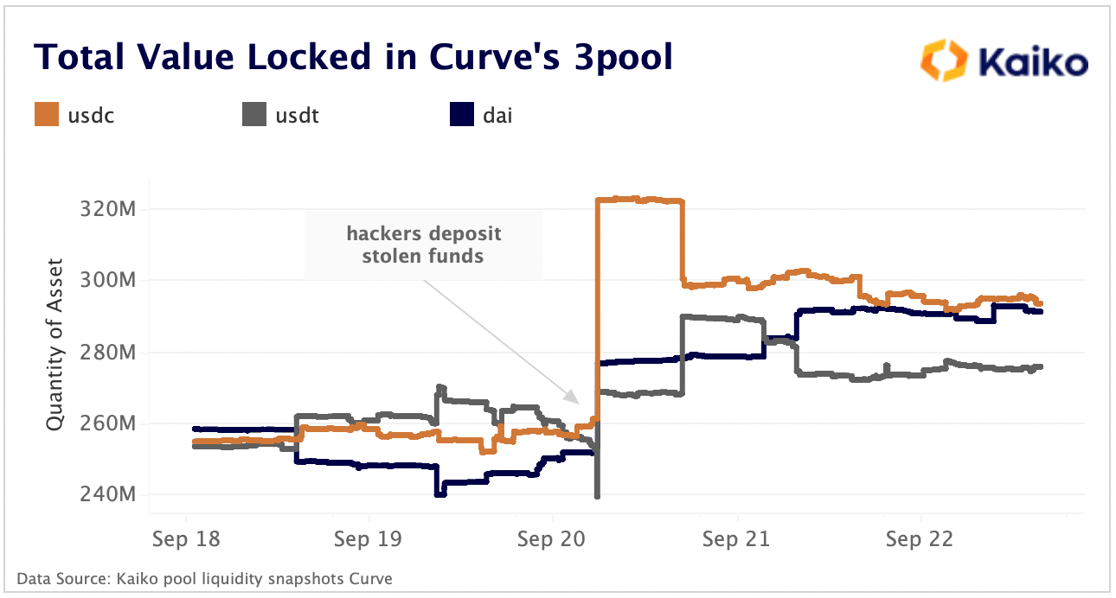

Another week, another massive crypto hack. Last week, Wintermute, one of the largest cryptocurrency market makers, was exploited for $160mn likely due to a bug associated with its wallet address. According to the CEO, only the firm’s DeFi unit was impacted while CeFi and OTC operations remain unaffected. A series of transactions quickly followed the hack which saw 112 million tokens transferred to Curve’s 3pool. The 3pool is one of the largest liquidity pools in DeFi, enabling swaps between the stablecoins USDC, USDT and DAI. Using Kaiko’s liquidity pool data, we can observe the exact moment the hackers deposited stolen funds in the 3pool, which caused the pool to become temporarily imbalanced with a surplus of USDC.

The hackers likely deposited funds in the 3pool as a way to avoid getting blacklisted by the issuers of USDC and USDT. Tether and Circle would only be able to freeze the stolen tokens by blacklisting the entire 3pool. This is far from the first time DEXs have been used to move stolen funds, although it is certainly one of the most visible hacks of the year.

Wintermute trades billions of dollars a day across various centralized and decentralized cryptocurrency platforms, providing essential liquidity services to the industry. The firm’s CEO asserts that the company remains solvent following the hack, and there was no observable drop-off in liquidity on centralized or decentralized exchanges.

Price Movements

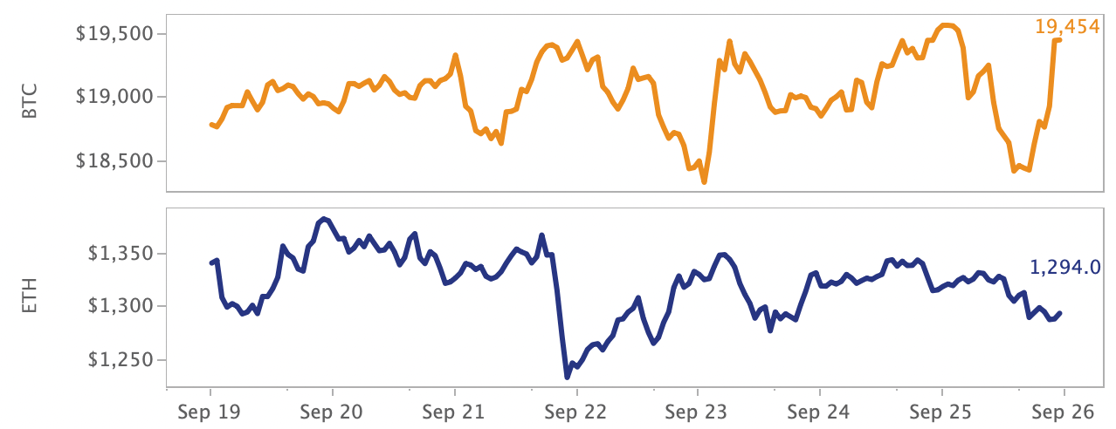

Crypto markets stabilize as macro volatility surges.

