin on June 22nd. Binance.US's market share of volumes compared with other U.S. exchanges has surged since the fee change from around 5% in early June to 21%.

Coinbase's market share appears to be most affected by the change, losing about 5% of BTC market share. Competition between crypto exchanges is heating up amid falling trade volumes, with Coinbase, Gemini, Bitso and Bybit already announcing layoffs to curb costs. Binance.US's move to cut fees will likely induce other exchanges to introduce their own incentive programs to attract the highly lucrative U.S. market.

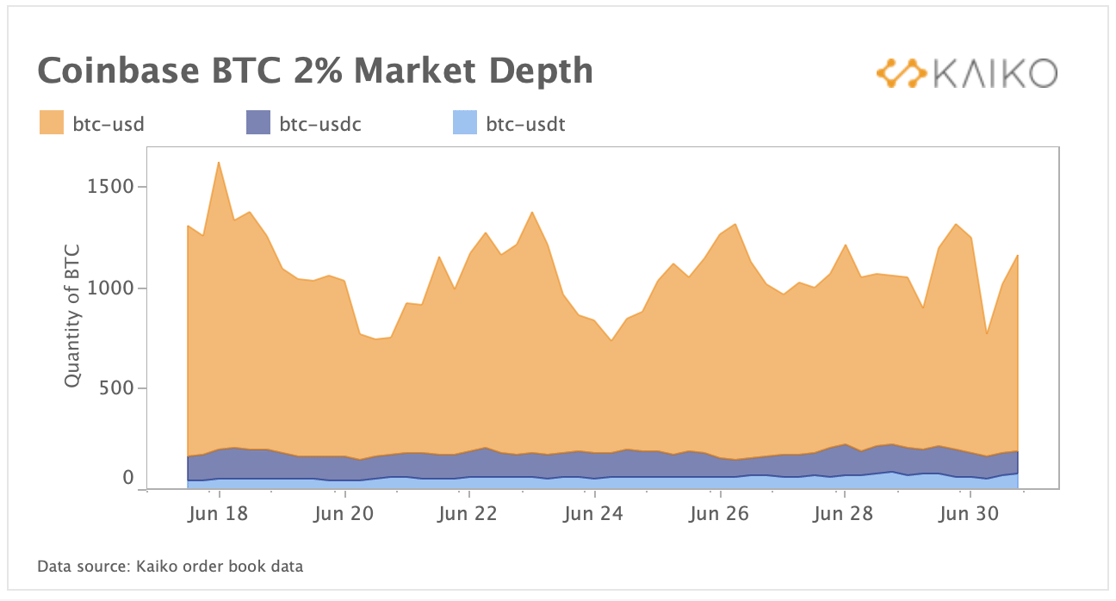

Coinbase unifying USD and USDC order books for deeper liquidity.

Last week, Coinbase announced they would be unifying their USD and USDC order books on July 13th for “deeper liquidity." The move comes as USDC liquidity on Coinbase lags significantly behind USD liquidity, which we can observe in the chart above. We compare the total quantity of BTC on Coinbase's BTC-USD, BTC-USDC, and BTC-USDT order books placed within 2% of the mid price. BTC-USD is by far the most liquid pair, with on average around 1,200 BTC on both the ask and bid side, compared with just 100 BTC on the BTC-USDC order book.

The unification of USD and USDC is likely a tactical move by Coinbase to increase the use of USDC, although it remains unclear how a unification would be impacted by a possible de-pegging event. A unified order book will allow traders without access to USD trading to trade on the same market as those that do have access, a first for crypto.

