Welcome to Deep Dive, Kaiko Research's brand new newsletter! Kaiko takes its name from the research vessel that successfully explored the deepest known point on the Earth's seabed inside the Mariana Trench, bringing incredibly valuable data to scientists around the world. In that spirit, Deep Dive will leverage Kaiko's unique cryptocurrency market data, providing in-depth and original insights to make sense of the complexities of cryptocurrency market structure today.

Our first issue explores the state of stablecoins in the aftermath of TerraUSD's collapse, diving deep into the variety of stabilization mechanisms that exist, and various market trends. Let us know if you have any feedback, and enjoy!

The Stablecoin Trilemma

June 2, 2021

By Conor Ryder, CFA

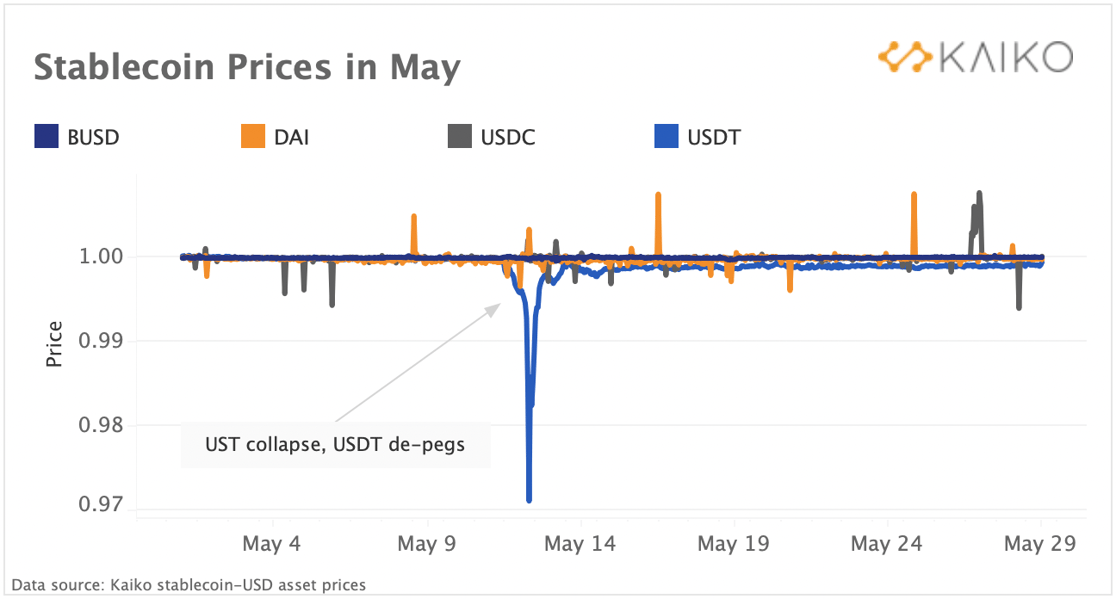

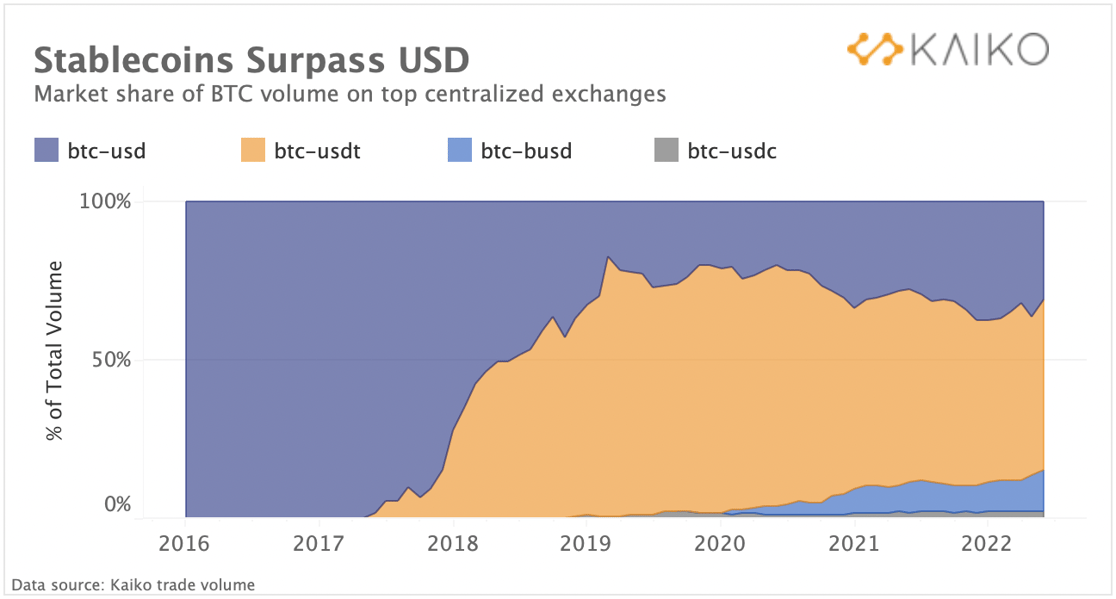

After a historic month of volatility, stablecoins have found themselves in the hot seat of the crypto universe. The dramatic collapse of Terra/Luna, the depegging of USDT and ongoing concerns around the reliability of stabilization mechanisms has generated unprecedented investor and regulatory scrutiny for a systemically important sector of the crypto economy. Just looking at the market share of stablecoin vs. USD volume over the years, we can observe how they have come to account for the majority of trading activity, far surpassing fiat currencies.

Yet, the backbone of cryptocurrency markets has arguably never been more, well, unstable. However, not all stablecoins are the same and in this article I’ll focus on the various nuances of each stabilization mechanism, using data to examine the current state of market structure.

Why Are Stablecoins Important?

In its purest form, a stablecoin is a digital asset on the blockchain whose value is tied to another stable asset, usually the US Dollar. The ability to remove volatility from the equation means that stablecoins become appealing not only as a store of value, but also as a medium of exchange. The result is what should be a superior form of fiat currency to which we’re accustomed. An economy run on decentralized currencies would be permissionless, programmable, borderless, trustless and highly liquid. The benefits are clear, but remain nearly utopian at this moment in time. We’ve seen large scale adoption of stablecoins, but each stablecoin has had to make trade offs in order to become a more viable option for investors, most evident in the collateral set-up.

There are generally three types of approaches that stablecoins take with regards to the collateral they keep in reserve:

1:1 Collateral (USDC, USDT, BUSD)

Over-collateralized or crypto-collateralized (DAI)

Under-collateralized/algorithmic (MIM, FRAX, and formerly UST)