Global markets are spinning amid one of the most volatile macro environments in decades. Last week, the Fed raised interest rates another 75 bps and although the move was largely expected, traditional risk assets experienced a sharp sell-off with the S&P 500 barreling towards yearly lows. The U.S. Dollar’s surge to multi-decade highs has compounded global equity volatility, hitting EU and UK markets particularly hard. As of Monday morning, BTC and ETH actually recovered some of their losses following the dramatic post-Merge sell-off, although a strong dollar historically bodes poorly for crypto.

There were some major updates this week on the crypto regulatory front: U.S. legislators proposed a two-year ban on algorithmic stablecoins, the EU finalized the text of its landmark crypto regulatory framework, and a judge ordered Tether to produce records showing USDT’s backing. In wider industry news, Nasdaq announced a crypto custody service, OpenSea expanded to the layer 2 Arbitrum, and Binance and FTX entered a bidding war for distressed lender Voyager Digital.

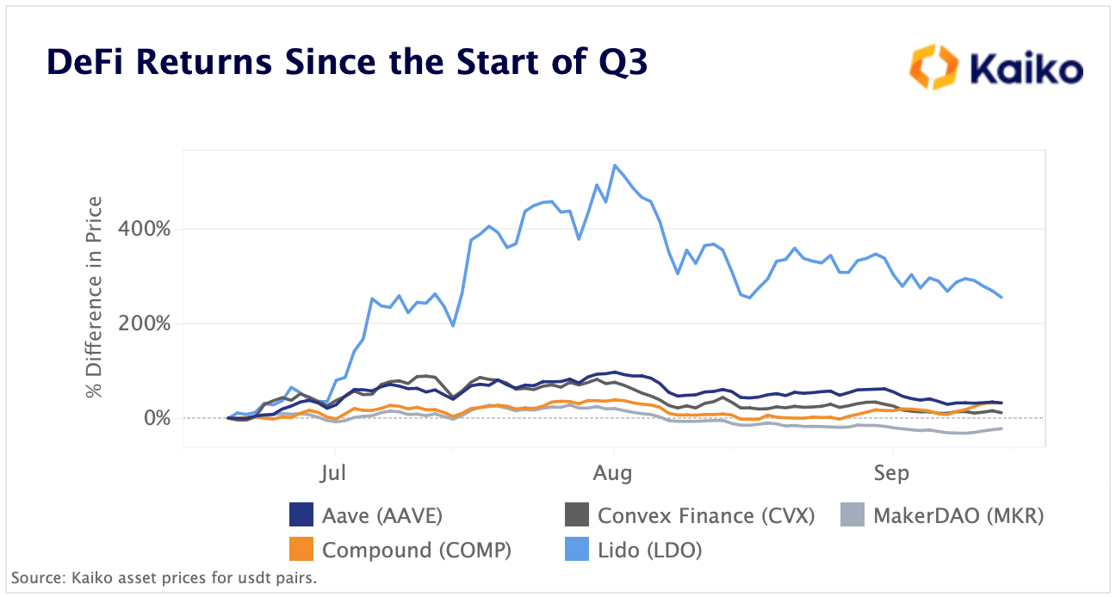

Lido’s LDO outperforms in Q3.

Liquid staking protocol Lido’s native token LDO has outperformed in the third quarter of the year. Lido offers staking services for five blockchain networks, with Ethereum accounting for the vast majority of total value locked. Despite the market downturn in September, LDO is still up by a staggering 255%. The protocol’s total value locked also increased but at a much slower pace (30%) and remains well below its levels from earlier this year, although this is largely due to the collapse of the Terra network, for which Lido offered staking services. While the success of the Merge could provide a boost to Ethereum’s liquid staking market, Lido faces rising competition from centralized exchanges.

Overall, DeFi protocols have shown resilience despite the risk-off mood and recent hacks. Lending and borrowing protocol Compound, which recently launched a new feature allowing institutions to borrow against digital assets, has rallied in September and is up over 32% in Q3. MakerDAO’s token MKR was the worst performer of the lot with both its price and total value locked declining in Q3.