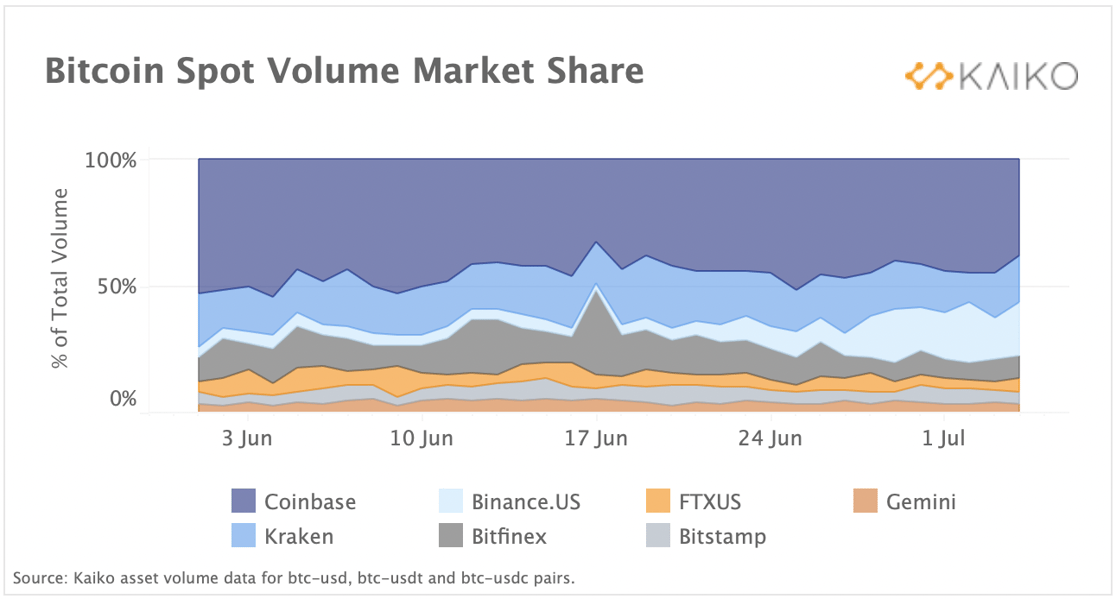

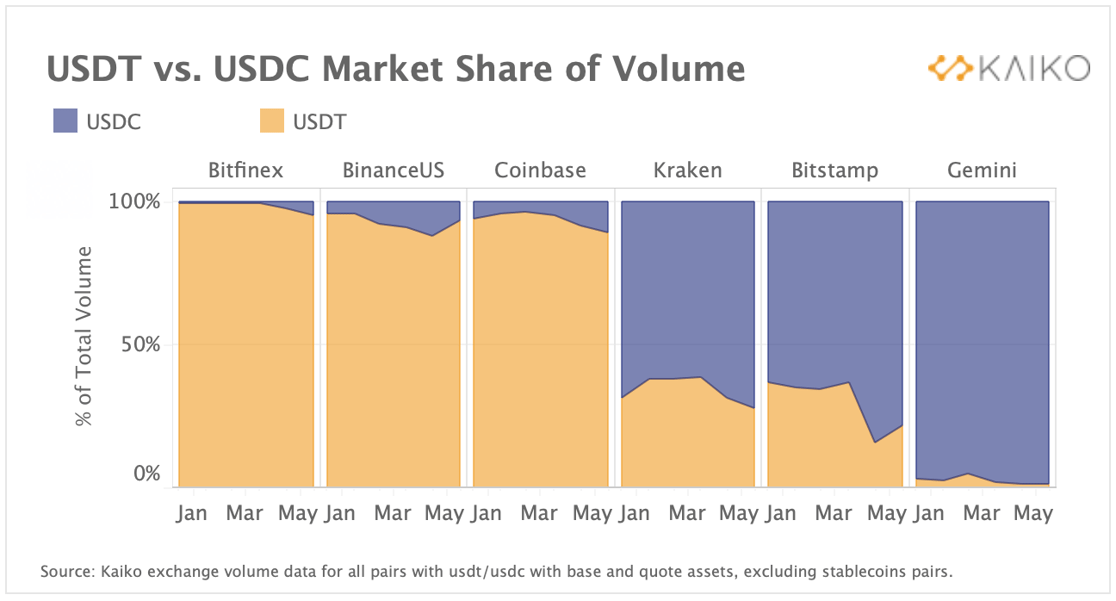

Ever since UST collapsed and USDT began trading at a discount, USDC has experienced a slight increase in market share on regulated exchanges.