1:1 Collateral

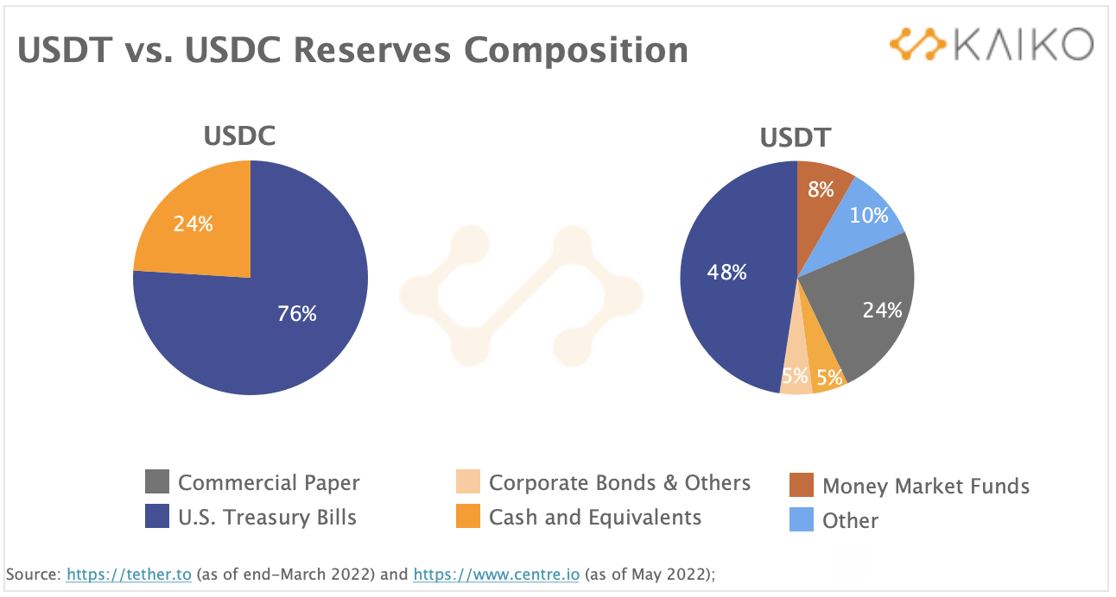

The collateral approach with the most adoption has been to keep the equivalent of 1:1 reserves with the US Dollar in order to maintain a 1:1 peg. For example, Circle’s stablecoin USDC currently has 53 billion tokens in circulation, matched by the equivalent of $53 billion in reserves. This approach offers good security in its 1:1 peg with the US Dollar and is somewhat capital efficient as $1 is needed to create $1 worth of stablecoins. Tether (USDT), however, provides little reassurance with regards to their reserves; they collateralize 1:1 but as we’ve charted below about 10% of their reserves come in the form of “Other” assets which Tether offer little to no clarity on, as well as providing little clarity on the location or nature of their holdings - leaving their 1:1 ratio ripe with ambiguity.

Tether and Circle reserve breakdowns showcase the big problem with centralized stablecoins, in that they require investors to trust centralized entities, something which ideally goes against the ambitions of both stablecoins and crypto. Generally, we think of the tradeoffs for stablecoins as a trilemma between:

1. Peg security

2. Capital efficiency (how much capital is required to make $1 of a token)

3. Decentralization

I’d suggest including a fourth option here for centralized stablecoins which would be:

4. Corporate profits

From a business model point of view, corporate profits are a big factor in the setup of centralized stablecoins as companies like Circle and Tether look to utilize the cash they have on hand to earn profits. Market makers, investors and crypto businesses offer Circle or Tether cash in exchange for stablecoin issuance, which means technically both issuers could collateralize at a 1:1 ratio in all cash. Why don’t they do this? Corporate profits. Leaving billions of dollars in cash on hand limits their interest-earning capabilities and their bottom line.

It’s a big reason why virtually no stablecoins are denominated in Euro: the ECB has been running negative interest rates on cash deposits for over a decade now and any corporation that is holding a chunk of cash in reserve is guaranteed to be losing money on those reserves. Interest rates in the US, on the other hand, have been positive, giving stablecoin issuers holding US Dollars a bit more flexibility in their management of reserves. As we can see in the chart above, Circle and Tether have taken very different approaches to managing their reserves, with Tether clearly taking on riskier investments in the pursuit of more profits.

USDC and USDT have prioritized corporate profits and maintaining the security of their 1:1 peg over decentralization. Their capital efficiency is good but not as good as an algorithmic stablecoin.