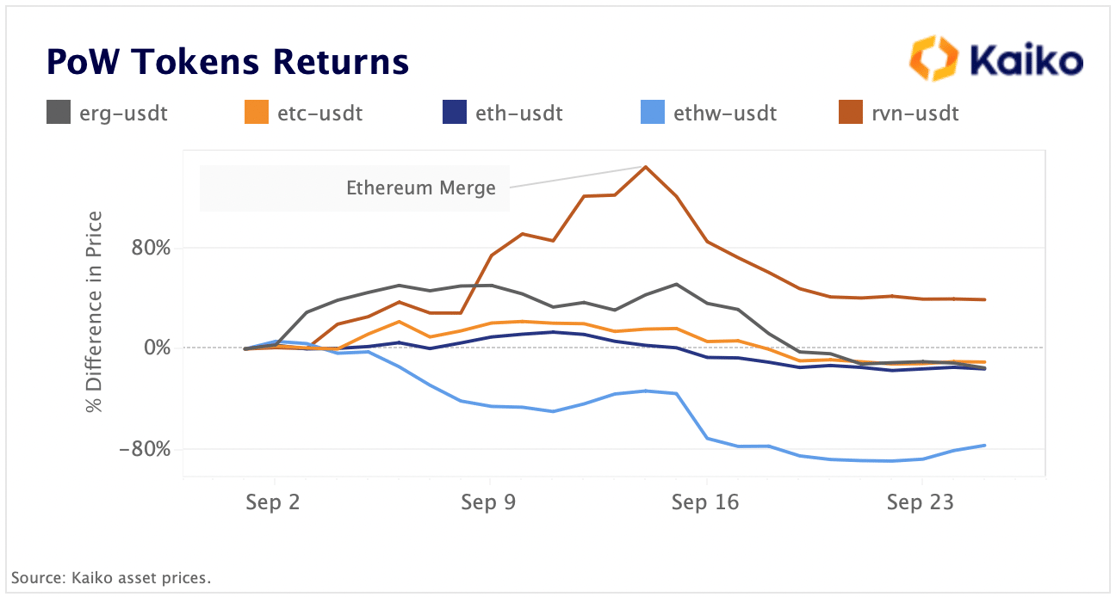

Proof-of-work tokens struggle post-Merge.

After Ethereum’s successful transition to the proof-of-stake (PoS) consensus mechanism, around one third of ETH miners have migrated to other networks while the rest have halted operations, according to WuBlockchain. While hash rates for proof-of-work (PoW) networks such as Ravencoin, Ergo and Ethereum Classic have soared, most PoW tokens have dropped sharply in line with the broad market. The token for the newly launched Ethereum hard fork, ETHW, is the worst performer, dropping over 70% since the start of September. On Sept 24th, ETHW volumes surged to all time highs, which suggests strong selling pressure. Ravencoin's RVN is the only PoW blockchain token up for the month, although its total market cap is just $430mn.

Market Liquidity

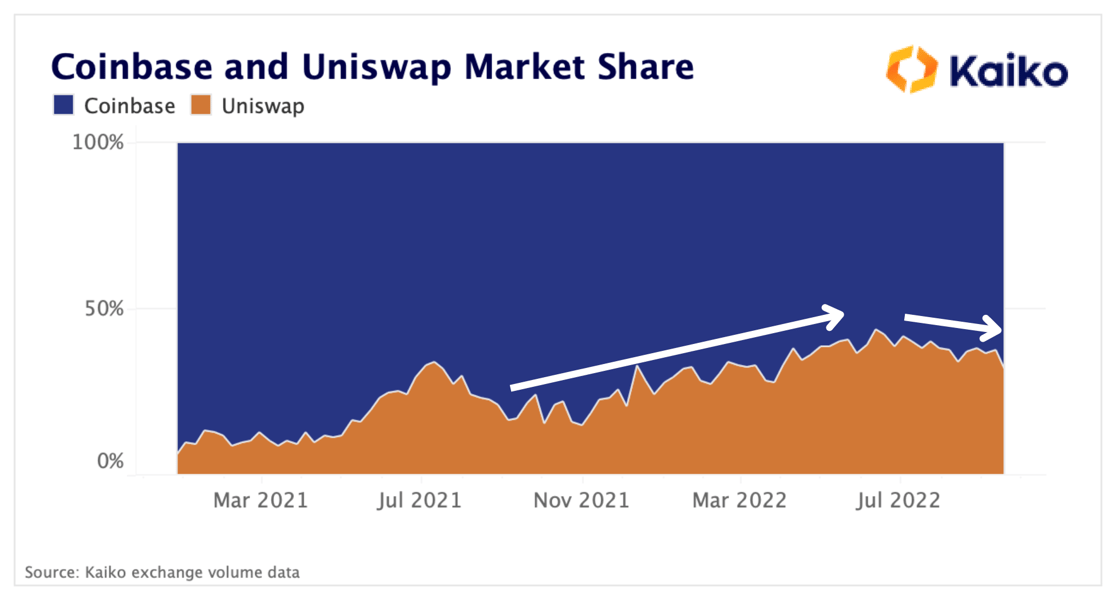

Coinbase regains market share to Uniswap.

In mid-July Kaiko reported that Uniswap (V2+V3) and Coinbase daily volumes were nearly even. Since then, this trend has begun to reverse, with Coinbase capturing 68% of volume last week. During the summer, Coinbase and Uniswap had weeks with a 55-45 split and on certain days Uniswap actually surpassed Coinbase’s volumes, which was a significant market event considering the secondary role decentralized exchanges have historically played to centralized platforms.

Volumes on centralized exchanges have been bolstered over the past month thanks to Merge-related speculation and repositioning. Meanwhile, on-chain activity has remained relatively flat, with little increase in volumes surrounding the Merge. Coinbase last week announced that it would be increasing fees for users with over $15mn in monthly volume, and we will be closely watching whether this impacts activity on the exchange over the coming months.

