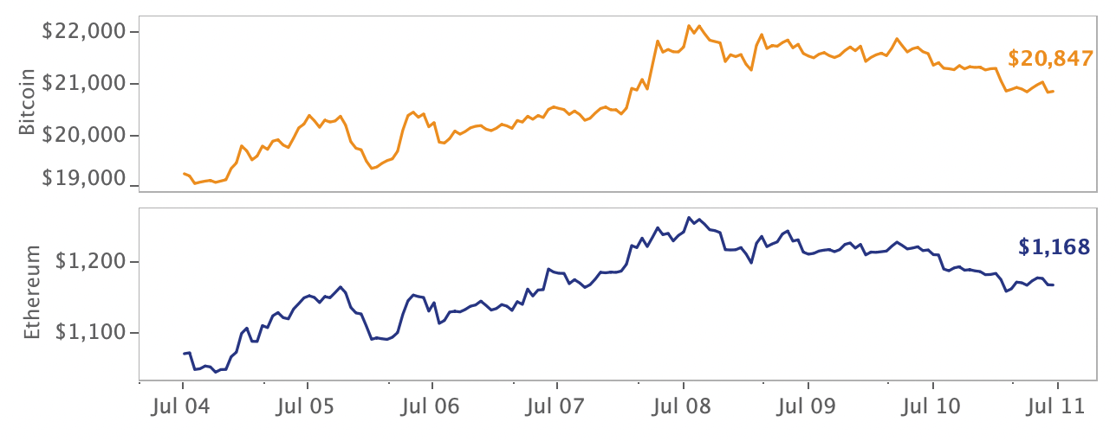

Price Movements: BTC staged a strong comeback early Monday morning, trading above $22k for the first time in 10 days. ETH is up 30% over the last week.

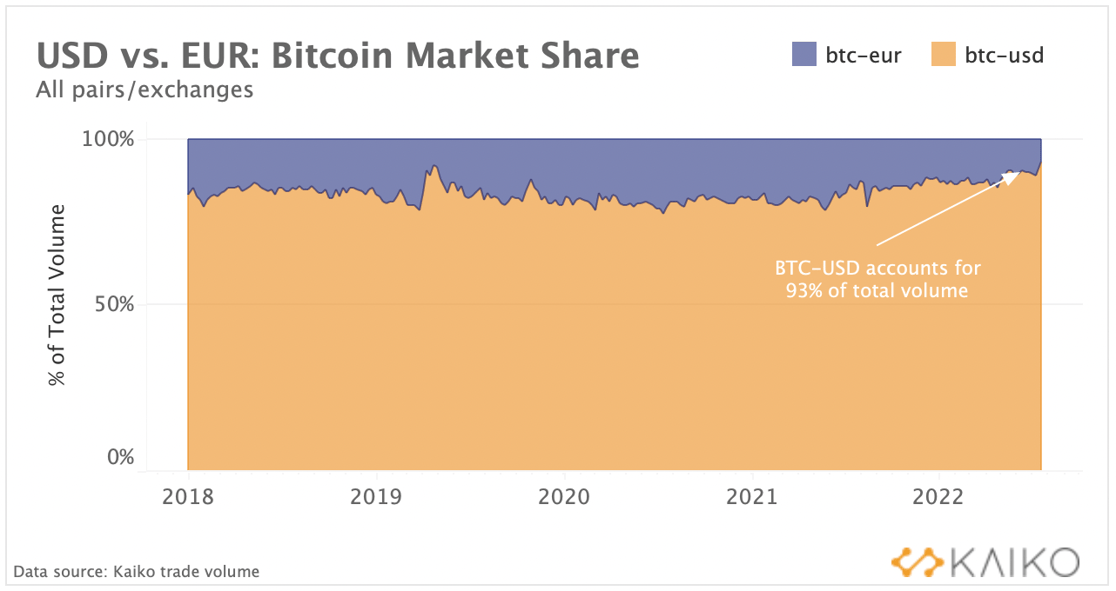

Market Liquidity: BTC-EUR trade volume fell relative to BTC-USD as the Euro reached parity with the Dollar.

Derivatives: BTC open interest climbed and funding rates flipped positive as market sentiment improved.