Overcollateralized

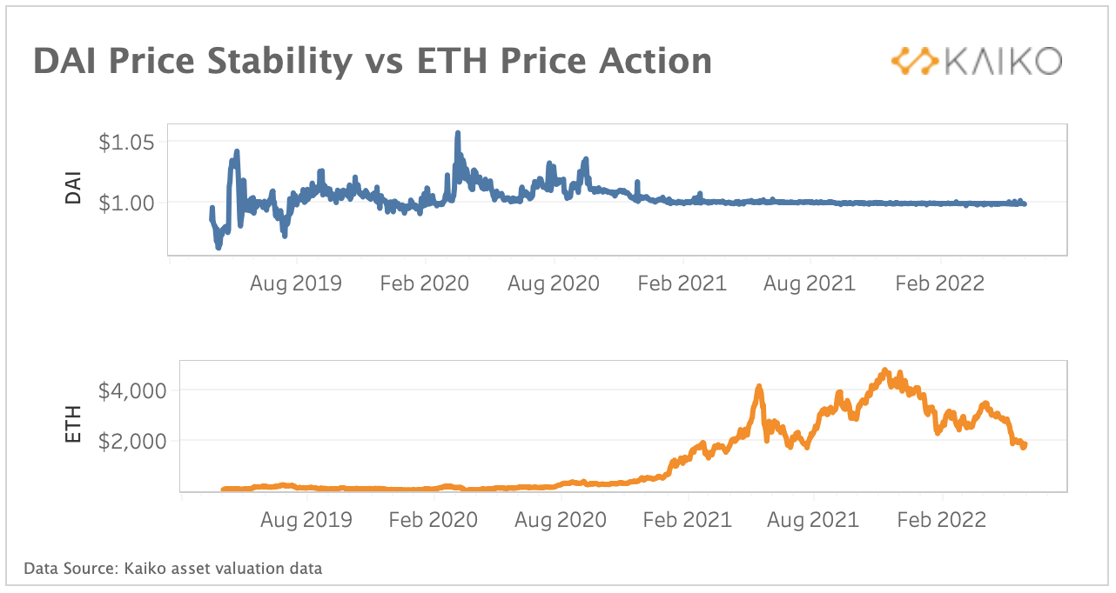

The second type of stablecoin collateral mechanism involves the use of a surplus of reserves to maintain a 1:1 peg. DAI is the most popular stablecoin using this model, and has overcollateralized reserves containing ETH, USDC, WBTC, and more. This surplus of assets should theoretically allow DAI to maintain its peg of 1:1 to the US Dollar, even though assets such as ETH are more volatile than usual forms of collateral. The overcollateralization and diversity of reserves is designed to meet an increase in redemption demand in the case of volatility for one or more assets held. As we’ve charted below, the DAI peg has so far held up relatively well despite large swings in ETH’s price, indicating that the reserve mechanisms are doing their job.

The main benefit of DAI is that it is decentralized; unlike USDT and USDC, DAI is run by a DAO (Decentralized Autonomous Organization) which allows community votes on proposals such as collateral makeup. The main risk to DAI would be if a black swan type event were to happen to ETH or other collateral assets, in which case DAI’s reserves might not meet redemption demands.

DAI has also had its decentralization called into question due to the make up of its collateral, particularly the prominence of USDC in their collateral breakdown. This presents a good deal of systemic risk to the DAI ecosystem and a good argument can be made as to how decentralized the project is as a result.

Reverting to the aforementioned stablecoin trilemma, DAI has attempted to prioritize decentralization and to a lesser extent security of its peg, over capital efficiency. The capital efficiency of the overcollateralized model is the biggest drawback as it takes more than $1 of capital to create $1 worth of tokens. That being said, investors seem happy with DAI’s model as DAI is by far and away the leading decentralized stablecoin after UST’s collapse, with on average $500m traded every day on DEXs, and $200m a day on CEXs.

Algorithmic

Algorithmic stablecoins were the focal point of this past market crash, with UST/Luna taking center stage. Algorithmic stabilization mechanisms typically involve the use of another token that expands and contracts in supply as the stablecoin is created or burned. It is now proven that this mechanism is not viable, and can result in devastating death spirals. For a deep dive on UST’s collapse and the stablecoin’s flawed stabilization mechanism, my colleague Riyad wrote a great article on the topic you can read here.

Algorithmic or under-collateralized stablecoins prioritize capital efficiency above all else and are usually somewhat decentralized, both at the expense of the safety of their pegs. Following UST’s collapse, the future of algorithmic/under-collateralized stablecoins remains up in the air, with no yet proven model for avoiding a death spiral.

