In this week's Deep Dive, we examine how XRP has fared since the U.S. SEC brought a case against Ripple and its top executives and what this could tell us about future enforcement actions. In case you missed it, Kaiko announced the launch of Price Rates, a suite of 50 clean cryptocurrency prices, enabling investors to accurately assess the value of their holdings and trade with confidence.

The current U.S. Securities and Exchange Commission Chairman has repeatedly stated that he believes most cryptocurrencies are securities, stating this month that of “the nearly 10,000 tokens in the crypto market, I believe the vast majority are securities… the investing public is buying or selling crypto security tokens because they’re expecting profits derived from the efforts of others in a common enterprise.”

Whatever one may think of this statement, it’s important to consider what could happen in a worst case scenario in which the SEC pursues enforcement action against a growing number of projects. Luckily we have an example in Ripple and XRP, which have been stuck in security/non-security purgatory since late 2020.

XRP functions much like a crypto Rorschach Test, in which someone’s opinion of the token depends on their exposure to XRP, time in the industry, and opinion on the SEC’s crypto policy. But let’s leave these judgements behind and instead look at how XRP has reacted since the SEC’s case against Ripple and what this could portend for future actions.

XRP and Ripple

Founded in 2012, Ripple is a money transfer service that leverages a native cryptocurrency, XRP, for fiat currency conversions. The token is designed to be used as a decentralized unit of exchange for Ripple’s cross-border payments blockchain network. But like many tokens issued by projects in the industry, many XRP holders treat it as an investment. In December 2020, the SEC alleged that Ripple had engaged in a $1.3bn unregistered securities offering of XRP.

The news caused XRP’s price to instantly crash with several regulatory-compliant exchanges de-listing the token to avoid potential conflict. Interestingly, the token bounced back in the 2021 bull run, and today remains the 6th largest cryptocurrency by market cap.

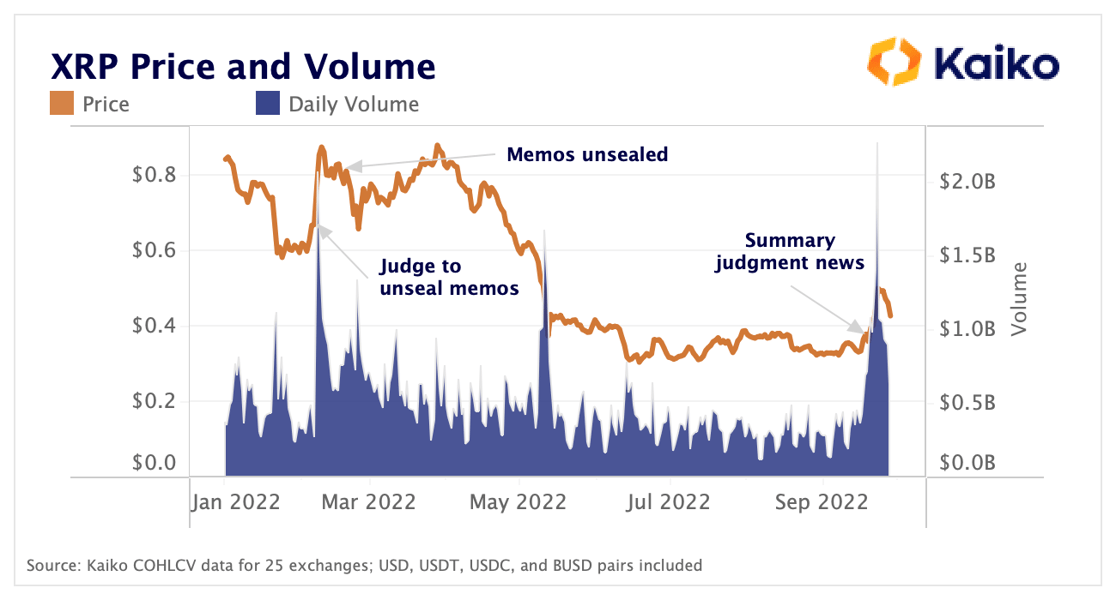

Since the SEC case began, XRP’s main idiosyncratic price catalysts have come in the form of court updates. Last week it was reported that Ripple and the SEC requested a summary judgment in the SEC’s case against Ripple. The summary judgment would allow the two parties to skip the trial phase and allow the judge to make a ruling; if it goes forward, we can expect a decision in the first half of next year. The news caused XRP’s price to surge and trade volume to hit yearly highs.