Macro Trends: U.S. consumer inflation accelerated to 9.1% in June, a new four-decade high.

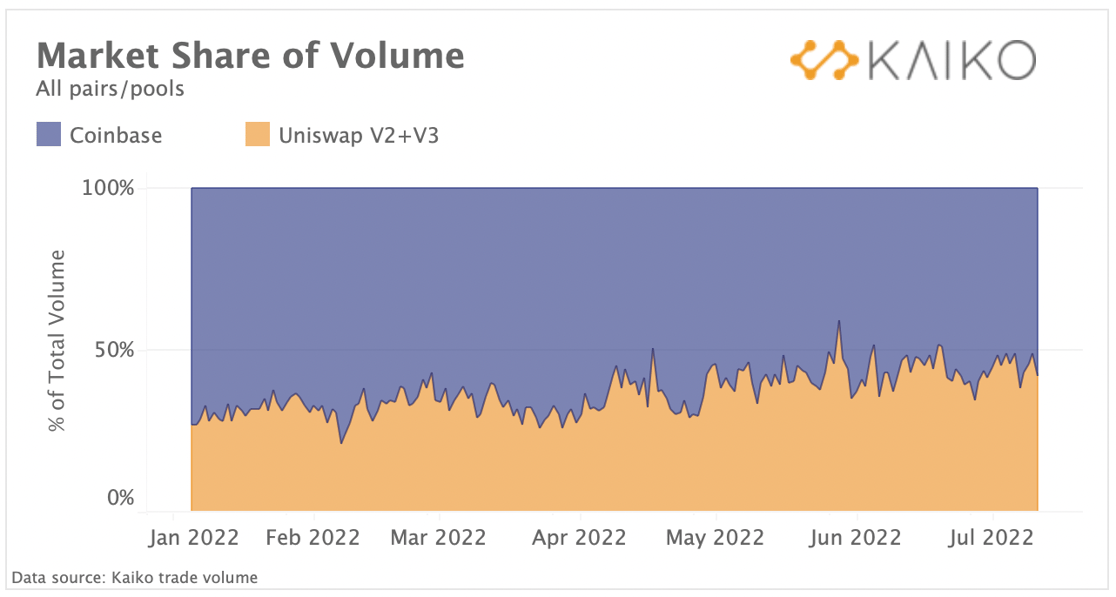

Uniswap and Coinbase daily trade volume is nearly equal.

Since January 2022, Uniswap's market share of volume relative to Coinbase's has surged from 27% to nearly 50%. This strong shift in market structure comes as Ethereum network transaction fees drop to their lowest levels since 2020. Decentralized exchanges had an initial surge in popularity during DeFi summer (2020) before Ethereum gas fees surged, making DEXs expensive to use with a trade often costing over $100. Uniswap's relative increase in volumes could also be related to the growing role that DEXs play in providing liquidity for stablecoin swaps, particularly important following TerraUSD's collapse and Tether's continuing discount to the Dollar. Today, stablecoin pools have the highest total value locked across DEXs and stablecoin trade volumes are comparable to that on CEXs.

Yet, all market trends should be viewed in context. Although Uniswap's volumes are now nearly equal to Coinbase's, overall Ethereum-based DEX volumes are still minuscule compared with global CEX volumes.