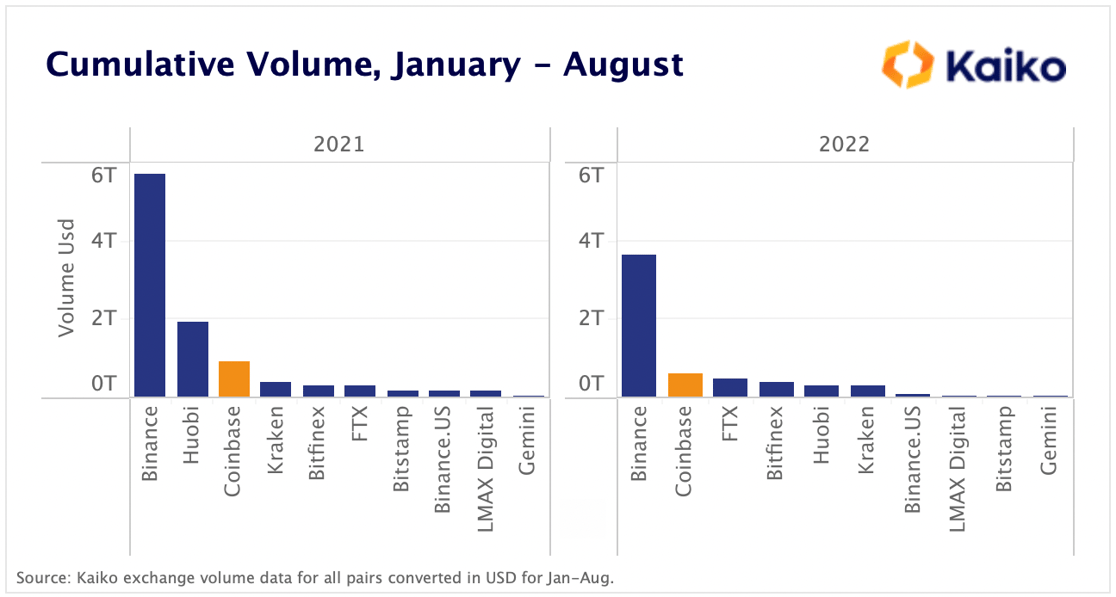

Now let’s take a closer look at how Coinbase’s volumes have fared in the bear market relative to a selection of the biggest spot exchanges. Below we chart cumulative trade volume in 2021 and 2022 for the time interval January to August. Despite a drop in cumulative volumes year-on-year, Coinbase has actually processed more trades than rival FTX, despite a drop in day-to-day market share.

Although Binance’s market share is at all time highs, the exchange has experienced a significant drop in cumulative volume processed throughout the same time interval last year, falling from nearly $6 trillion to just under $4 trillion. Huobi has been most impacted by the bear market, with 2022 volumes less than 1/4 what was processed during the same time in 2021.

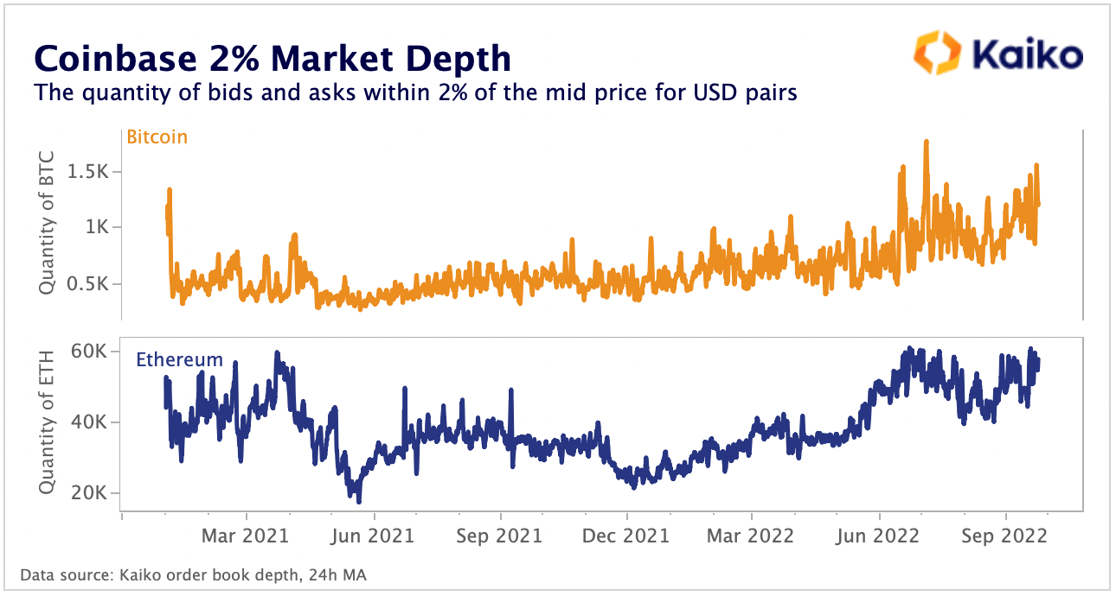

Now let's take a look at the underlying liquidity on Coinbase for BTC and ETH. Since the start of 2021, we can observe a strong increase in 2% market depth for the BTC-USD pair, rising from around 500 BTC on the bid and ask side throughout 2021 to more than 1.5k today.