Looking back, legal updates have been at the core of XRP’s trading activity over the past year. In February, a judge ruled to unseal memos sent to Ripple from its outside counsel in 2012. The memos revealed that Perkins Coie LLP attorneys had “advised Ripple not to sell the proposed coins, as various conditions could subject them to being regulated as securities or commodities. A second memo… suggested that XRP may not be considered to be a security under federal law, but cautioned there was a risk the Securities and Exchange Commission would see things differently.”

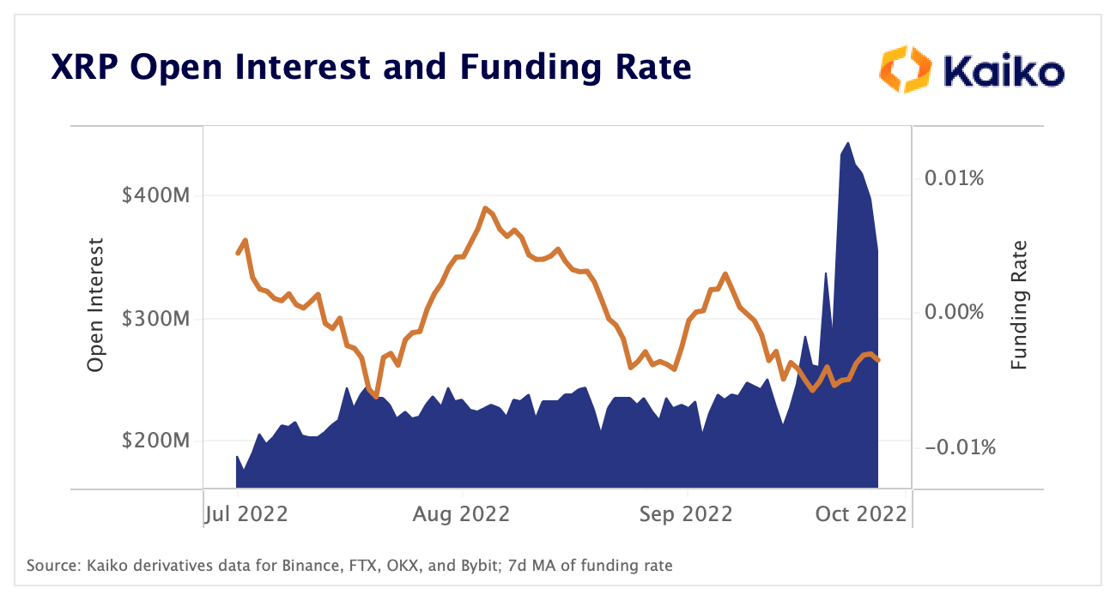

Along with strong spot market activity following the summary judgment news, there has been a massive spike in open interest, doubling from $211mn to $445mn in under a week. The funding rate has remained negative, suggesting that these new positions were skewed towards the short side.

So, traders clearly still like to speculate on XRP, and it seems that there is a good amount of alpha available to traders who have a good understanding of the U.S. legal system and/or are keeping up with court proceedings.

But this doesn’t really answer the question of what befalls a token that enters the SEC’s proverbial doghouse. So let’s move on to a more thorough breakdown of volumes.

