Welcome to the Data Debrief! This week, Coinbase announced the launch of their new Layer 2: Base, Jump Crypto recovered 120k ETH stolen during the Wormhole exploit, and the number of daily transactions on Arbitrum surpassed those on Ethereum's mainnet. On the data side, we explore:

The impact of Coinbase's Layer 2 announcement.

BUSD dipping to $0.20 on Binance.

Bitcoin's low correlation with Chinese equities, and more.

Trend of the Week

Optimism's token breaks ATH price and hourly volume following Coinbase announcement.

Following a day of anticipation after a cryptic tweet from Coinbase, the exchange announced that it would be creating an Ethereum Layer 2 network called Base, built on the OP Stack, which is also used by Optimism (token: OP). Coinbase stated its intention to bring users into the Ethereum ecosystem and to provide a percentage of Base’s fees to the Optimism Collective, which governs Optimism.

After the announcement, OP-USD/stable pairs’ hourly volume reached $76mn, the highest hourly volume ever, surpassing the record of $60mn set a couple hours after the token’s launch. On some pairs, including Binance’s OP-BUSD, its price breached ATHs, while Binance’s USDT and Coinbase’s USD pairs did not break their February 3 levels.

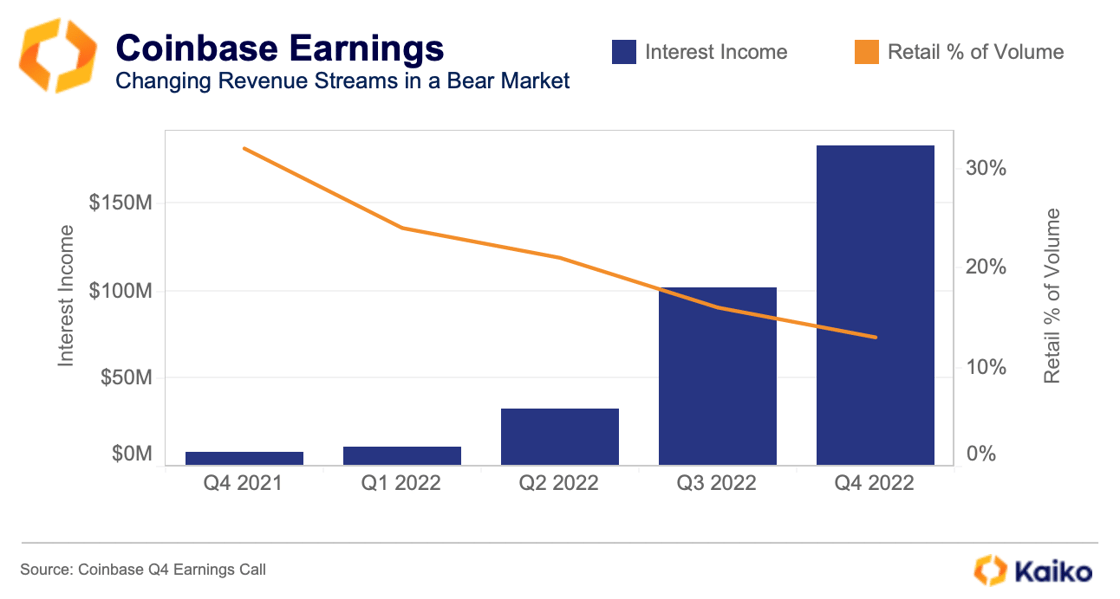

Base could become an important moneymaker for Coinbase, which has been looking to diversify its revenue stream amid falling crypto trading volumes. Coinbase's earnings call last week highlighted its changing revenue stream: this time last year, retail trading made up 32% of Coinbase’s volumes, compared to just 13% now. This is a significant shift in market for Coinbase, particularly as retail trading tends to make the exchange more money than institutional trading.

Coinbase has instead relied more heavily on the interest earned from USDC, rising from $8mn to $182mn year over year. This rise in interest earned has been due to the broad increase in interest rates across the financial system, with Coinbase and Circle now having the ability to generate over 4% interest on collateral backing USDC.

In August 2022, the exchange launched ETH staking services, which boosted its staking income to around 10% of net revenue in Q4. However, concerns around the legality of retail staking in the U.S. have risen after the U.S. SEC targeted Kraken’s crypto staking program in early February.