ETH market depth started 2021 at around 40-60k before dropping off sharply throughout the year. Market depth has since recovered to ~60k in the run-up to the Merge. Overall, Coinbase remains one fo the most liquid exchanges in crypto as measured by volume and market depth.

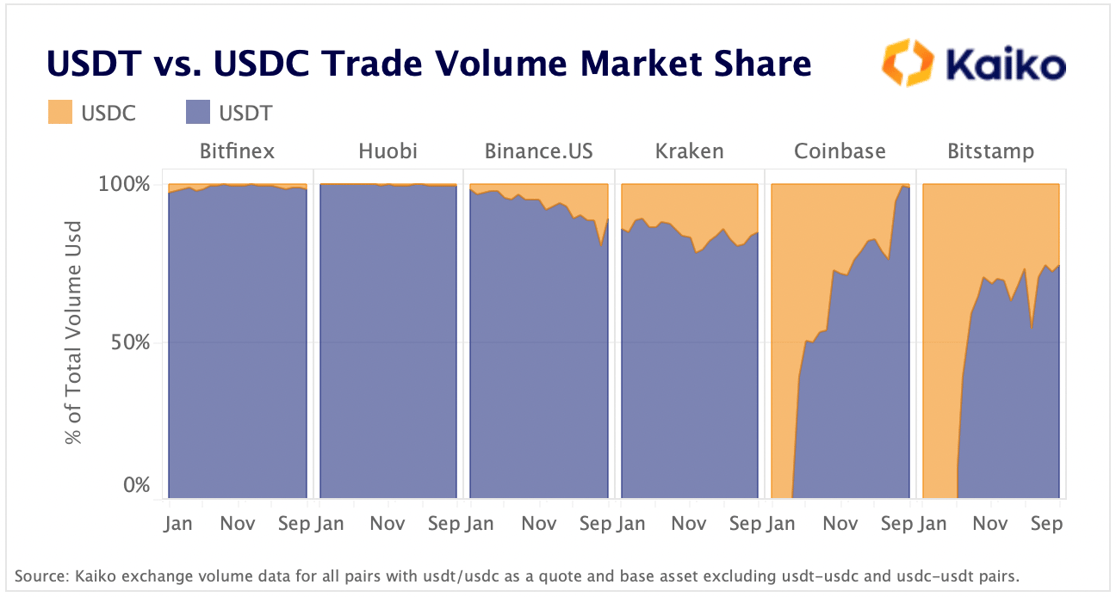

Stablecoin market share diverges across exchanges.

Tether’s USDT is by far the most popular stablecoin, commanding over 90% of aggregate stablecoin trade volumes on centralized exchanges. However, its market share does show slight variation depending on how regulated the exchange is. We compare the market share of USDT and its main competitor Circle’s USDC on 6 exchanges that list both assets.

On regulated US exchanges, USDC’s market share varies from 1% on Coinbase to 26% on Bitstamp. It is notable that USDC’s market share on Coinbase was fairly similar to Bitstamp’s - hovering around 26% - until the exchange merged its USD and USDC order books mid-July, effectively de-listing all USDC-denominated pairs. USDC’s share on Kraken and Binance.US – the US arm of Binance Global – has risen since the start of the year to 15% and 11% respectively. However, USDC has failed to gain traction on Huobi and Bitfinex - who shares a parent company with Tether - where its share of monthly trade volume remains below 2%.

Binance’s recent decision to delist USDC and move customers funds to its own stablecoin BUSD could pose a threat to USDT's dominance. The largest Indian exchange WazirX followed suit with a similar move last week. Tether remains by far the dominant stablecoin, but pending legislation in the US and continuing questions around its reserves could pose pose headwinds.