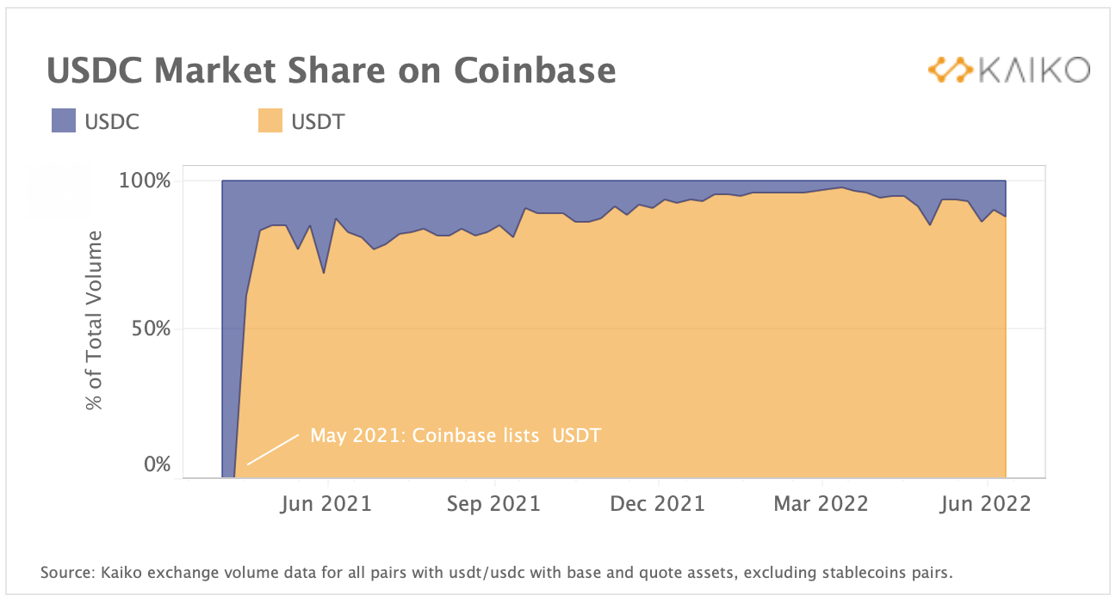

The market share of volume for USDC vs. USDT varies across exchanges: Gemini, Bitstamp, and Kraken all have more USDC volume than USDT, while Bitfinex, BinanceUS and Coinbase all have more USDT volume than USDC. When we zoom in on Coinbase's market share of volume we can see that as soon as USDT was listed on the exchange in May 2021 it almost immediately overtook USDC as the top stablecoin.

That trend has slowly become more pronounced over the year and at the time of writing sits at about 88% in favour of USDT. The unification of order books for USD and USDC is the strongest move we’ve seen from Coinbase to increase adoption of USDC, allowing customers to be paid out interchangeably between the two currencies as well. What is most interesting about the unification is the expanded access traders around the world will have to the exchange's deep BTC-USD liquidity.