Stablecoin Market Structure

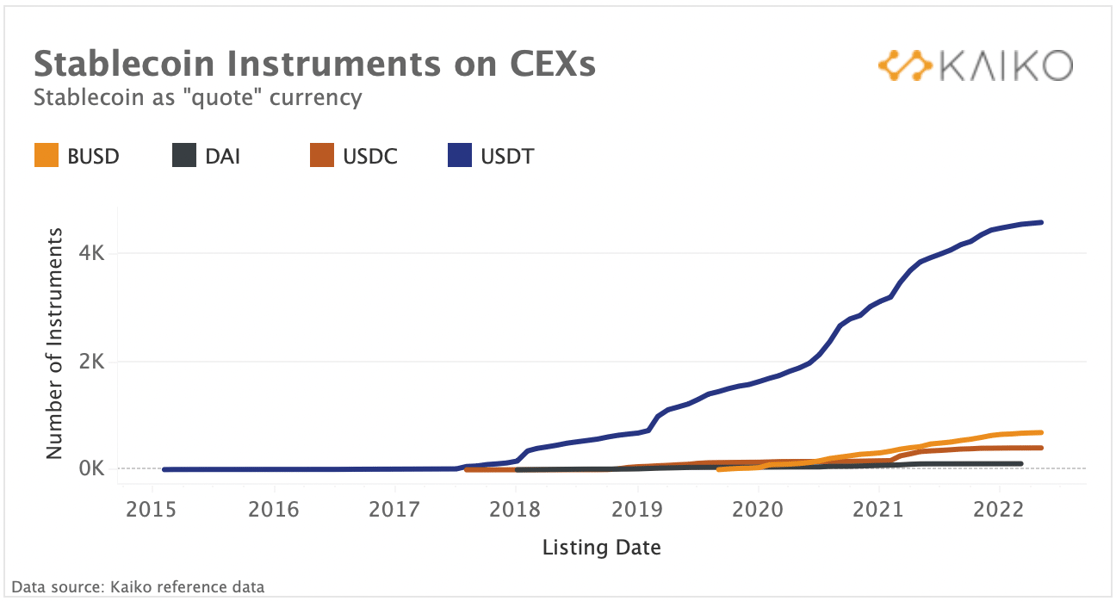

Today, stablecoins have surpassed both fiat currencies and Bitcoin as the leading denominating asset on centralized exchanges, which still account for the vast majority of crypto market activity. Since 2017, the number of new BTC-denominated spot instruments has dropped precipitously, while stablecoin-denominated listings have soared. Fiat listings have experienced steady growth, in large part due to increasing efforts by exchanges to be regulatory compliant within countries.

USDT is by far the dominant stablecoin, accounting for the vast majority of new listings on centralized exchanges. Binance’s BUSD ranks second, in large part due to the amount of BUSD-denominated pairs the exchange offers.

