Three Arrows Capital famously blew up because of a series of bad trades, primarily Luna and GBTC. What happened to Luna is obvious: it went to 0 because of UST’s flawed peg maintenance mechanism. The GBTC situation was a bit more complex: “Grayscale allowed big investors like 3AC to purchase shares directly by giving Bitcoin to the trust. These GBTC holders could then sell the shares to the secondary market. That premium meant any sales could net an attractive profit for the big investors.” However, “shares bought directly from Grayscale were locked up for six months at a time. And starting in early 2021, that restriction became a problem. GBTC’s price slipped from a premium into a discount,” which was especially devastating for firms like 3AC, which used leverage to enhance its returns.

Essentially, 3AC made a bet that GBTC – a fundamentally different asset than BTC, with significant frictions in entrance and exit – would closely track BTC’s price. This saga has been front of mind as I’ve observed stETH (and other liquid staking derivatives) begin to displace ETH in DeFi protocols.

So, this week I’ll break down the significant differences between stETH and ETH and explain why investors and DeFi protocols should be much more cautious towards the former. Note that most of the issues I’ll lay out apply to all ETH LSDs, this will focus on stETH because it is by far the largest and most intertwined in DeFi.

stETH

Lido Staked ETH (stETH) is a tokenrepresenting“staked ether in Lido, combining the value of initial deposit plus staking rewards. stETH tokens are minted upon deposit and burned when redeemed.” stETH accrues yield, which is paid out to holders in the form of a rebase (i.e., the number of tokens one holds goes up automatically) every day at 12pm UTC.

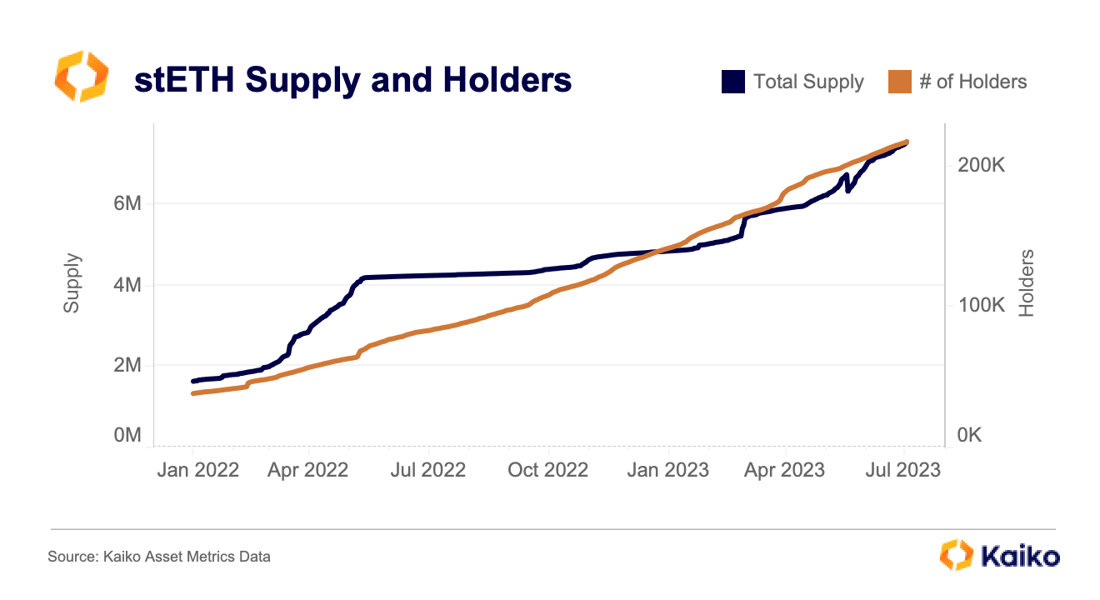

stETH has been one of the most successful tokens over the past year and a half, its supply growing fivefold from 1.5mn to 7.5mn while holders increased from 40k to nearly 220k. The only dip in stETH supply came as Celsius’s withdrawals wereprocessed.

So, what’s the problem? The problem lies not with stETH – a well-designed token that gives non-technical people access to ETH staking yield – but rather in how it is being utilized. This can be explained in two primary components: liquidity and leverage.

Liquidity

On-Chain

As a liquid staking derivative, liquidity is obviously paramount. Since stETH’s inception, Lido DAO has prioritized Curve’s stETH-ETH pool as the token’s primary source of liquidity. The DAO incentivized users to provide liquidity in this pool by providing LDO token rewards; without the incentives, it’s hard to justify LPing here, as users are essentially cutting their yield in half by being exposed to stETH and ETH instead of just stETH. Late last year, the DAO was distributing 2.5mn LDO tokens per month to liquidity providers (LPs) on Curve.

However, since June 2023, these incentives have been eliminated entirely, with the stated rationale that DEXes no longer have to be the primary source of liquidity because withdrawals have been enabled post-Shapella.