Derivatives

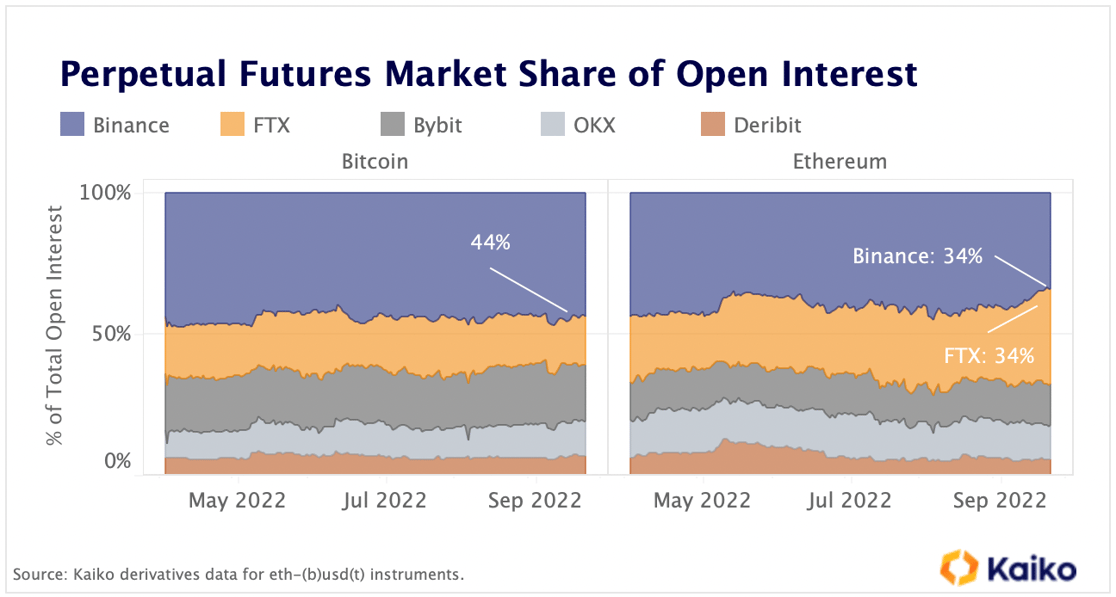

FTX gains market share to Binance in ETH perpetual futures.

While Binance has managed to significantly increase its spot volume market share after abolishing trading fees for Bitcoin and Ethereum pairs, it faces tougher competition in the highly segmented crypto derivatives market. This is particularly evident on ETH markets, which have seen stronger inflows than BTC markets over the past months ahead of the Merge. Bitcoin's open interest in native units (eliminating the price effect) is up 35% since June while ether's saw a 80% surge, hitting an all-time high in August.

Binance still holds over 40% share of BTC perpetual futures open interest. However, its market share on ETH markets has decreased and is now equivalent to FTX’s. FTX saw significant inflows with its market share rising from 25% in August to 33% in September despite ETH spot prices dipped below $1.4K post-Merge, prompting liquidations across derivatives markets.

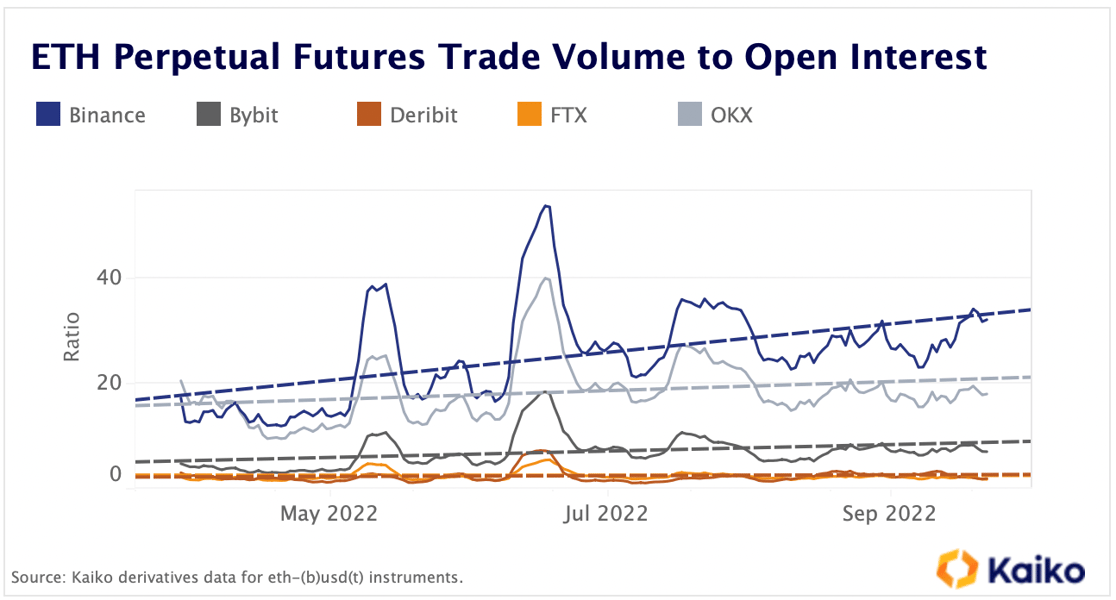

We further look at the ratio between ETH trade volume and open interest which could be seen as a measure of speculative activity. When the ratio increases, it means that perpetual futures trade volumes are rising faster than open interest which could indicate higher speculative activity as traders enter and exit the market within a short period of time (inflating volumes) while hedgers typically hold their positions for a longer period.

The ratio has increased on Binance, Okex and Bybit since April suggesting that these exchanges have managed to attract more speculative flows as traders positioned ahead of the long anticipated Merge. By contrast it has remained flat on FTX and Deribit.