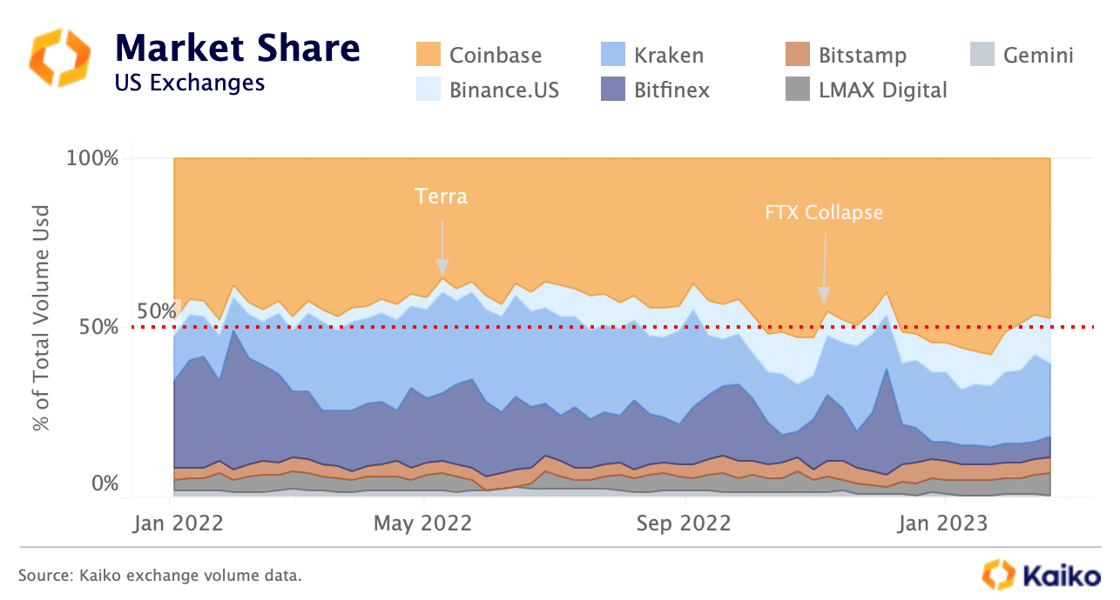

Despite adverse market conditions, Coinbase’s increased its market share from 40% to over 50% last year as it managed to maintain its institutional trading base thanks to lowering market makers fees in September. Binance.US has also exhibited strong growth over the past year despite Binance's global arm facing a confidence crisis and outflows. Its market share has risen from 13% to 23% over the past year.

Price

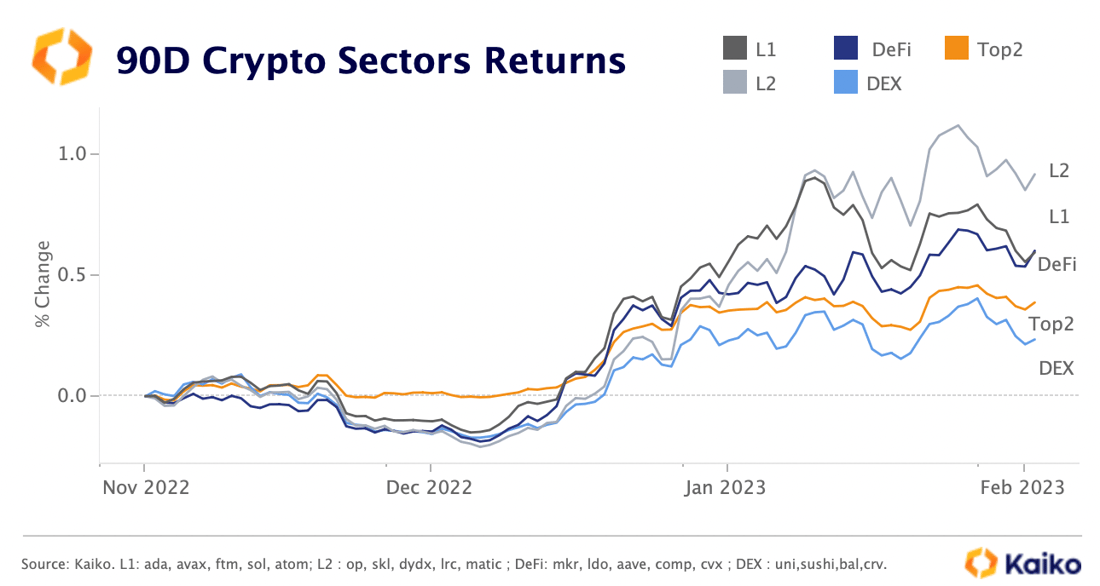

Layer 2s outperform since November.

