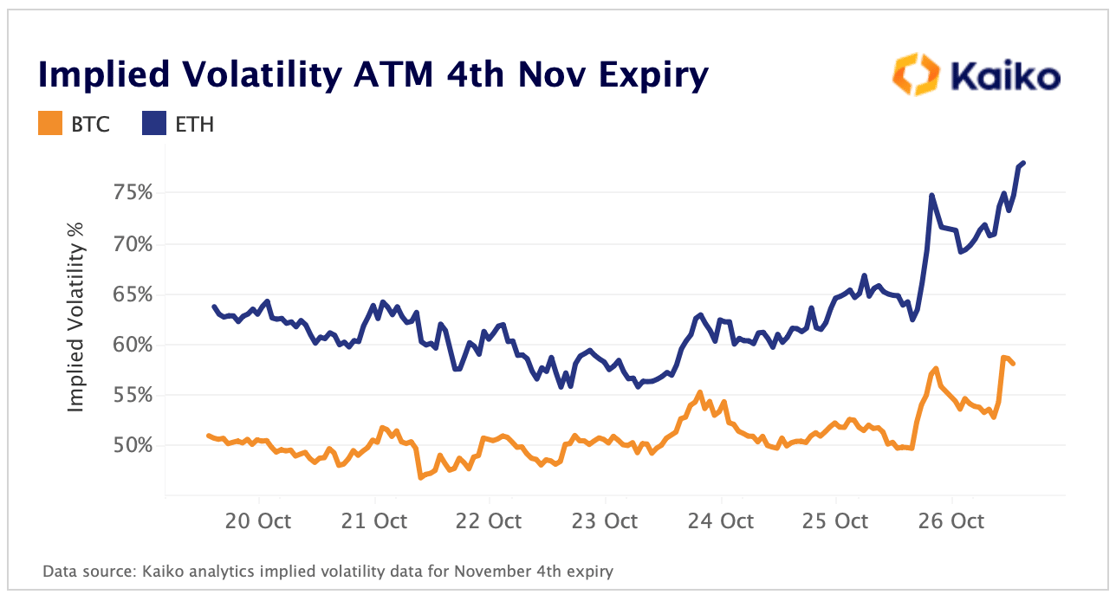

Implied volatility spikes after months of stagnant prices.

The volatility that crypto has been missing for months finally returned after ETH rallied a whopping 17% and BTC 6% week-on-week, which stands in sharp contrast to the continued tech stock sell-off. The strong volatility was reflected in options markets by a spike in implied volatility for BTC and ETH options. When IV increases, options are more valuable and thus become more expensive. Implied volatility gives an insight into how much volatility investors are expecting in the markets and the higher the IV, the more expensive the option. When looking at the November 4th expiry, ETH implied volatility rose from a low of 56% to 78%, outpacing BTC implied volatility which rose from lows of 47% to highs of 59%. With an expiry one week away, the options market is expecting ETH to have significantly higher volatility during that period.

Implied volatility is a fundamental data type for crypto options traders. We are pleased to launch the industry's first implied volatility smiles for BTC and ETH, providing IV for any expiry and strike price with our transparent and data-driven methodology.

Most crypto assets closed Sunday night with strongly positive returns, but nothing compares to Dogecoin's performance. DOGE is up +100% in just seven days with a market capitalization now greater than $16 billion, placing the memecoin in the top 10 largest crypto assets. Strong price momentum emerged as Elon Musk, a vocal DOGE enthusiast, finalized his $44bn takeover of Twitter, which included a $500mn contribution from Binance. In other industry news, the CEO of BitMEX stepped down, MakerDAO approved a proposal to place $1.6bn in Coinbase’s custody, and Apple implemented controversial rules for NFT purchases.