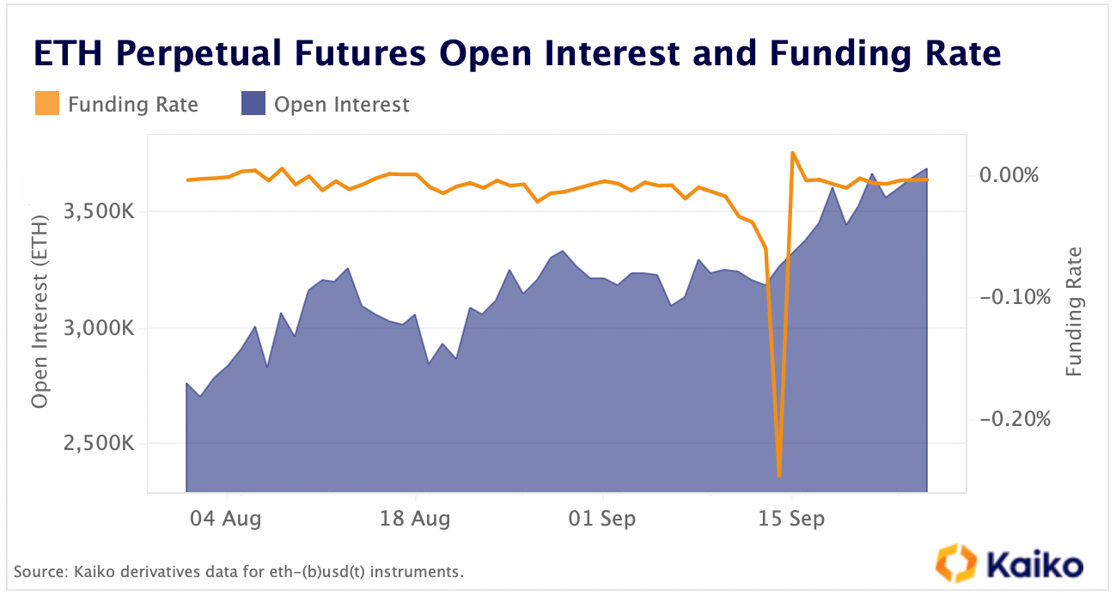

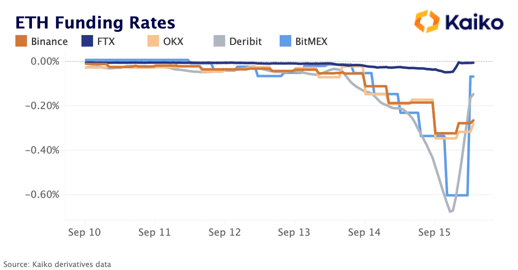

Overall, ETH open interest has continued to climb past all time highs following the Merge. Funding rates have reverted to neutral following a record-breaking dip negative.

Macro Trends

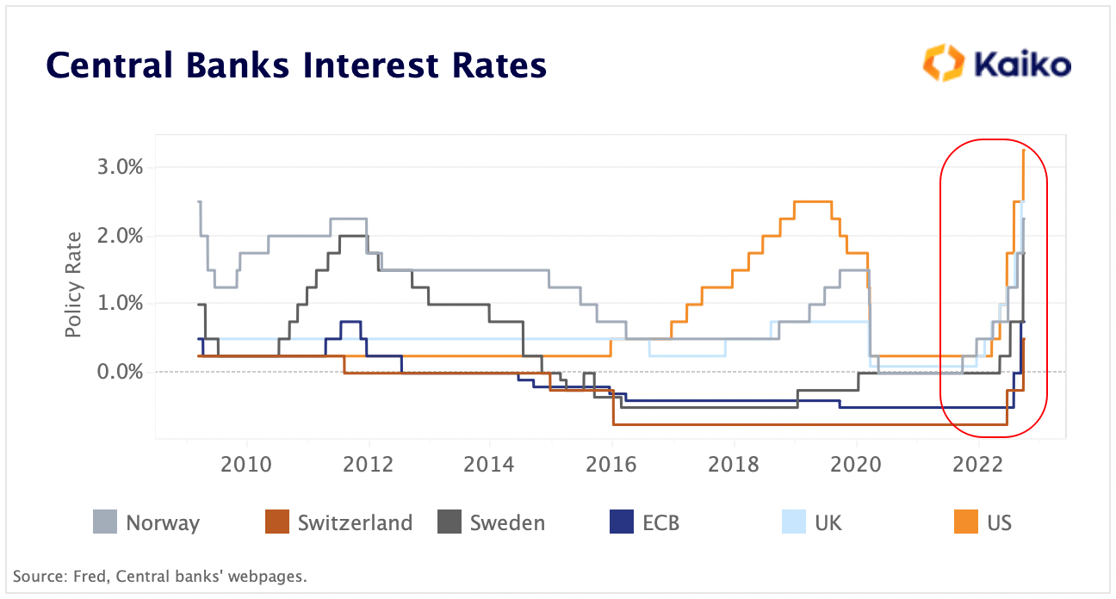

Risk assets face headwinds as global central banks ramp up inflation fight.

Despite mounting US recession risks, the Fed is leading the way among developed countries, raising its policy rate by 75bps for a third time in a row, totaling a cumulative 300bps in rate increases YTD. The Swiss National Bank ended a seven-year period of negative rates with a similar rate move while the Bank of Sweden hiked by a full percentage point. Over the past year, global central banks have shifted from an almost decade-long regime of low interest rates and ample liquidity to higher rates for longer to fight rampant inflation.