Enthusiasm around Layer 2 (L2) scaling solutions is on the rise with L2 tokens outperforming the broad market since November. We built five simulated portfolios tracking composite returns of the top five tokens per sector ranked by market cap. The L2 basket is up by over 90% with most tokens rising by over 50% since end-November. Layer 1 and DeFi increased by 60% while the top decentralised exchanges (DEX) tokens are the worst performers. Overall, there have been strong differences in market performance across crypto sectors since the start of 2023, with most altcoins outperforming BTC and ETH. Our equally weighted BTC and ETH portfolio gained 41% and underperformed all sectors except DEXs.

Liquidity

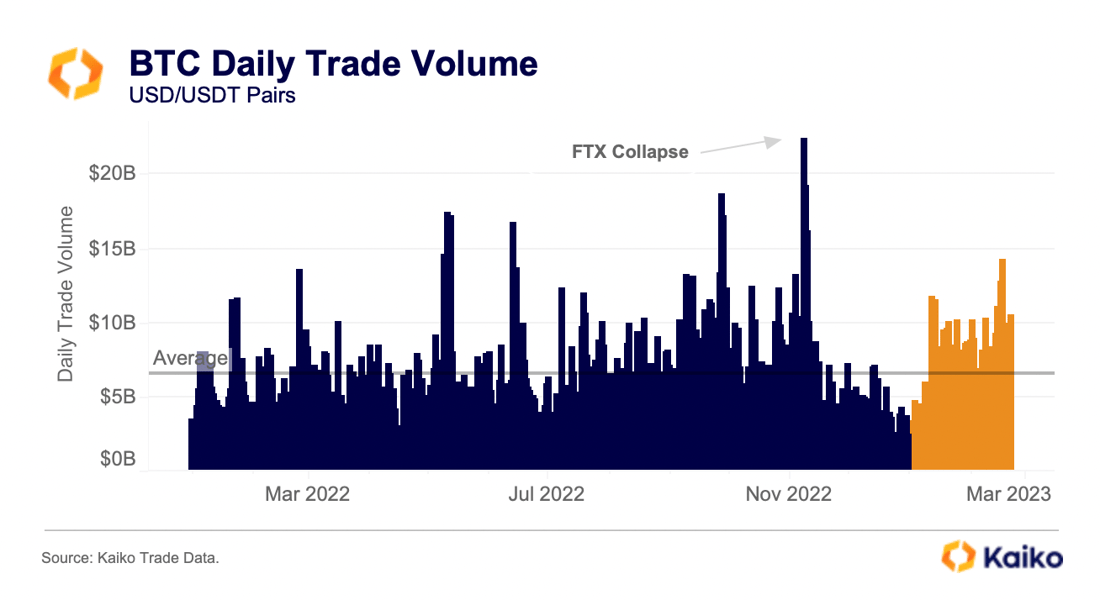

2023 daily volume consistently higher than end of 2022.

Compared with 2022, daily trade volume has been consistently higher in 2023. Daily volume sunk to yearly lows at the end of 2022 in part due to poor sentiment among retail after FTX's collapse. Encouragingly, that sentiment appears to have picked up significantly to start 2023, with daily BTC volume crossing $14bn at times during February.

The overall level of volumes is also higher than the end of 2022, seemingly anchored to the $10bn daily volume number, as opposed to about half that to close last year.