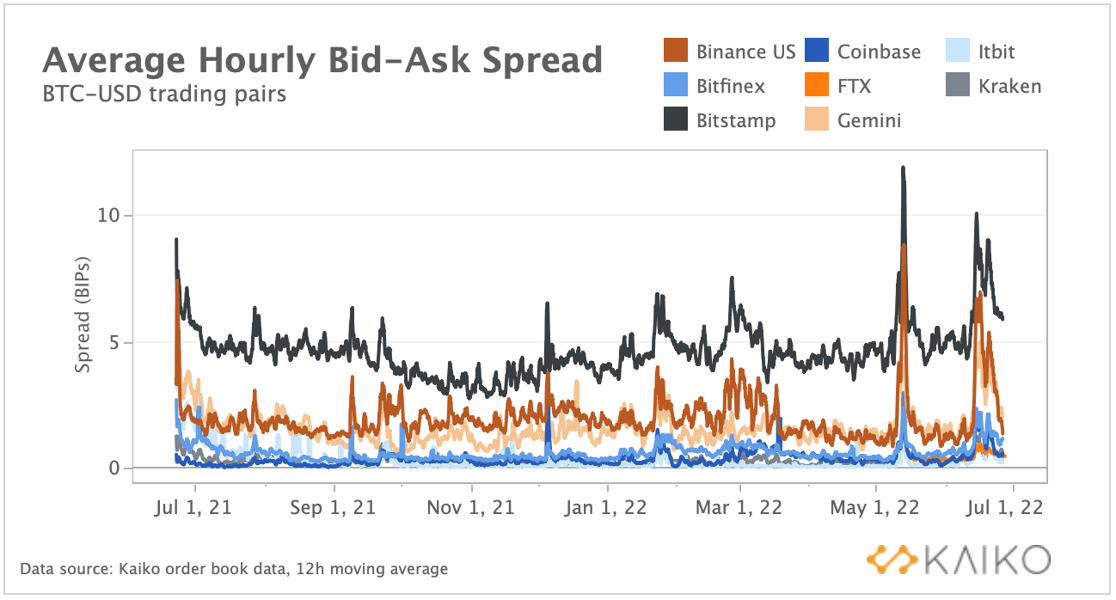

Spreads reach second widest level in over a year

Bid ask spreads across exchanges reached their second widest levels in over a year as volatility picked up heading into the end of Q2. Unsurprisingly, the two largest spikes in spreads coincided with the two biggest volatility events of the year, namely the Terra collapse in mid-May and the liquidity crisis that started to unfold mid-June. Typically, widening spreads are a sign of deteriorating liquidity for a trading pair. However, spreads have dropped sharply over the past week in a sign that market makers could be anticipating a cool down in volatility.

Derivatives

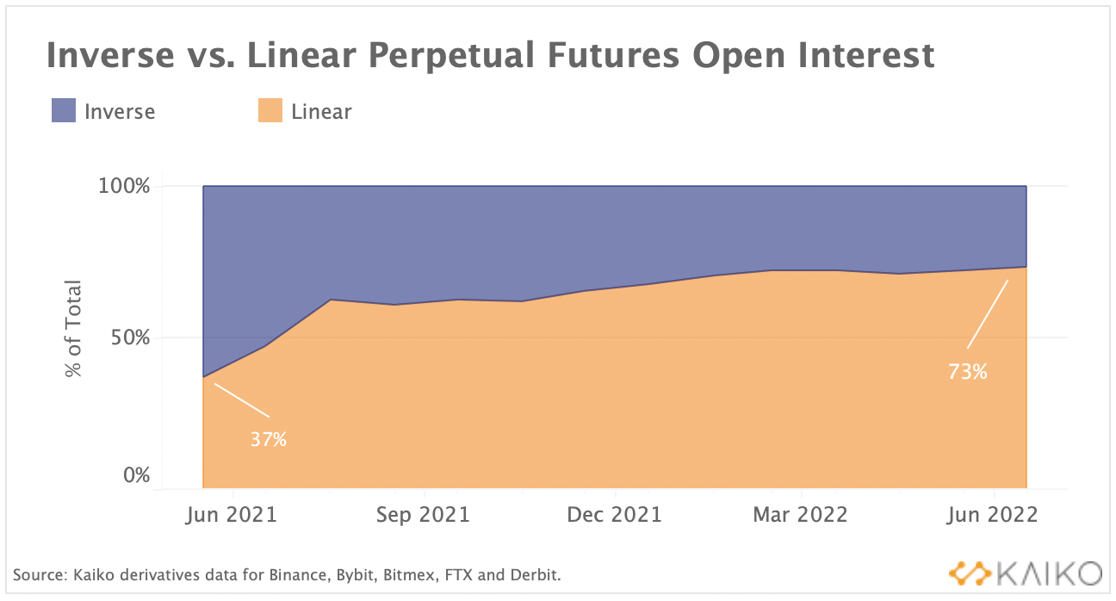

Market share of linear derivatives is rising.