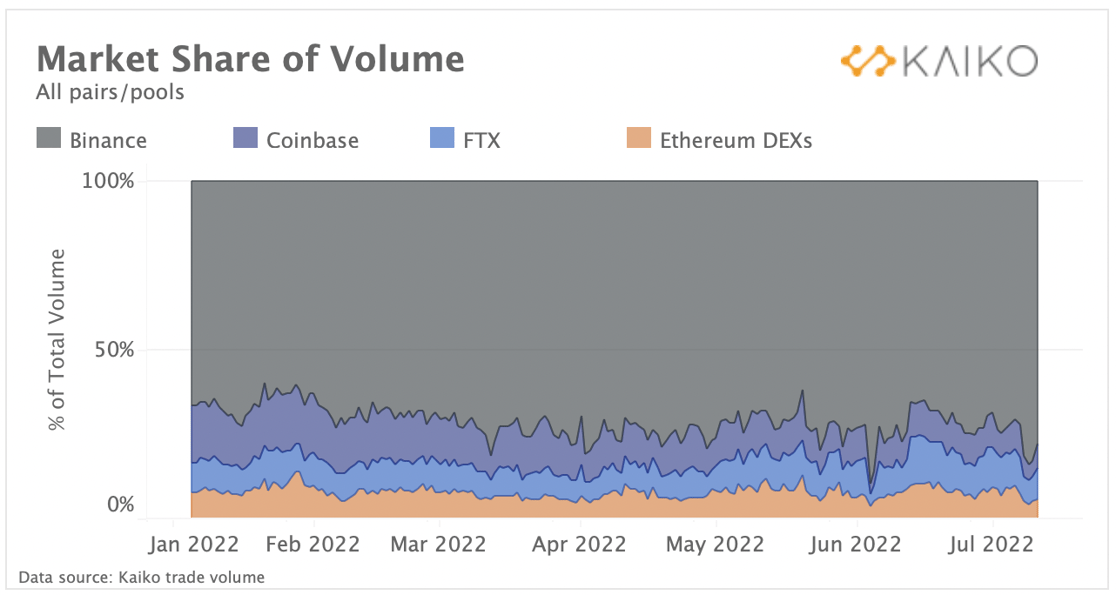

DEXs accounted for just 8% of total volume in June compared with the top three exchanges (Binance, FTX, and Coinbase), a sign that cryptocurrency market structure continues to be dominated by centralized exchanges (which themselves are heavily dominated by Binance). Within the DEX category, Uniswap V3 accounts for between 80-90% of all daily volume, although Curve has recently captured a growing percentage of market share.

For more on the latest DEX trends, tune into research director Clara Medalie's presentation at EthCC here on July 21st 1:30pm GMT+2.

Crypto winter took a momentary pause over the weekend after markets staged a respectable relief rally. ETH significantly outperformed BTC after news broke that the network's merge to proof-of-stake was projected for September 19th, which investors interpreted as a bullish signal. Meanwhile, the Celsius saga took a new turn after the beleaguered lender finally filed for bankruptcy, revealing more than 100,000 creditors and that the company is owed more than $439 million from a private lending platform. Finally, Uniswap lost over $8 million worth of ETH in a phishing attack and the Euro hit 1:1 parity with the US dollar for the first time in 20 years.

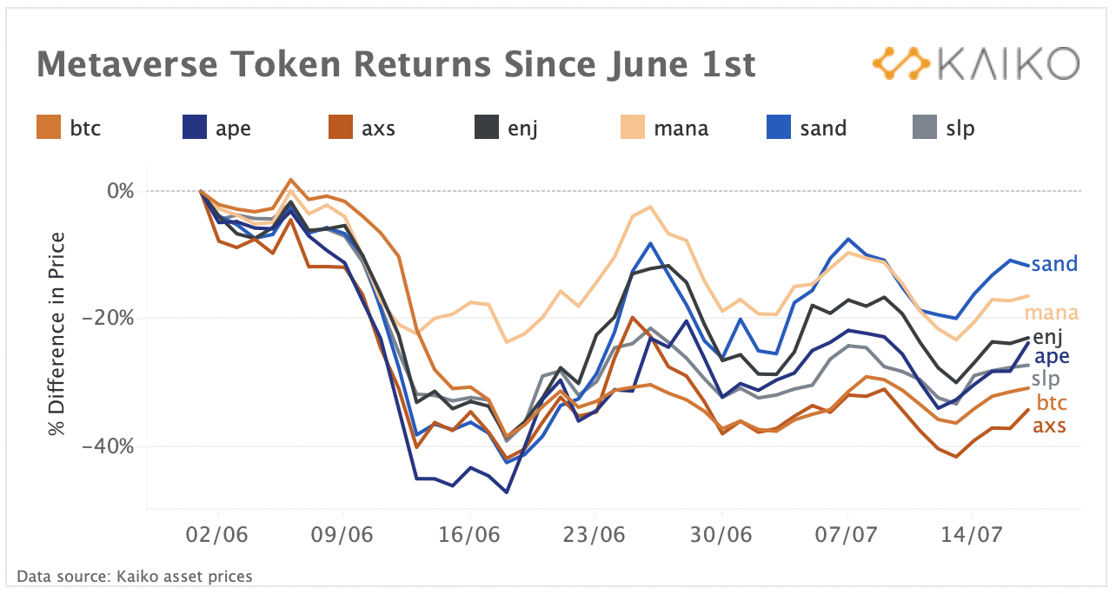

Axie Infinity's AXS token is worst performer.