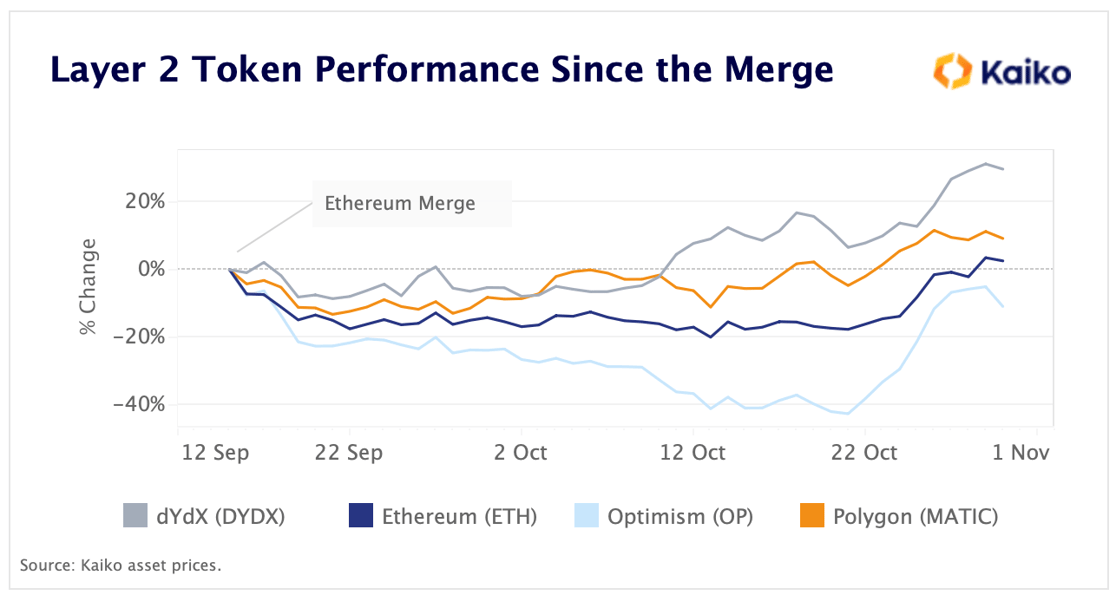

Layer 2 activity heats up six weeks post-Merge.

We are six weeks out from the Merge and Ethereum Layer 2 scaling activity is stronger than ever. Last week, zkSync, one of the buzziest Ethereum scaling solutions, went live on mainnet with a "Baby Alpha" launch. Investors are taking note, with tokens for Layer 2 projects rebounding strongly since the Merge. dYdX’s DYDX token and Polygon’s MATIC have spiked by 30% and 9% since September 15. While Ethereum’s transition to proof-of-stake is just the first step towards a meaningful improvement in scalability, it should boost the bull case for Layer 2s built on top of Ethereum - benefiting from the mainnet security while offering faster throughput. L2 TVL has risen by 40% since the start of Q3.

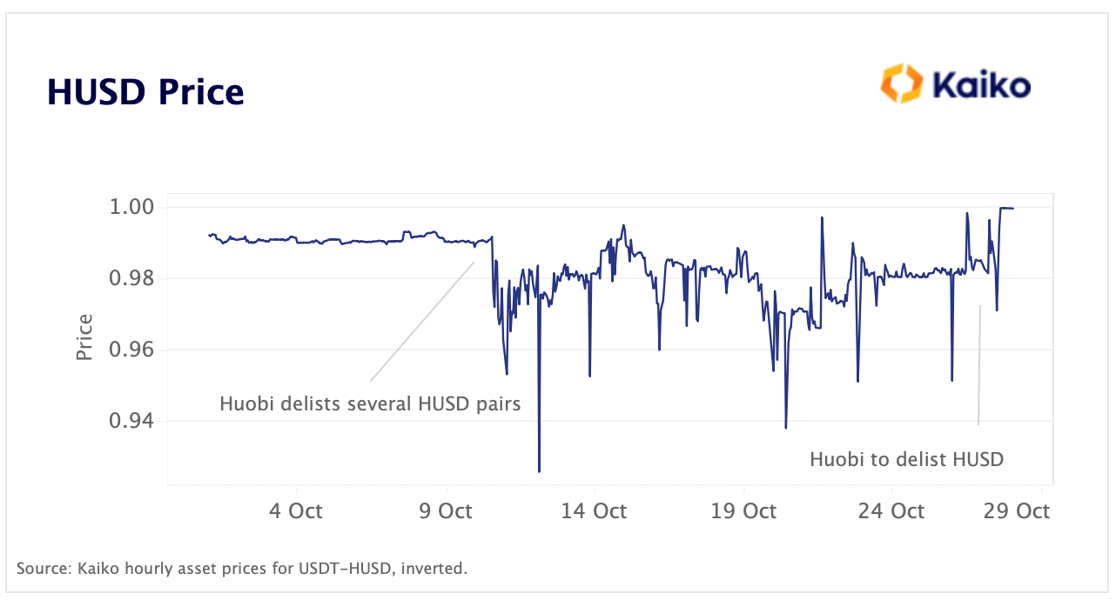

Huobi de-lists HUSD stablecoin.

"Alt" stablecoins are struggling as USDT, USDC, and BUSD increasingly dominate market activity. Last week, Huobi announced they would de-list the exchange's native HUSD stablecoin. HUSD denominated 58 trading pairs on the exchange, but had volumes magnitudes lower than Tether. HUSD de-pegged in early October when Huobi de-listed 21 HUSD trading pairs, at one point dropping below .93. On October 28, Huobi finalized the de-listing, and will convert all HUSD tokens into USDT at a 1-to-1 rate. Near Protocol also recently announced that it would wind down its algorithmic stablecoin USN after it temporarily became under-collateralized.