Volumes

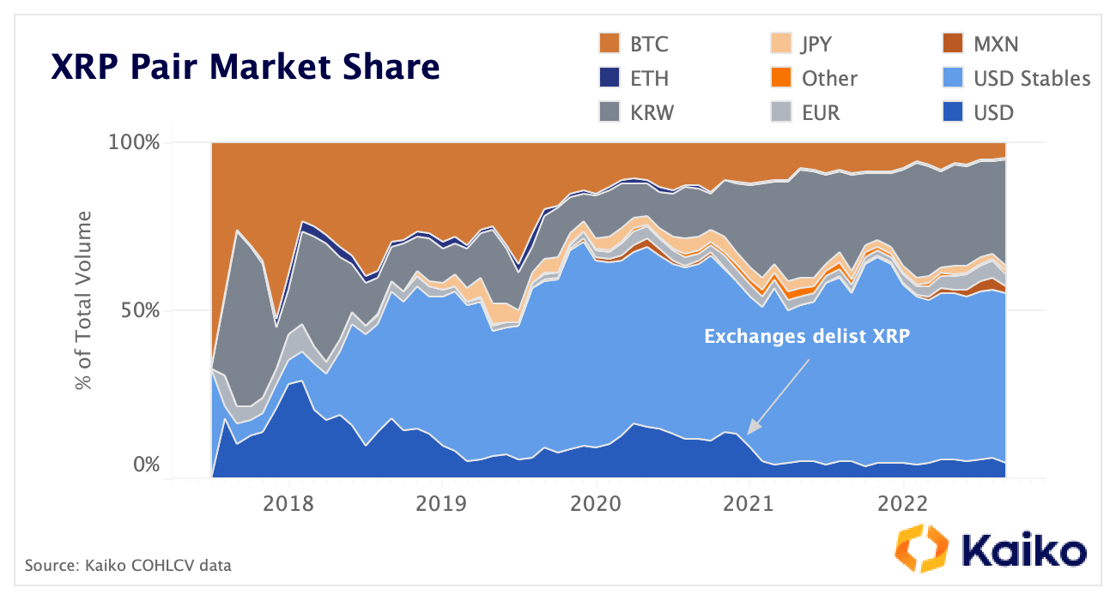

Following the SEC revealing its case against Ripple, exchanges – including Coinbase, Crypto.com, and OKCoin – began to delist XRP in January 2021, while Kraken disallowed U.S. users from trading the token.

The delisting from U.S. exchanges had a clear cooling effect on USD volumes, which have been flat at 5% since early 2021. USD stablecoins, too, have been nearly flat since the delisting. As with most older tokens, BTC used to be a significant trading pair but has since shrunk to just 5% of volumes. But what is most interesting to note are the other fiat currencies – especially the Euro and Mexican Peso – have grown their market share, with the two accounting for nearly 10% of volume in August.

XRP in particular has found a niche in Latin American markets due to Ripple’s partnership with Bitso, one of the larger exchanges in the region. Bitso uses XRP to make cross-border transfers of USD and MXN in minutes. While activity from this service is not reflected on spot markets, we can use spot as a gauge to understand the breakdown of XRP holders.