Metaverse and play-to-earn projects have been one of the hardest hit sectors in crypto over the last couple of months. Play-to-earn games leverage in-game tokens that are often given as rewards, such as Decentraland’s MANA, Axie Infinity’s SLP and AXS tokens, and the Sandbox’s SAND. The destruction in value of these rewards over the last couple of months has far reaching consequences for in-game economies, which in turn affect real world players.

AXS is the worst performer, down more than 34% since June 1st following a devastating $600m hack of the game’s network in April. SAND, MANA, ENJ, and APE are also each down double digits, although BTC remains a worse performer. Axie’s largest user base is in the Philippines, with weekly users at one point peaking above 2.7 million, although this number has since plummeted to a few hundred thousand. The sharp drop in value highlights the struggle that play-to-earn games have in retaining users during a market downturn.

Kaiko Market Reports

Data-driven commentary on June's most significant market events

The share of euro-denominated bitcoin trade volume has declined to its lowest level since 2016 as the EUR/USD hit parity last week for the first time in two decades. Despite the Dollar remaining the preferred quote asset for fiat-to-crypto trading, BTC-EUR has maintained a stable share of around 20% over the past five years. However, this appears to have changed after the May 2021 market crash with BTC-EUR market share steadily declining to just 7%. The trend suggests suggests investors increasingly prefer to trade in Dollars amid growing risk aversion and FX volatility.

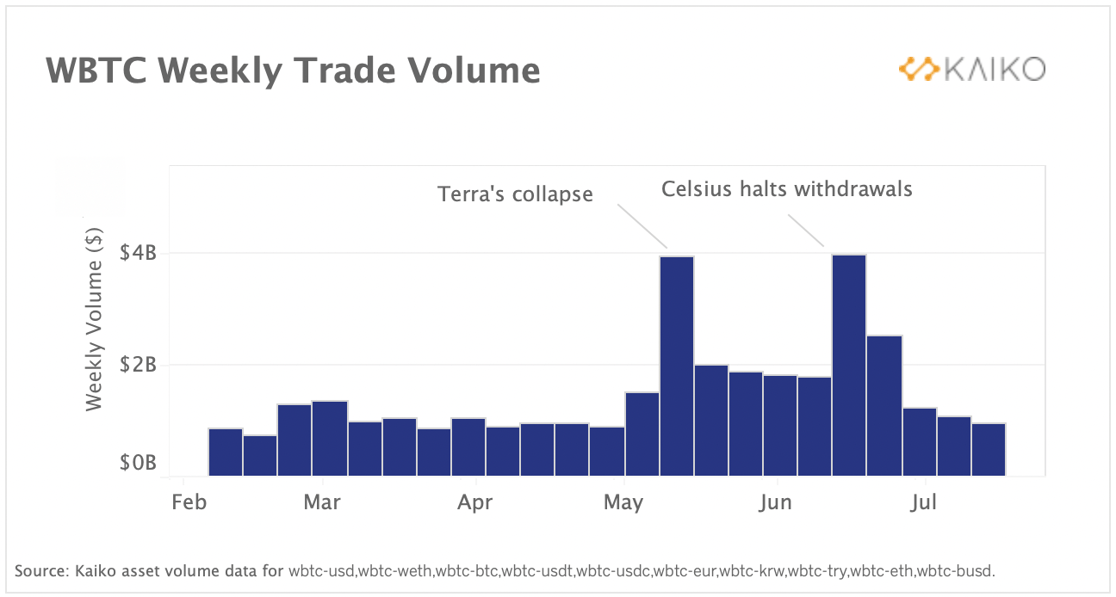

wBTC volumes broke all time highs in June.