With Bitcoin and most altcoins down over 70% since November’s all-time highs, traders are increasingly preferring linear contracts for their crypto futures, as opposed to inverse. Inverse contracts are margined and settled in the base currency and the value of the margin varies with the asset’s price movements. Linear contracts are margined with USD or stablecoins, thus the value of collateral does not shift with price volatility. While inverse contracts are more profitable when Bitcoin’s price is rising, they are riskier when prices are falling.

Above, we chart the market share of open interest for Bitcoin inverse vs. linear perpetual futures contracts on five exchanges. We can observe that the share of linear contracts has nearly doubled from 37% to 73% of total open interest over the past year. The trend suggests that traders are more cautious amid rising macro volatility.

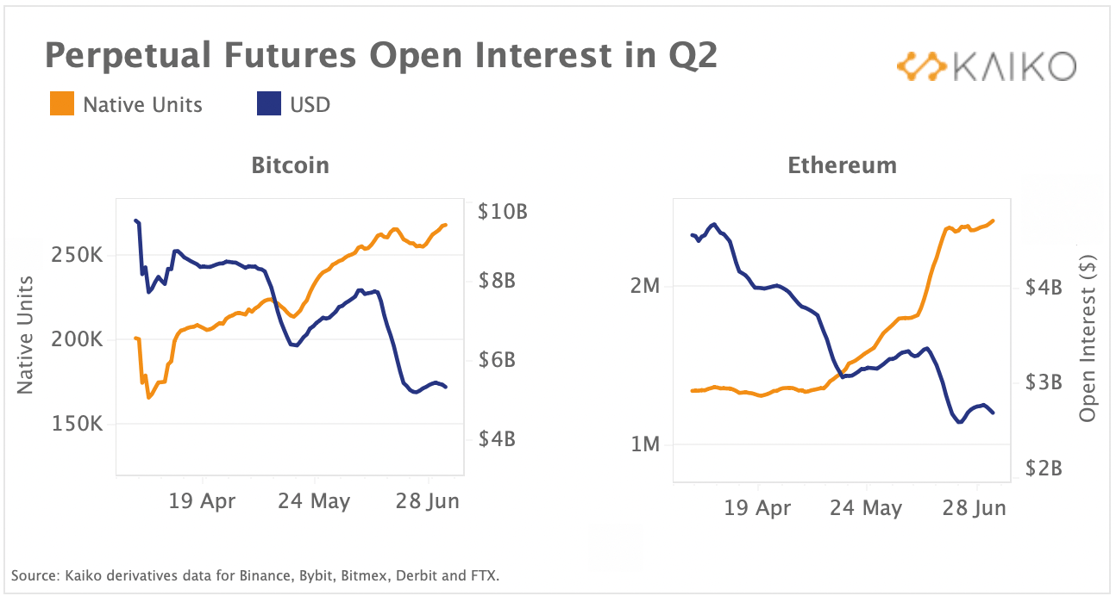

Open interest expressed in native units is surging, while USD-denominated open interest is falling.

Both Bitcoin and Ethereum USD-denominated open interest for perpetual futures are down by around 40% in the second quarter of the year following a sharp drop in spot prices and risk sentiment. By contrast, the amount of Bitcoin and Ethereum open interest expressed in native units has risen, by 50% and 80% respectively as the effect of downward price action is removed. This suggests that traders continue to steadily purchase derivatives contracts, although the recent price crashes have caused the USD value of these contracts to fall. Funding rates (not charted) have been mostly negative since Celsius network’s withdrawal freeze, after oscillating around neutral in April and May.