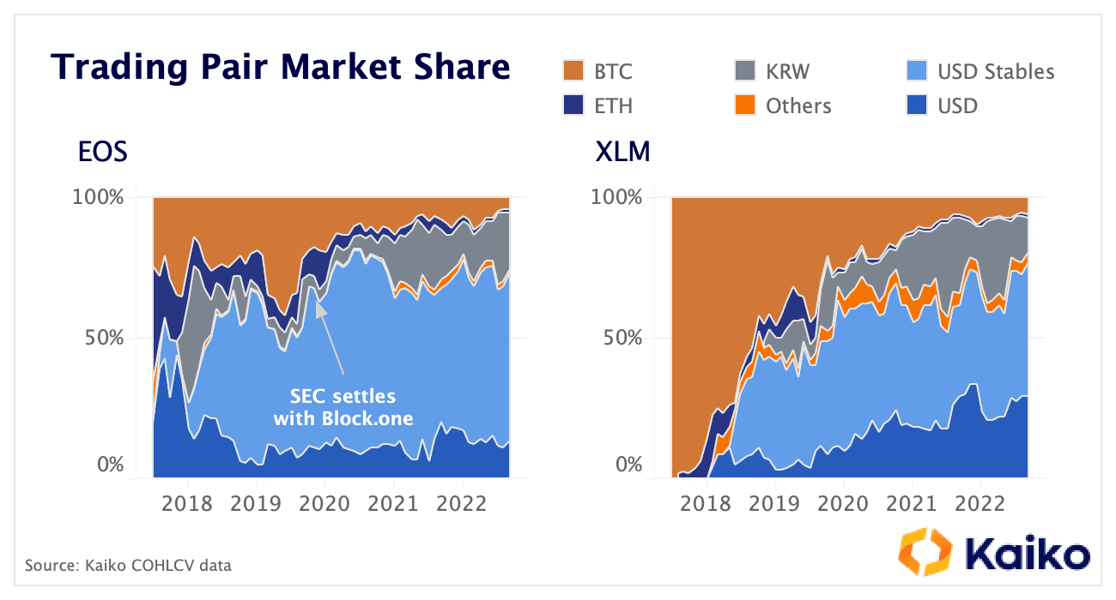

To give this more context, let’s look at the tokens EOS and XLM. EOS because it was previously involved in a dustup with the SEC and XLM because it’s nearly as old as XRP and is intended to address similar frictions, namely cross-border transfers.

Again, USD stablecoins are dominant for both tokens and BTC’s market share has decreased. But look at the market share of all non-USD, non-KRW fiat pairs (it’s the tiny bright orange sliver). For EOS, it was just 2.21% in August. For XLM, it was 4.3%. The Mexican Peso alone accounted for 3.5% of XRP’s volume in August, and its total non-USD, non-KRW market share is about 12%. While still small, XRP’s volumes are meaningfully more decentralized than similar tokens.

Now let’s take a look at liquidity for XRP to see how it compares to tokens of similar market caps. One might then assume that XRP’s USD (and associated stablecoin) liquidity is much worse than comparable tokens due to swirling regulatory uncertainty. But this isn’t the case.