Weekly trade volume of wrapped bitcoin (wBTC) on centralized exchanges hit an all-time high of $4bn after crypto lender Celsius halted withdrawals in early June. wBTC is an ERC-20 token that represents one bitcoin on the Ethereum blockchain, enabling BTC holders to participate in popular DeFi applications. Celsius in particular benefitted from yields that could be earned by depositing wBTC into DeFi lending protocols, which is why wBTC volumes are relevant to pay attention to right now. Celsius recently paid off its debts to the largest DeFi lenders - Aave, Maker, and Compound - which has released over $1bn of collateral, mainly in wBTC and stETH. The problem is that wBTC is not a very liquid market (much like stETH), meaning Celsius could have a difficult time exchanging their wBTC holdings for BTC without experiencing high slippage. Metrics such as market depth suggest that wBTC markets on centralized exchanges are highly illiquid (check out our deep dive on the topic here).

wBTC holders likely anticipated the coming liquidity problems back in June after Celsius’ crypto holdings became highly scrutinized, causing a spike in volumes on centralized exchanges. wBTC trade volumes have reset to their levels from earlier this year, which suggests Celsius has not yet liquidated their holdings.

Coinbase merges BTC-USD and BTC-USDC order books.

Coinbase officially mothballed its BTC-USDC pair on July 13. The pair had significantly less liquidity than the BTC-USD pair, with just 63 BTC compared to 300 BTC within 0.5% of the mid price at the time of its discontinuation; within 1% of the mid price the figure was 80 BTC and 800 BTC, respectively. It is unclear whether Coinbase has merged the two order books yet, as market depth for the BTC-USD pair has trended upwards but has not broken above its normal range. Even if all liquidity from the BTC-USDC pair was moved to the BTC-USD pair, it would have a relatively small effect on market depth.