APT token launch provides case study in price discovery.

The Aptos network’s native token APT was launched on October 19 amid heavy criticism of the project, which we covered last week. This week, we wanted to closer examine the token’s price immediately after listing, which provides interesting insights into the price discovery process. APT had never before traded on an open market, and the initial price at listing on an exchange was determined by the price levels at which market makers place their bids and asks. Not every exchange lists a token at the exact same moment and not every data provider is able to collect, normalize, and list market data for a new token at the same pace, which is why the initial prices for a token can vary drastically.

On FTX and Bybit, APT pairs were trading below $10 immediately after listing. The two pairs on Binance, APT-BUSD and APT-USDT, traded nearly identically and at a higher price level than the other exchanges. At 1:05am UTC, just 5 minutes after listing, differences between exchanges had been arbitraged away.

Market Liquidity

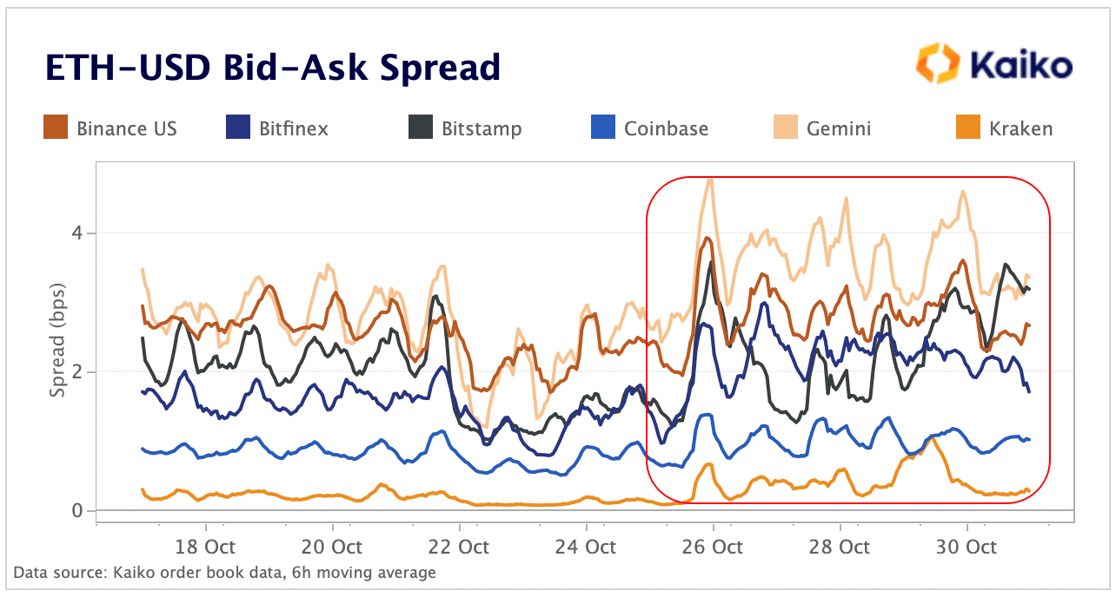

ETH volatility triggers automatic widening of spreads.

Just a bit of volatility can "spread like a contagion" across cryptocurrency markets, triggering market maker algorithms that automatically widen spreads (the mechanics of which are explained in this great twitter thread). ETH soared 7% in a single minute last week, causing ETH-USD spreads across exchanges to spike and remain volatile over the weekend. Altcoin liquidity was also affected, despite price volatility lagging behind ETH.