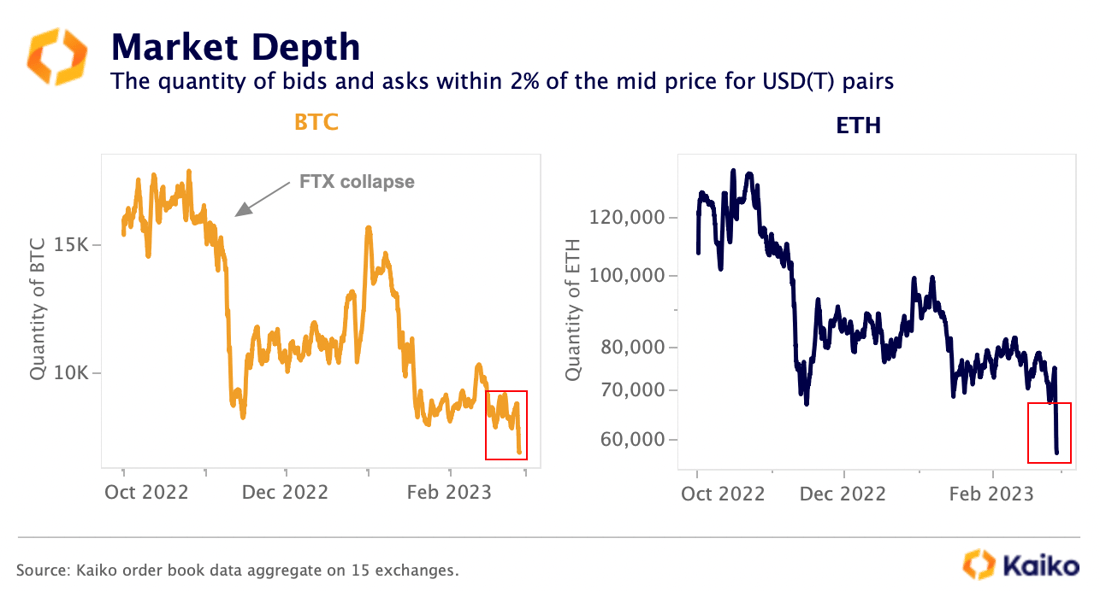

BTC and ETH market depth hits lowest level since May 2022.

BTC and ETH liquidity in native units continued falling last week, hitting its lowest level since the Terra collapse. BTC 2% market depth aggregated on 15 centralized exchages fell to 6.8k BTC, down almost three-fold since October’s highs. Liquidity plummeted by 43% on Binance and Coinbase and by over 60% on Gemini and Kraken.

ETH market depth also dropped to around 57k ETH down from 139k ETH in October. The decrease was mainly driven by Binance where ETH market depth fell by 63%, compared to a 38% drop on Coinbase. Overall, market makers remain risk averse amid darkening macro outlook and regulatory uncertainty in the U.S.

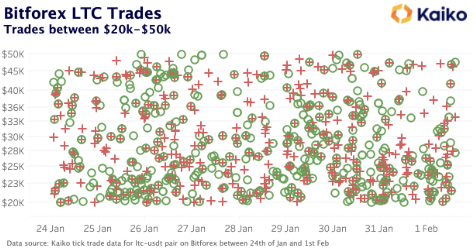

BUSD briefly dips to $0.2 on Binance.

There was a brief moment of panic on February 22 as Twitter accounts that alert to quick price movements sounded the alarm that BUSD had traded at $0.20 on its BUSD-DAI pair on Binance. While some speculated that this was a visual error, we found that the price had in fact decreased rapidly, and some traders were able to purchase thousands of BUSD at an 80% discount. However, the cause remains somewhat of a mystery, as there was no large sale of BUSD that caused the dip.

In fact, in the minutes before the flash crash, traders were actually buying large amounts of BUSD, represented by the large green circles. At 11:16am UTC there was $400k worth of bids; just a minute later this had decreased to less than $30k before improving again. Thus this crash appears to have been liquidity driven, perhaps with a market maker or large trader pulling bids as volume spiked.

Curve pool shifts as Curve releases Euro Coin.

Coinbase last week listed Euro Coin (EUROC), a stablecoin pegged to the Euro and issued by Circle. While Uniswap V3 facilitates most of the volume for EUROC, Curve holds its largest liquidity pool. This pool holds EUROC and agEUR, a decentralized stablecoin issued by Angle. The pool has been relatively static since its inception, with €9mn locked. However, since the beginning of the year, the pool has grown to over €10mn while the balance has shifted, with €7.4mn agEUR and €2.8mn EUROC.

As discussed in a previous Deep Dive, this shift in balance suggests that there is increased demand for EUROC. The growth of non-USD stablecoins will be something to watch as there are signs that Binance may opt to replace BUSD with an alternative stablecoin.