Derivatives

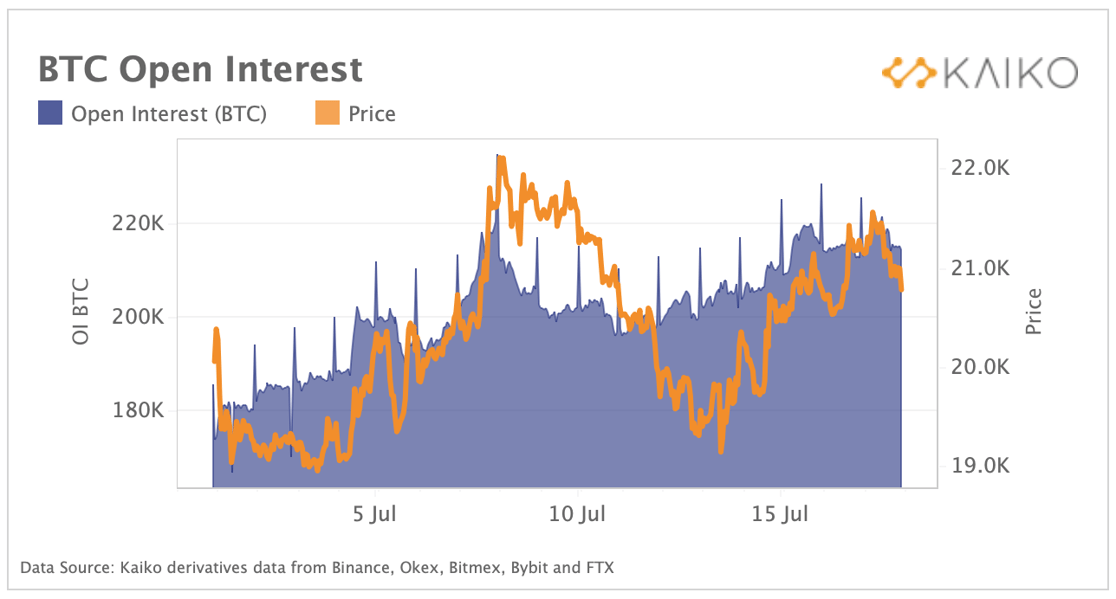

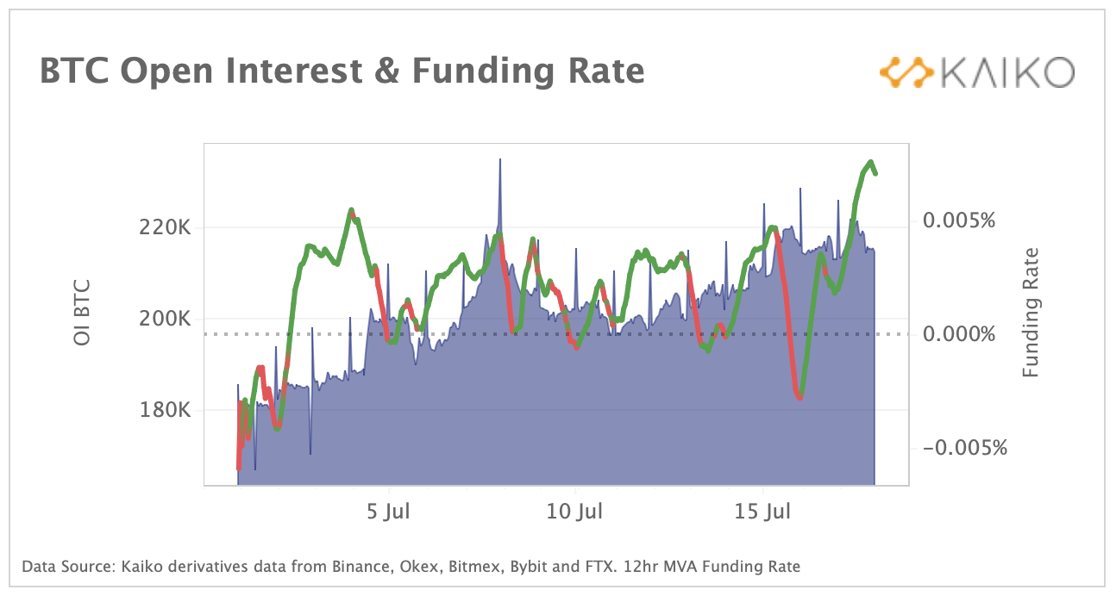

BTC open interest climbs as funding rates turn positive.

Open Interest denominated in BTC has increased roughly 20% since July 1st as new capital floods into the Bitcoin futures markets. One particularly noteworthy trend is how closely the rise in open interest tracked the price action of Bitcoin as the two appeared to move in lockstep at the start of last week. This would perhaps indicate that the recent upwards move in Bitcoin’s price was largely driven by perpetual futures markets as investors piled into new positions. A large buildup in open interest usually results in increased volatility because leveraged positions in futures markets can get wiped out in either direction. In order to get a better sense of whether these new positions are investors trying to time the bottom, or investors taking up short positions in anticipation of further contagion, we can look at funding rates to determine the directionality of these bets.

Interestingly, funding rates have been grinding upwards in tandem with a rising level of open interest as futures market sentiment shifts positive. This would seem to indicate that the majority of new positions being entered into are long positions and help explain why we’ve seen a so-called relief rally in the last week or so. With such a buildup in open interest, the next move in funding rates and price will be crucial as the market looks primed for some short term volatility.

Macro Trends

US inflation beats estimates, boosting rate hike bets.