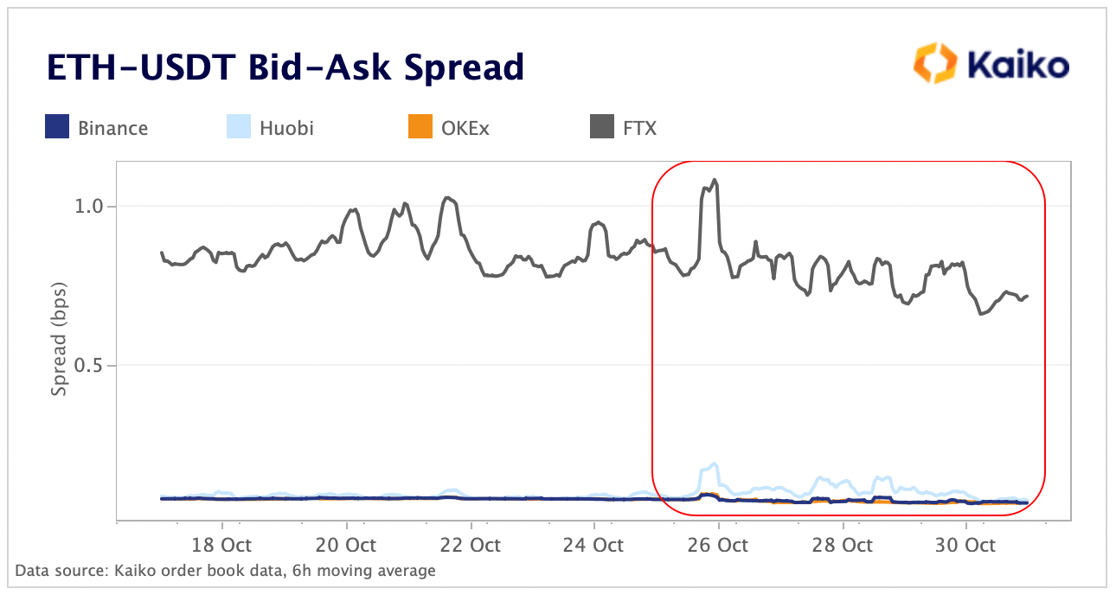

While ETH-USD liquidity has remained volatile, ETH-USDT spreads barely suffered a dent during the price movements, with market makers on the most liquid exchanges maintaining spreads of less than 1bp. Spreads on Binance, Huobi and Okex remained stable at less than .01bp, barely budging as markets soared.

On FTX, spreads actually improved, dropping from the .8bp range to .7. There was a tiny spike in spreads on Binance and Okex from .07 to .08bps, which quickly corrected. Liquidity is highly interconnected in crypto, governed by market maker algorithms that automatically adjust bids and asks, which can exacerbate price movements and increase correlations between assets.

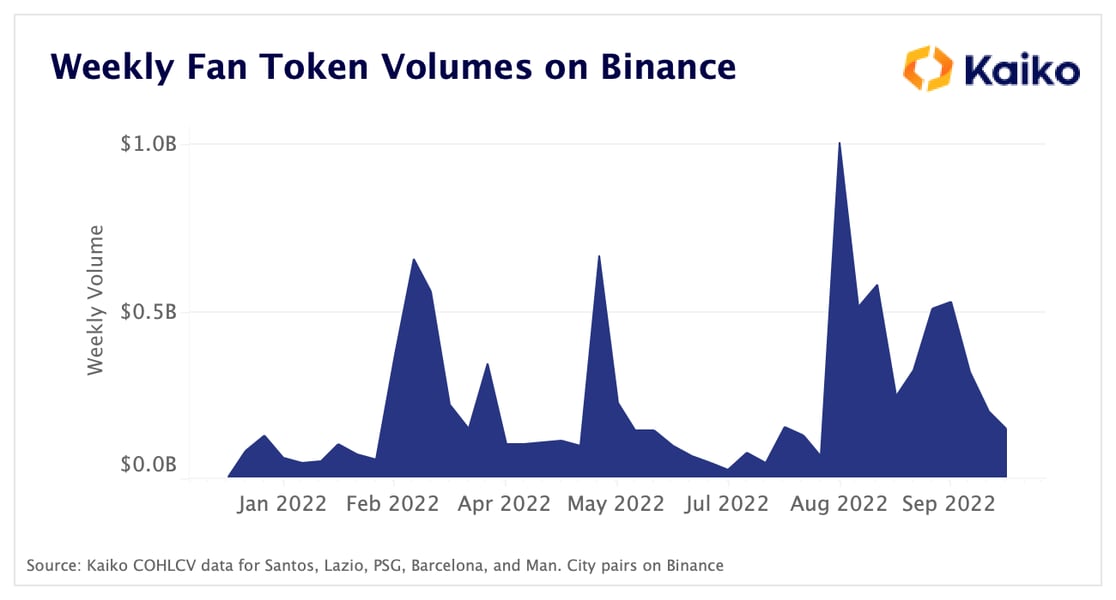

Fan token volumes on Binance spike ahead of World Cup.

Volumes for five of the largest fan tokens by market cap have been significantly higher than summer lows, coinciding with the beginning of the regular season for most of the teams included. Fan tokens are a type of cryptocurrency designed for fandoms, giving holders membership perks such as exclusive content, prizes and votes.

In August, the tokens did over $2bn in volume, decreasing slightly to $1.85bn in September. Volumes have fallen in October along with a wider downturn in crypto markets, with the tokens doing just $700mn. However, the World Cup is fast approaching – scheduled to kick off November 20 – and it is likely that fan tokens will receive renewed interest amidst the world’s most viewed sporting event.

Chicken Bonds, the latest DeFi innovation, causes soaring demand for LUSD.