Derivatives

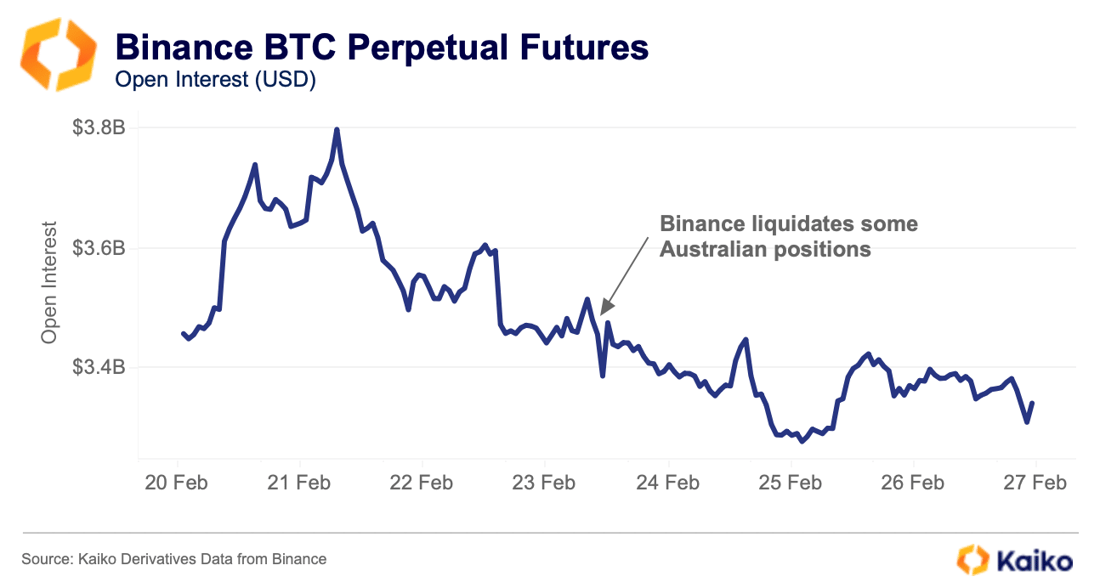

Binance liquidates incorrectly tagged Australian users.

On Thursday, Binance announced it had incorrectly tagged 500 Australian users as wholesale investors, resulting in a complete liquidation of their positions. Binance Australia does not allow retail users to trade derivatives products on the exchange; only wholesale traders are allowed to trade these products. Open interest for BTC contracts Binance did drop by nearly $100mn, though this coincided with a significant price drop for BTC and can thus be classified as price-driven. It seems the 500 traders were not large enough to materially impact BTC’s open interest figure in global derivative markets.

Macro

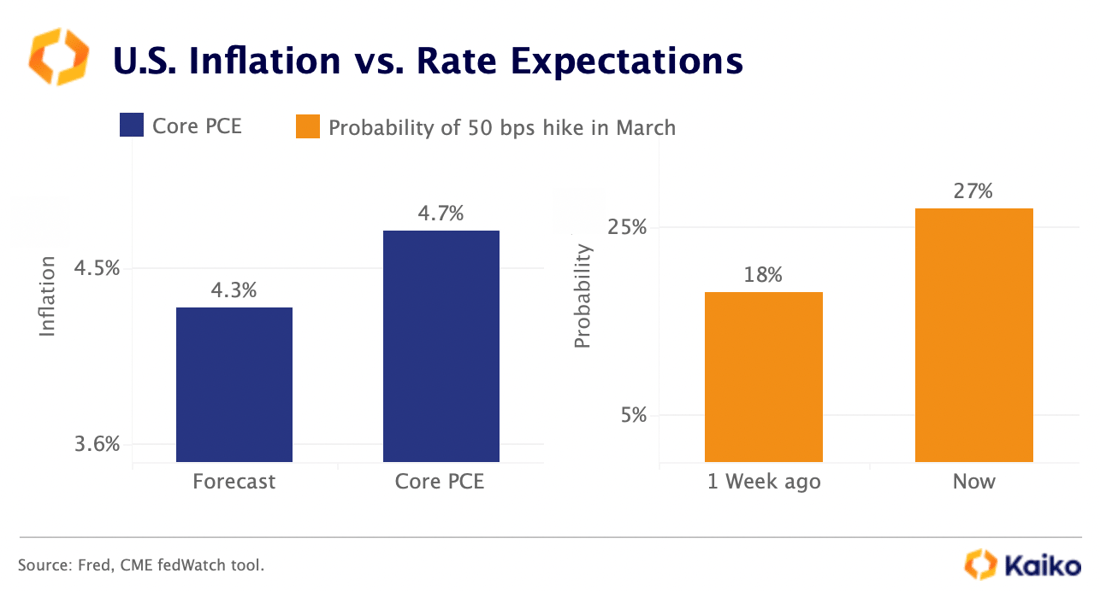

More cracks in the disinflation narrative.