Macro Trends

GBTC discount widens following SEC’s ruling.

Last week, the US securities watchdog (SEC) rejected Grayscale’s application to convert its Grayscale Bitcoin Trust’s (GBTC) into a physically backed ETF, citing potential fraud and manipulation in the underlying bitcoin market and the role of Tether’s USDT in the broader crypto ecosystem. GBTC’s share prices halved in June while trade volumes remained lacklustre, before spiking to an 18-month high on June 21st. Grayscale sued the SEC almost immediately following the decision. The conversion was expected to help reduce the so-called GBTC discount but once the decision to deny the application was announced, the discount widened even further to all time highs of 34%. The discount refers to the difference between GBTC’s share price and the price of its underlying bitcoin holdings as traded on cryptocurrency exchanges. SEC’s decision comes days after one of the largest investors in GBTC, crypto hedge fund 3 Arrows Capital, was ordered into liquidation.

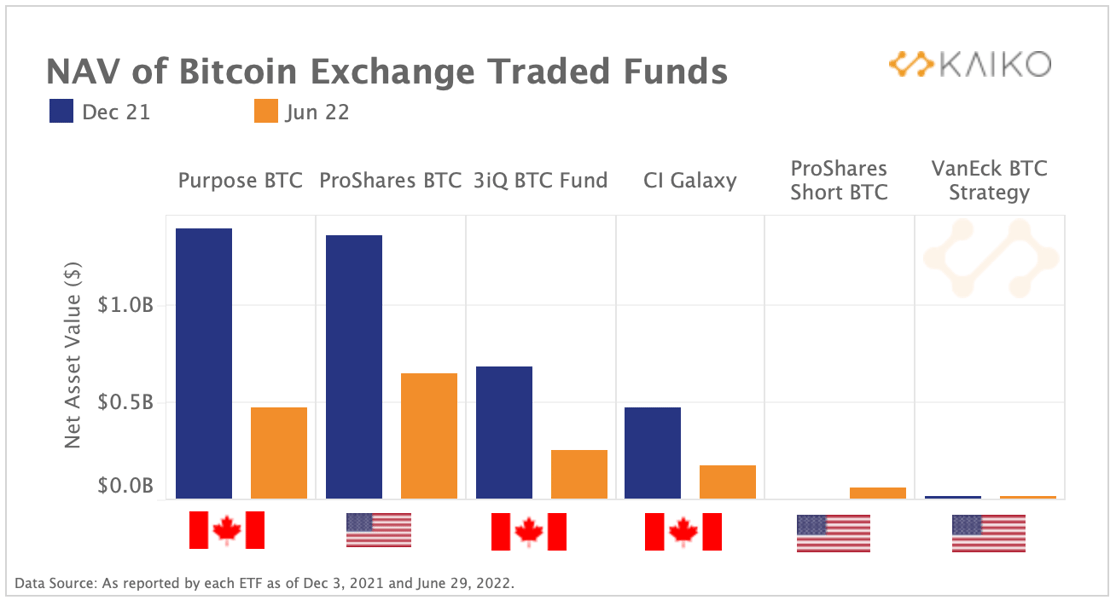

Bitcoin-linked investment products see outflows.

Bitcoin-linked ETFs have seen significant outflows over the past few months as investors continued de-risking their portfolio. Overall, Canadian spot-backed ETFs registered a larger decline in their net asset value (NAV) between December 2021 and June 2022 relative to futures-backed instruments. The Canadian Purpose Bitcoin ETF had its AUM decline the most, plummeting from over $1.3b to around $460m. Falling demand for GBTC coupled with bearish market conditions have benefited the newly launched ProShares Short Bitcoin ETF (BITI) which offers a way to gain short exposure to bitcoin via futures contracts. However, despite BITI becoming the second largest ETF on US markets just two weeks after its launch, it is still well behind its Canadian and U.S. counterparts in terms of assets under management.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.