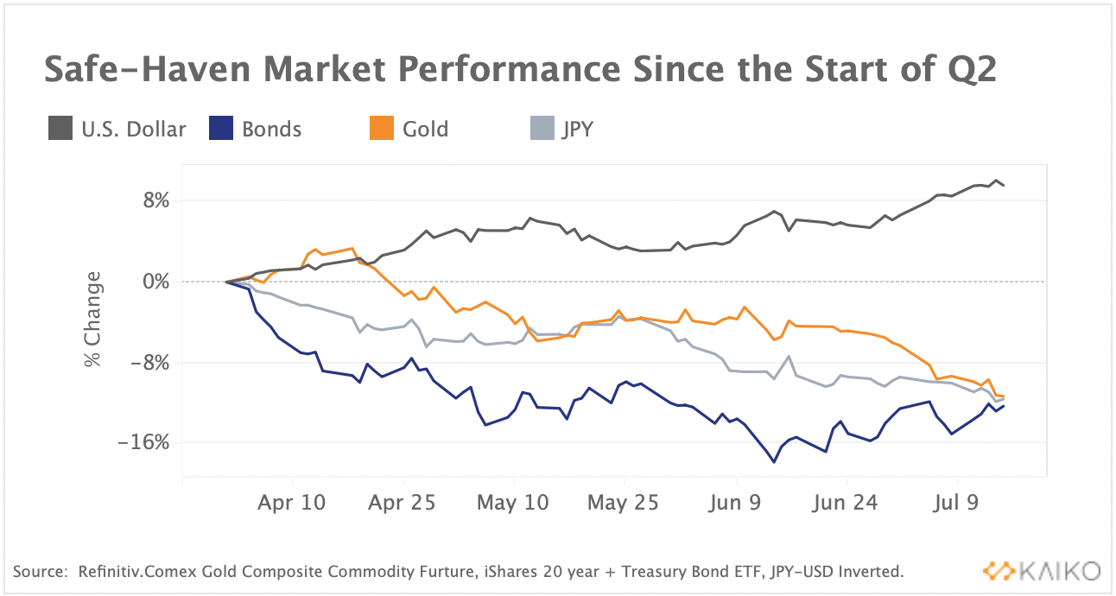

The US Dollar continued strengthening against its peers last week with the EUR/USD hitting parity for the first time in two decades. The Dollar index (DXY) which measures the performance of the greenback against its peers is up more than 12% so far this year while most other safe-haven assets are down double-digits. The greenback has managed to attract safe-haven flows due to a combination of aggressive Fed tightening and its status as a reserve currency. Meanwhile, bonds and gold have trended downwards since the start of April.

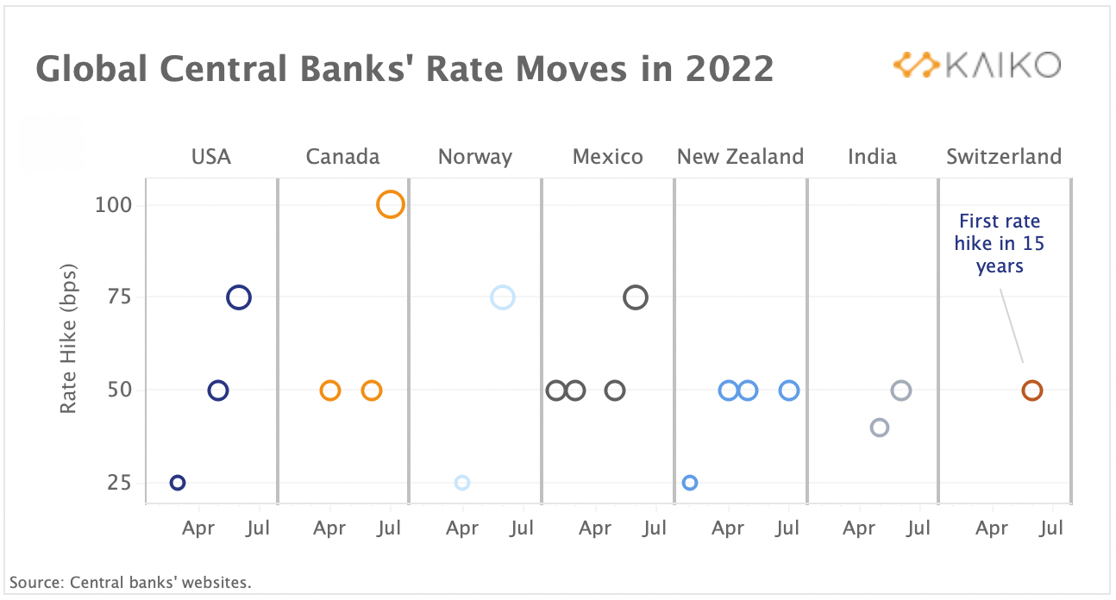

The Dollar continued its record rally right as the U.S. consumer price inflation numbers revealed an acceleration to 9.1%, beating economist’s expectations and triggering a sharp repricing in Fed rates expectations. The Fed's move will be closely watched by other major central banks, which have already sped up rate hikes as well (charted below).

Odds for a supersized 100bps hike at the July FOMC meeting spiked to 86%, up from just 7% before the inflation print. In the US, the Fed has already sped up the pace of monetary policy tightening rising rates by 75bps last month, instead of the initially planned 50bps move. This has put pressure on other central banks to follow suit, with the Bank of Canada hiking rates by 100bps last week.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-3.png?upscale=true&width=1116&upscale=true&name=image%20(6)-3.png)