“Chicken Bonds” are the latest innovation to sweep DeFi markets and they have nothing to do with animals. This new type of “bonding” mechanism was crafted by the Liquity protocol, which issues the decentralized stablecoin LUSD. Holders can “bond” their LUSD in exchange for bLUSD, which accrues yield from LUSD’s Stability Pool and a Yearn Curve vault that deposits into the LUSD-3crv pool, stakes the LP token in Convex, and auto-compounds the rewards into LUSD. Essentially, Chicken Bonds enable higher yield than what one would get by depositing LUSD into Liquity's Stability Pool.

Additionally, bLUSD can be unbonded at any time, giving users the opportunity to "chicken out" by withdrawing their deposits, and users are given a dynamic NFT that indicates the status of their bond. There has been a significant amount of liquidity added to the Curve pool since the beginning of September, with a net gain of over $4mn USD. However, the pool has become more imbalanced, moving from 13% LUSD to just 8% now, which speaks to the high demand for LUSD which has caused the stablecoin’s price to diverge from $1. LUSD’s market cap has grown from $175mn to nearly $190mn since the middle of October.

Derivatives

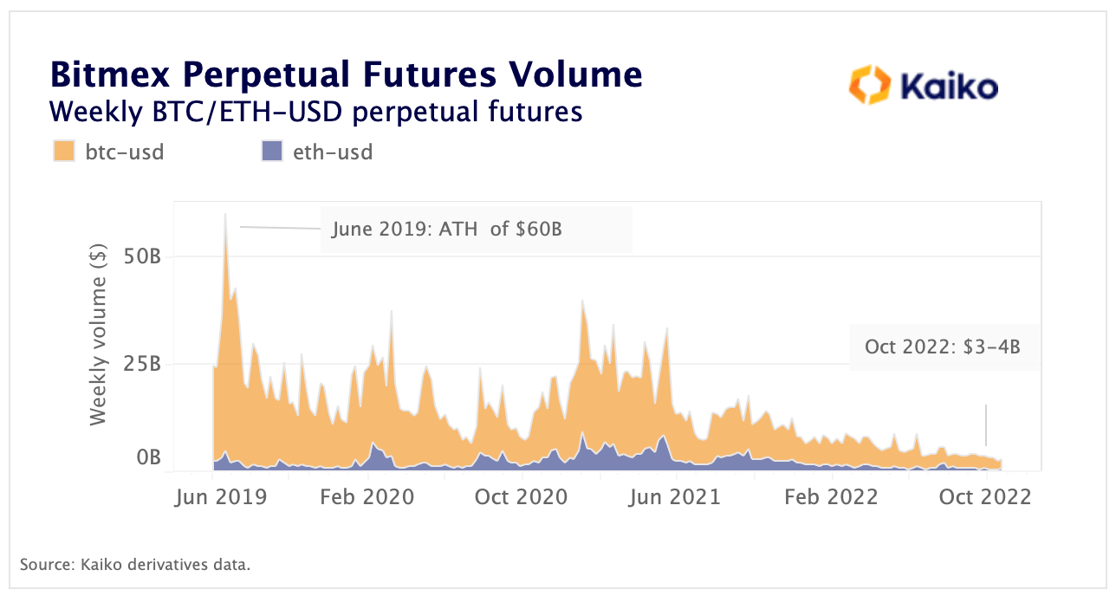

Bitmex derivatives struggle to keep up.

Last week, BitMEX CEO Alexander Hoeptner resigned after less than two years on the job. Bitmex has had a tough few years marked by executive turnover, lagging volumes, and growing competition. The exchange is known for its innovative derivative products and was the first to offer perpetual future contracts back in 2016, benefiting from a first mover advantage. However, as competition intensified - with Binance and FTX entering the markets - BitMEX's trade volumes have decreased significantly. The combined BTC and ETH weekly perpetual futures volumes have declined steadily from an all-time high of $60B in June 2019 to around $3-4B as of October 2022. Today, the exchange's market share for perpetual futures is just 1%.