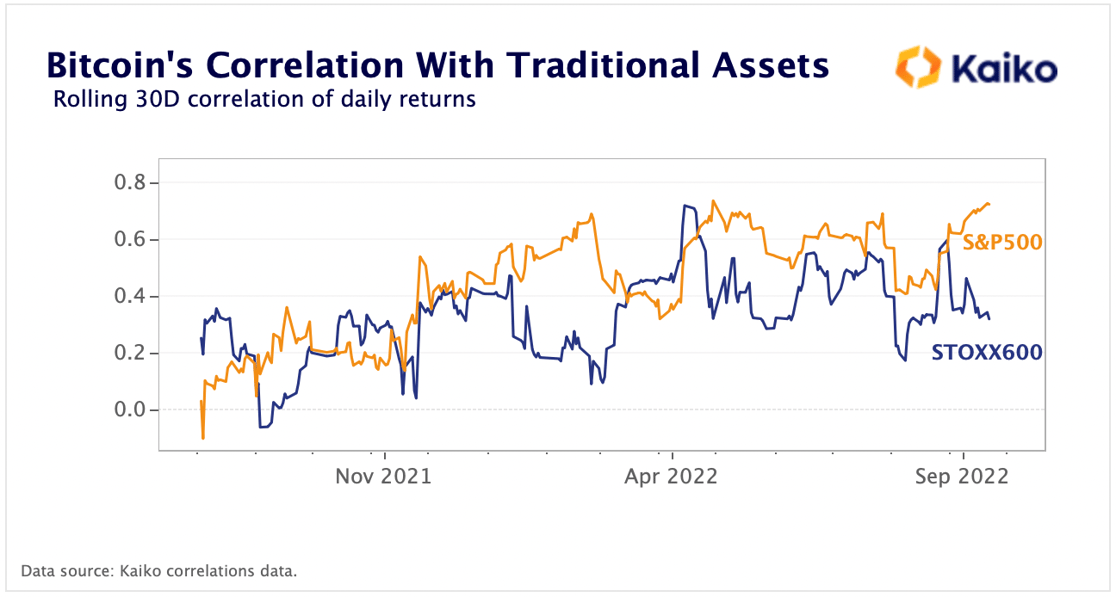

Typically, monetary policy tightening negatively impacts risk-taking and asset valuations. Immediately following the 75bp hike, the S&P 500 slid nearly 200 points. Last week Bitcoin’s correlation with the S&P 500 hit a fresh all-time high of .8 after declining throughout the summer.

Interestingly, BTC's price movements are more tightly correlated to US equities compared with European markets (as measured by the STOXX600 index). The divergence between European and US equities performance has deepened over the past few months as the ongoing energy crisis and renewed geopolitical worries have weighed particularly heavily on EU markets.

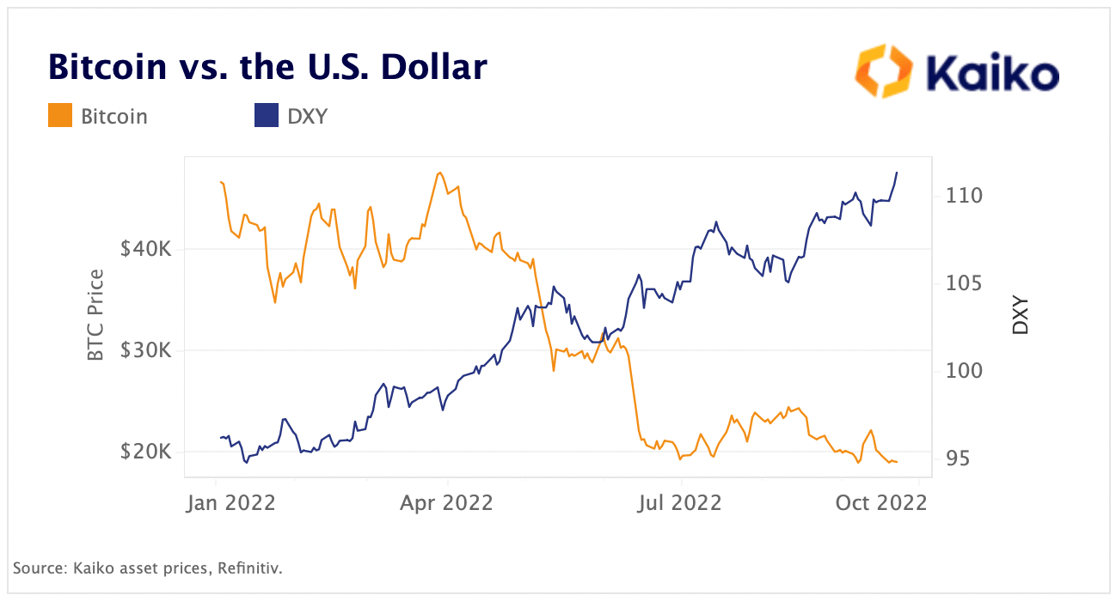

U.S. Dollar hits 20-year high.

The Fed's hawkishness and strong safe-haven demand continued to fuel the U.S. Dollar, which hit a fresh two-decade high last week. Bitcoin’s correlation to the greenback has been mostly negative over the past two years and is now nearing a yearly low of negative .5. The Dollar index (DXY) measuring the greenback’s performance relative to its main rivals is up 3.2% in September and 14.1% YTD . This has prompted an unprecedented intervention from the Bank of Japan - the first since 1998 - in defence of the Yen which touched the 145 level against the Dollar.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.