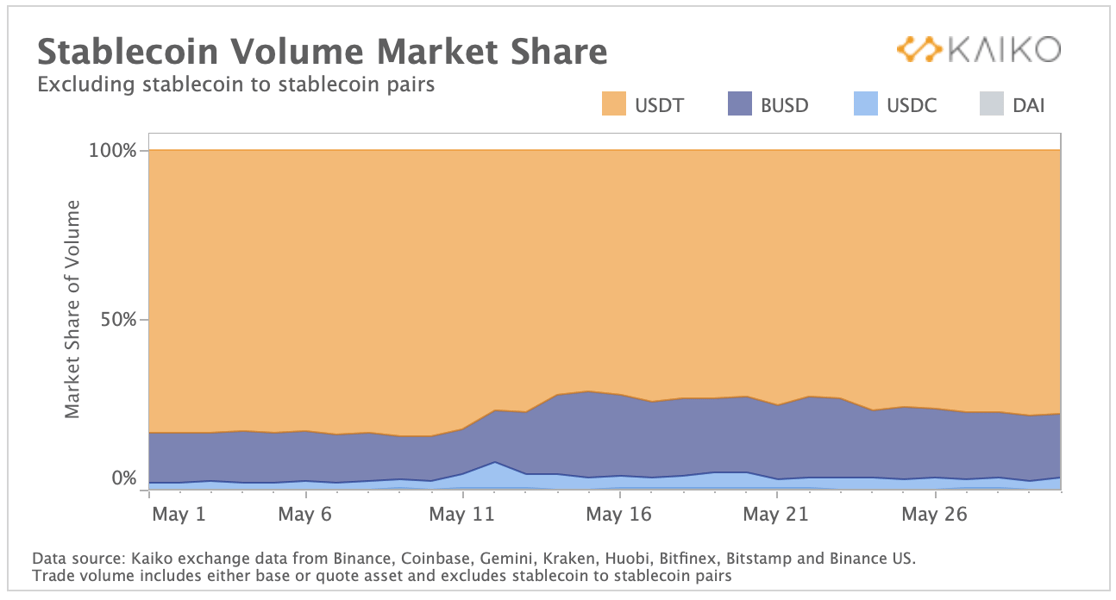

When looking at trade volume, we can see that USDT possesses around 80% market share on centralized exchanges.

Interestingly, BUSD took a large share of volume, gaining about 12% after the Tether depeg on May 12th as investors prioritized stability in the stablecoin market. Prior to its depeg Tether had an 84% volume share and as of the end of May that share has been reduced to 77%.

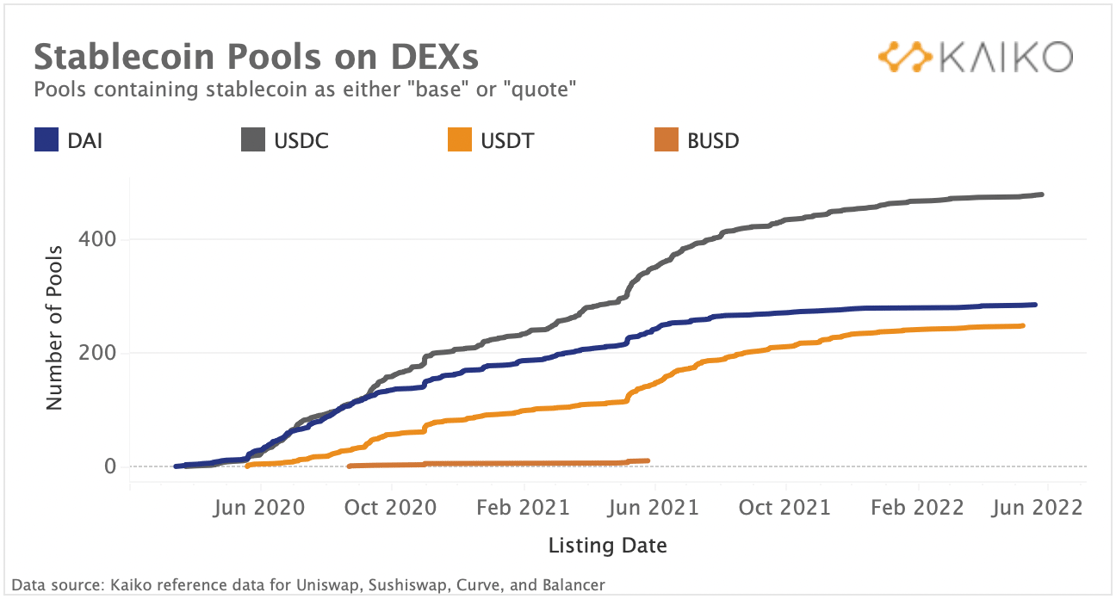

On DEXs, stablecoin market structure is very different, with USDC and DAI being the most popular stablecoins used in pools, with USDT in third and BUSD a distant fourth.