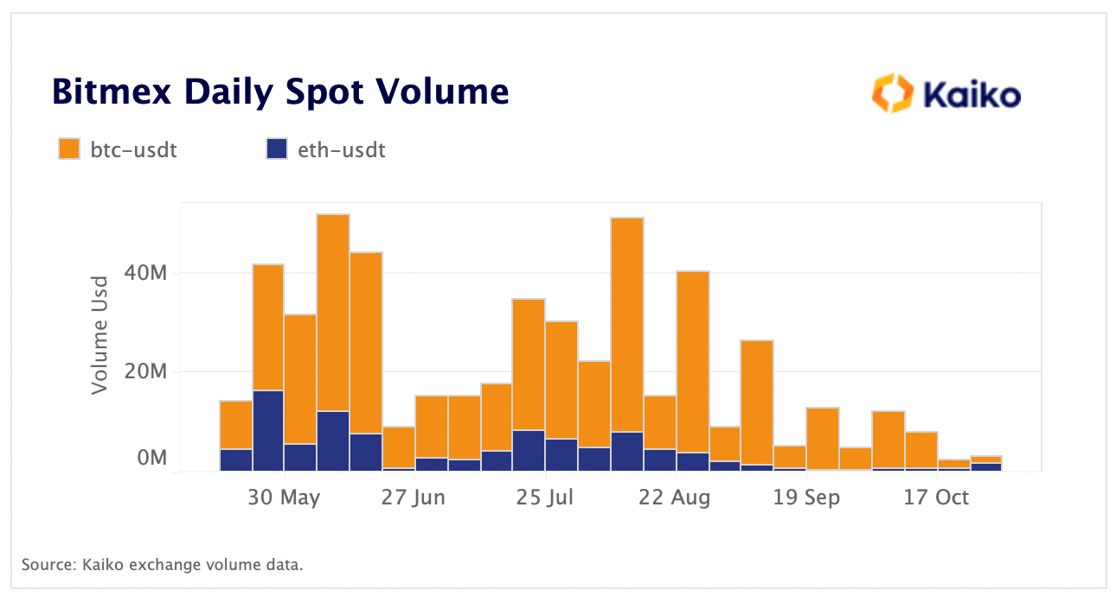

In May 2022, BitMEX launched a spot trading platform in an attempt to expand its product offerings beyond derivatives. However, this effort has struggled to gain traction, with competitors like Binance attracting the majority of market share. The average BTC and ETH weekly spot volumes – which account for around 70% of total spot volumes on the exchange – fell fivefold since June to just $6mn in October.

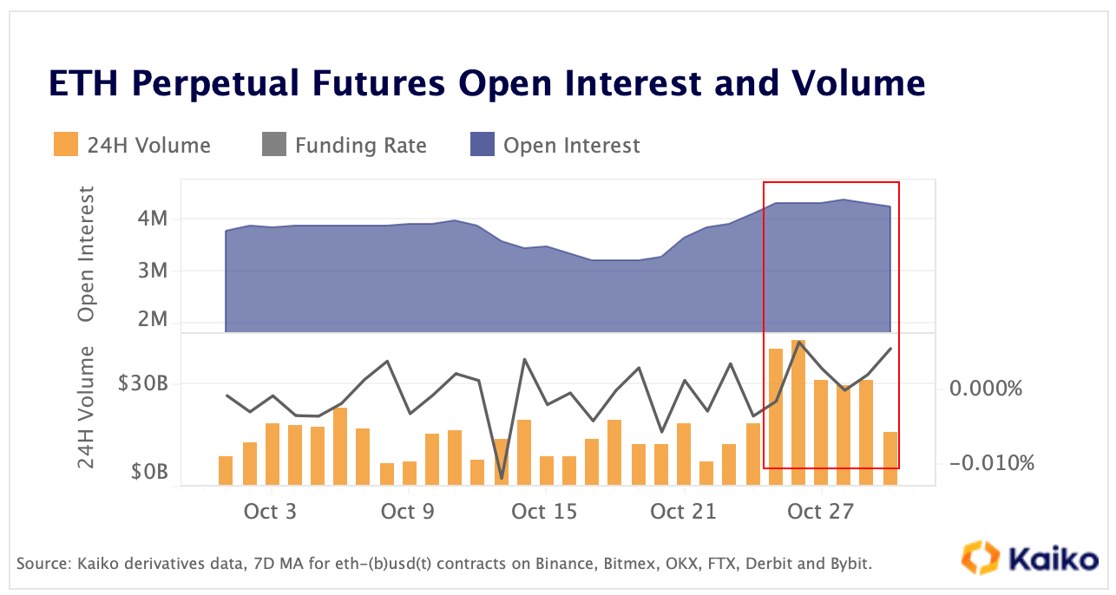

ETH open interest remains stable despite liquidations.