The disinflation narrative that boosted risk assets over the past weeks is increasingly under scrutiny as the U.S. Fed’s preferred gauge of inflation – the personal consumption expenditure (PCE) – beat expectations last week. The core PCE accelerated to 4.7% year -over-year, rising at the fastest pace since July.

The hot inflation data joins a robust jobs report in January and the lowest unemployment rate in half a century. BTC fell 2.6% on Friday following the release, underperforming the Nasdaq 100 which declined 1.7%. Overall, risk sentiment weakened in February as investors sharply repriced their monetary tightening expectations. Probabilities of a 50 bps rate hike in March rose to 27% from 0% a month ago according to the CME FedWatch tool.

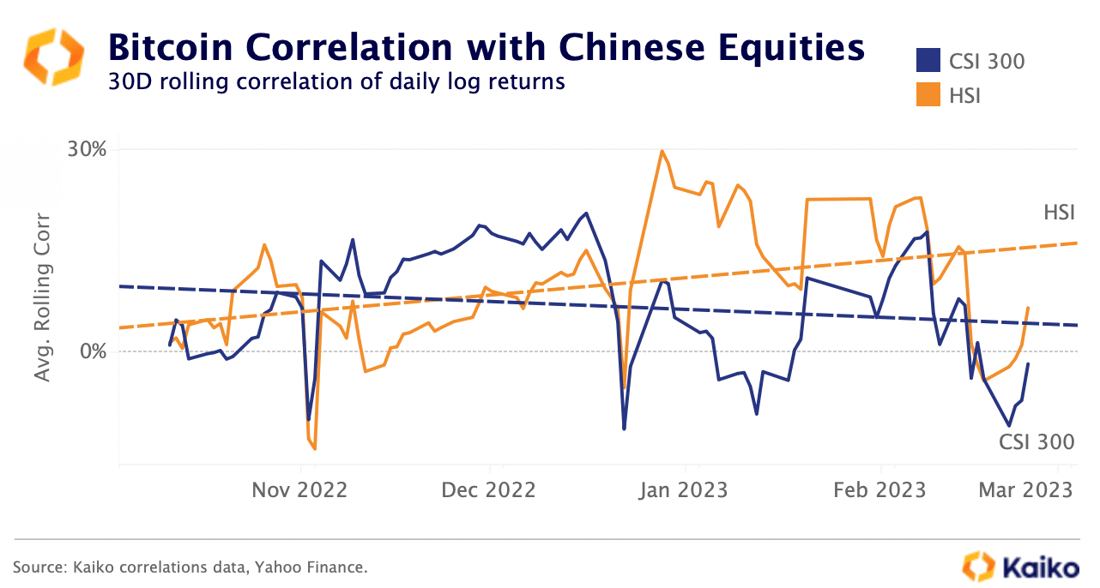

Bitcoin remains uncorrelated with Chinese equities.

Crypto markets remain mostly uncorrelated with Chinese equities. BTC's correlation with the blue-chip CSI 300 index and Hong-Kong listed Heng Seng China Enterprise Index (HSCE) hovered between -0.2 and 0.2 over the past months.

Interestingly, since the start of the year, BTC is slightly more correlated with the HSCE than the CSI, perhaps due to the greater global investment in the HSCE.

The influence of China on crypto asset prices has been limited after a wave of regulatory crackdowns on crypto beginning in 2017. However, this may change in the coming months if some of the pent-up Chinese demand finds its way into crypto via Hong Kong (for more on the impact of improving regulatory clarity on Asian markets check out last week's Deep Dive).

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-Feb-27-2023-01-18-07-2524-PM.png?upscale=true&width=1120&upscale=true&name=image%20(5)-Feb-27-2023-01-18-07-2524-PM.png)

-Feb-27-2023-01-17-30-7969-PM.png?upscale=true&width=1100&upscale=true&name=image%20(3)-Feb-27-2023-01-17-30-7969-PM.png)

-Feb-27-2023-01-17-43-9854-PM.png?upscale=true&width=1100&upscale=true&name=image%20(4)-Feb-27-2023-01-17-43-9854-PM.png)