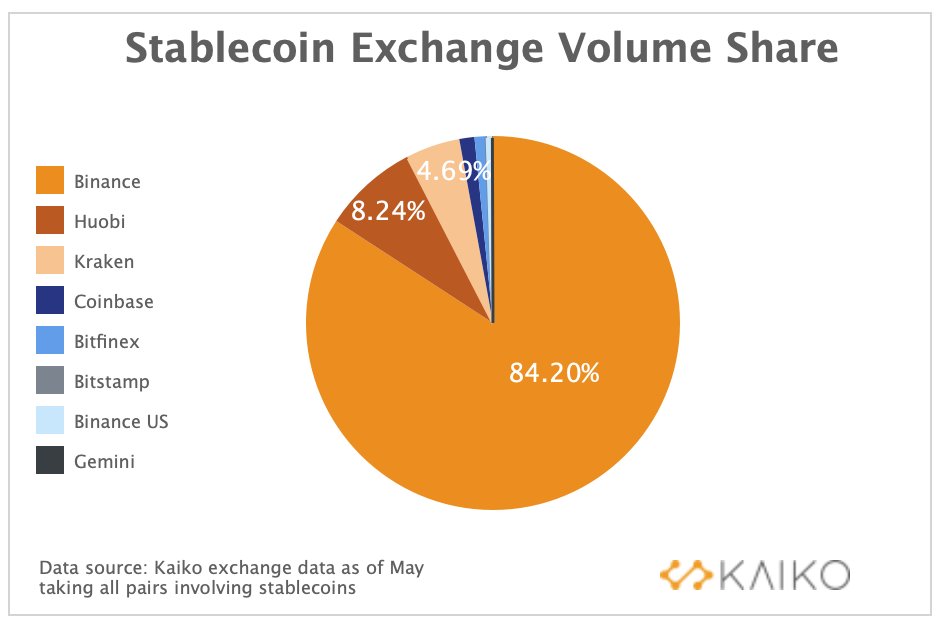

Exchange volume share paints a similarly dominant picture for stablecoin volume with Binance owning roughly 70% of all volume for the exchanges chosen. Kraken’s share of stablecoin volume went from 12% on May 12th back down to 8% by the end of the month, while Coinbase volume share closely tracked roughly 10% for most of the month, bar a spike to 17% on May 20th.

The main insights to be gained when looking at stablecoin market structure are that Tether is dominant on centralized exchanges, with the majority of activity concentrated on Binance. On DEXs, stablecoins are widely traded, albeit with a lot lower volumes and USDC and DAI taking the lead.

Conclusion

The most pressing issues with centralized stablecoins is two-fold in my eyes:

Transparency

Easily regulated

As is the case with Tether and Circle, corporate profits have been given preference over transparent collateralization as both entities have failed to provide much clarity as to the nature of their reserves. Not only that but another downside to this model is it’s well inside the scope of regulators who can place limits on the capabilities of centralized entities. The mass adoption of these centralized stablecoins so far indicate that these are risks investors are willing to take in the hope of safer stablecoins.

No doubt centralization is a safer model, which is perhaps what is needed in the short term to restore faith in crypto markets, but longer term a decentralized solution fits the ethos of a trustless crypto far better. This solution could look like what RAI is doing currently, holding only ETH and therefore fully decentralized collateral, while not relying on an internal token like Terra did to stabilize the peg in the event of a market crash.

If I had to guess, I would say that the decentralized solution to stablecoins hasn’t been found yet, but it’s of utmost importance if we are to build a trustless economy. I also believe that an economy running on decentralized currencies is how crypto breaks away from its high correlation to equities, not affected by Jerome Powell’s every word at a press conference. That however is a topic for another day, and likely another article. Either way, it’s safe to say that the month of May has regulators and investors watching the stablecoin space with a very keen eye.

Thanks and see you next week!

Kaiko Market Reports

Data-driven commentary on April's most significant market events

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.