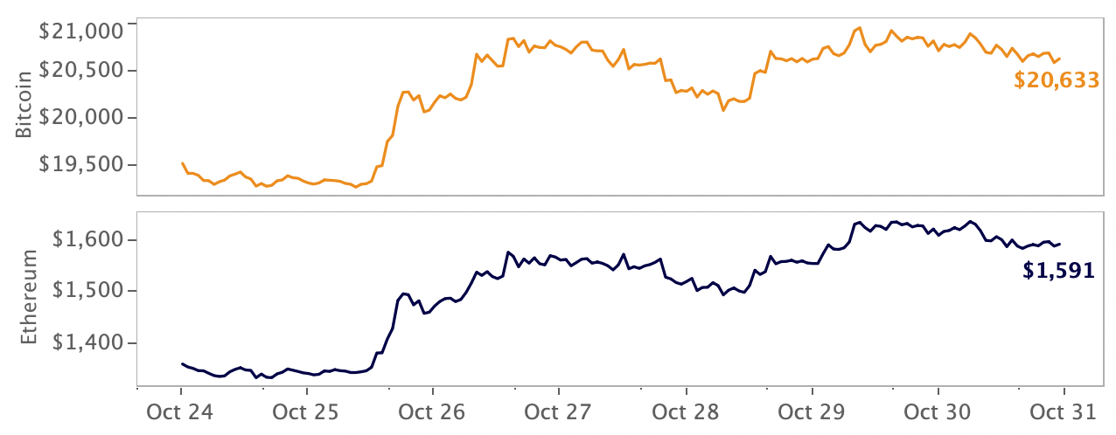

Ether saw a record amount of short liquidations after ETH spot price surged by 17% last week. Perpetual futures trade volumes nearly doubled between Oct 24-26 to around $40B and remained elevated throughout the week. After decreasing by over 16% between Oct 10-20, ETH open interest expressed in native units (removing the price effect) has remained relatively stable throughout the week, hovering above 4mn ETH. Funding rates also turned slightly positive suggesting traders were entering long positions. Bitcoin also gained some ground - ending the week above $20K - which could suggest a broad improvement in risk sentiment.

Macro Trends

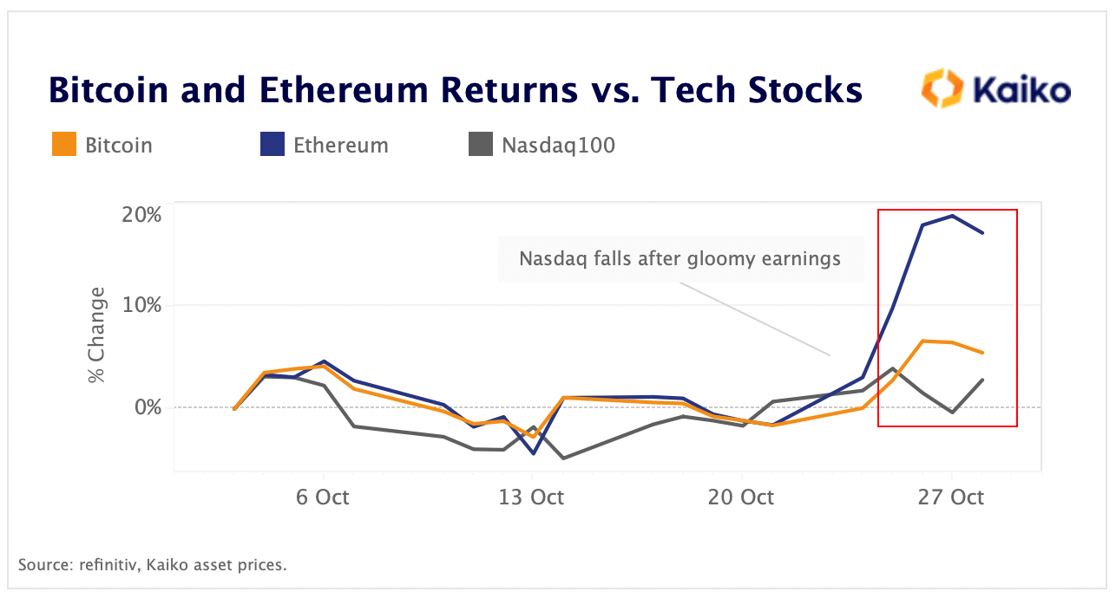

U.S. tech equities underperform crypto as interest rates rise.