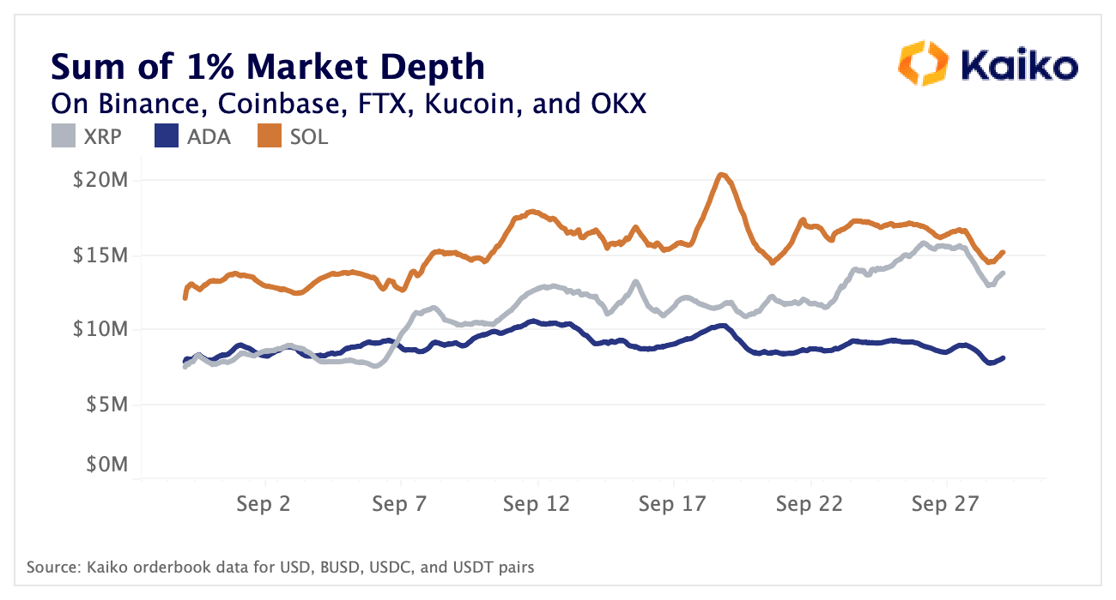

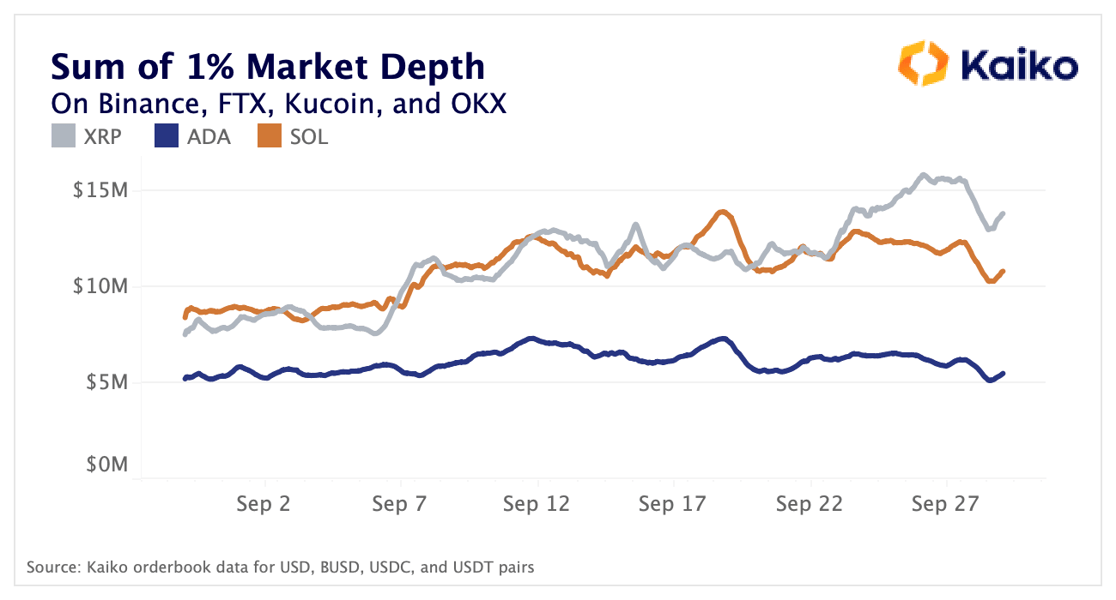

Compared to two of the tokens closest to XRP by market cap, XRP is nearly as liquid as SOL and significantly more liquid than ADA.This chart was created by summing the 1% market depth across five of the world’s largest exchanges – Binance, Coinbase, FTX, Kucoin, and OKX – but here’s the kicker: XRP isn’t listed on Coinbase. So even with this disadvantage, XRP is comparable. If we remove Coinbase, XRP is $3mn more liquid than SOL within 1% depth.

XRP’s depth has also been steadily increasing throughout September. This closely follows the increase in open interest observed on derivatives markets and surging volumes on spot markets, suggesting traders and market makers anticipate volatility.

Conclusion

So what has the SEC’s case against Ripple done to XRP? It stymied USD’s growing dominance as a trading pair, allowing other currencies to gain market share. For any decentralized currency, and especially one that’s focused on improving cross-border transfers, diversity of fiat trading pairs is a good thing, provided it doesn’t fragment liquidity. While USD volume remains dominant, we can observe growing market share of MXN and EUR activity. For now, liquidity for XRP is still quite good. We don’t know how the SEC’s case against Ripple will pan out, but XRP has thus far proved that the SEC has the ability to make it harder for U.S. persons to buy a token, but not the ability to kill a project.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

.png?upscale=true&width=1116&upscale=true&name=Copy%20of%20Medium%20Banners%20(3).png)