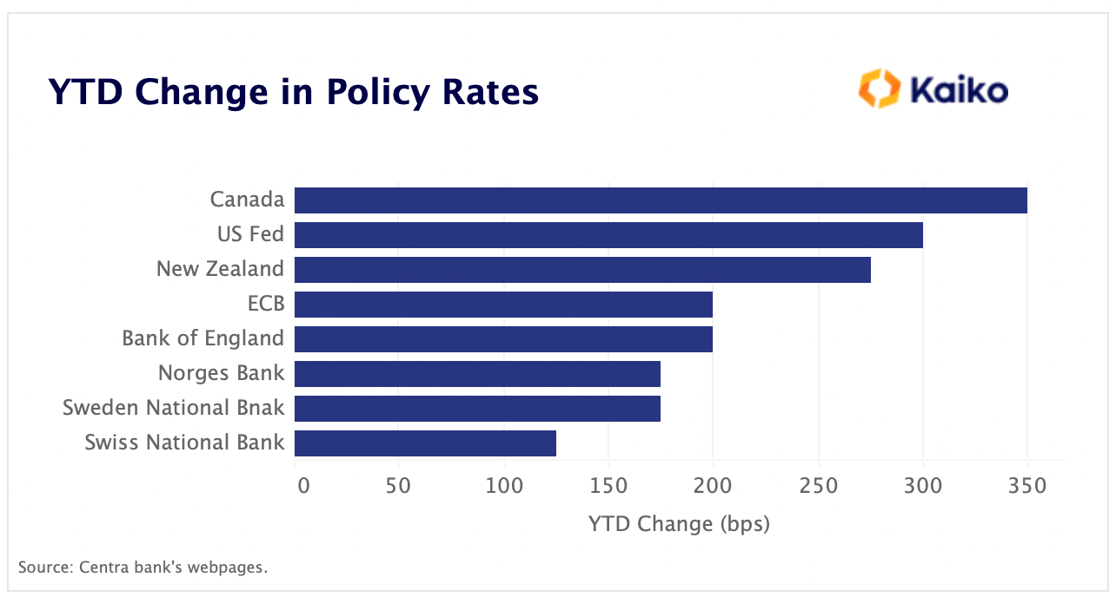

After months of aggressive rate hikes, global central banks are weighing the pros and the cons of additional tightening amid growing recession fears. Last week the ECB joined the central banks of Canada and Australia in hinting that it could slow down the pace of tightening despite German inflation surprising on the upside.

Overall, the U.S. Fed is still widely expected to hike by another 75bps this week, topping the list of most hawkish central banks with a 375bps YTD cumulative increase in rates. However, markets are pricing in a slowdown and a smaller 50bps hike in December.

While ebbing tightening expectations typically benefit risk assets, US equities had a volatile week after a disappointing big tech earnings season. Both BTC and ETH have outperformed the Nasdaq 100 in October, with ETH surging double-digit last week and ending the month up 20%.

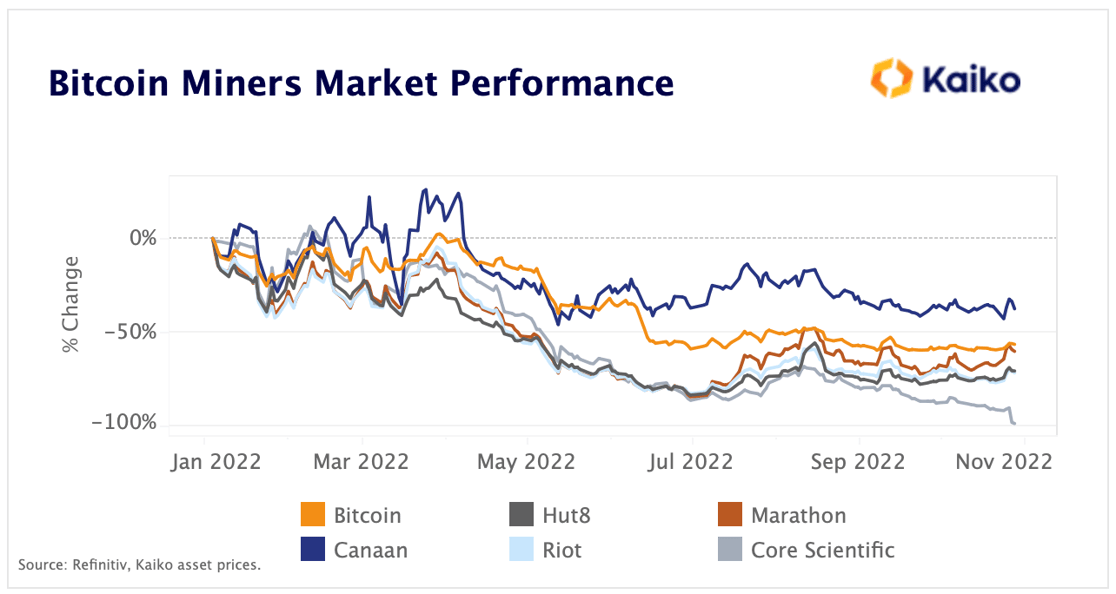

Core Scientific is latest BTC mining company to suffer.

BTC prices are down 70% relative to last year’s all-time high and the network's hash rate has continued rising, putting a strain on miners’ profitability. Most large public BTC mining companies are down double-digits this year, underperforming BTC. Last week, Core Scientific, a public BTC mining company, announced it would halt all payments to service providers, triggering a +70% drop in its share price.

Some smaller companies are facing delisting from the New York Stock Exchange (NYSE) and Nasdaq due to their share prices falling below the $1 threshold. This has created opportunities for crypto-native centralized and decentralized lending platforms. Recently Binance launched a $500mn lending fund for Bitcoin miners while DeFi lender Maple Finance created a $300mn special purpose miner finance pool.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

.png?upscale=true&width=1116&upscale=true&name=image%20(14).png)

-2.png?upscale=true&width=1116&upscale=true&name=image%20(14)-2.png)