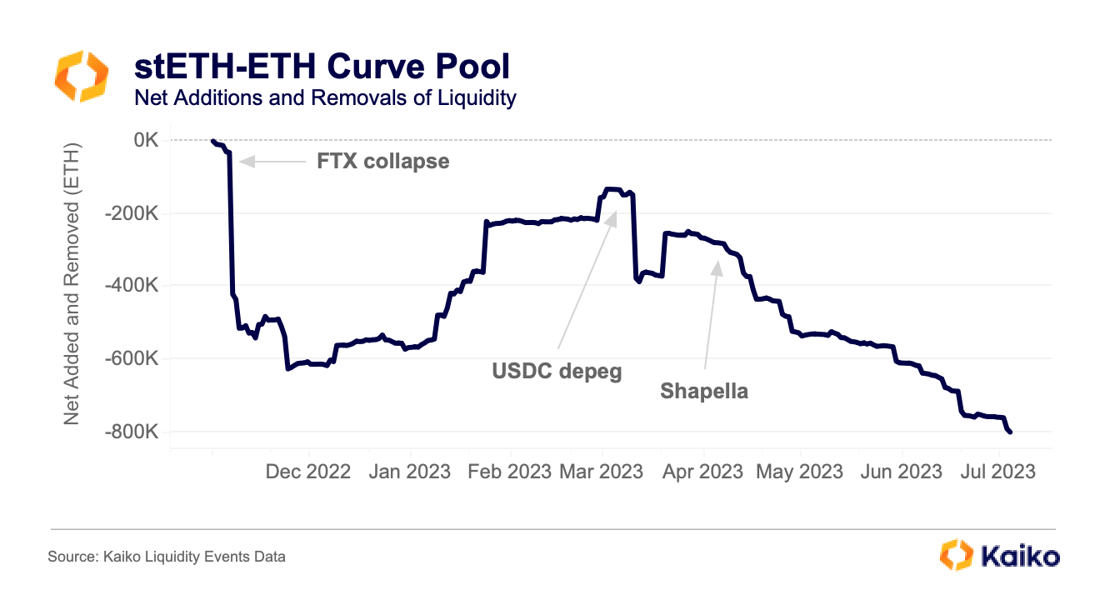

The chart below shows the net change in liquidity in the Curve stETH-ETH pool, beginning just before the FTX collapse.

In just one day, nearly 400k total ETH and stETH were removed from the pool. There was a partial recovery before over 200k was removed on the day of USDC’s depeg. Since Shapella, which enabled withdrawals of staked ETH, over 500k has been removed. Currently it holds 200k ETH and 201k stETH and is still the largest pool on Curve at $750mn.

The two main takeaways from this are: 1) the pool is prone to rapid contraction in periods of stress; and 2) there is a clear downwards trend since Shapella that is in line with Lido DAO’s assertion that DEXes will no longer be the primary liquidity venue for stETH.

However, the problem with relying on ETH withdrawals is the time delay; according to Lido a withdrawal can take 1-5 days under “normal circumstances” and takes longer during periods of high demand. It’s easy to imagine a scenario in which liquidity continues to dry up in Curve, a market event (like FTX’s crash or USDC’s depeg) causes even more liquidity to be removed, the withdrawal queue lengthens, and stETH holders want to swap into ETH, leading stETH to fall relative to ETH.

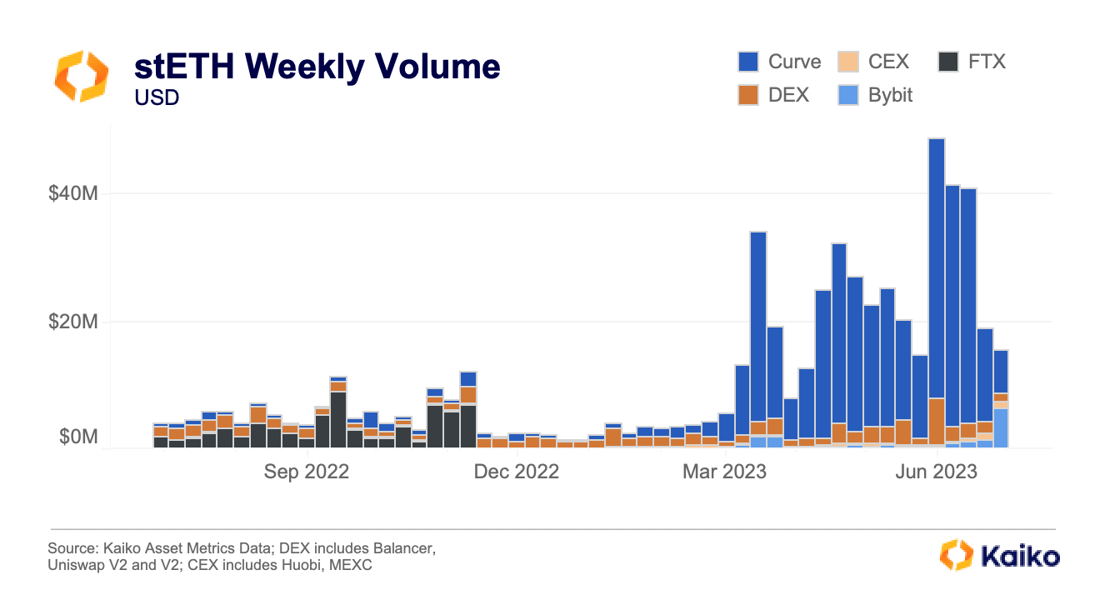

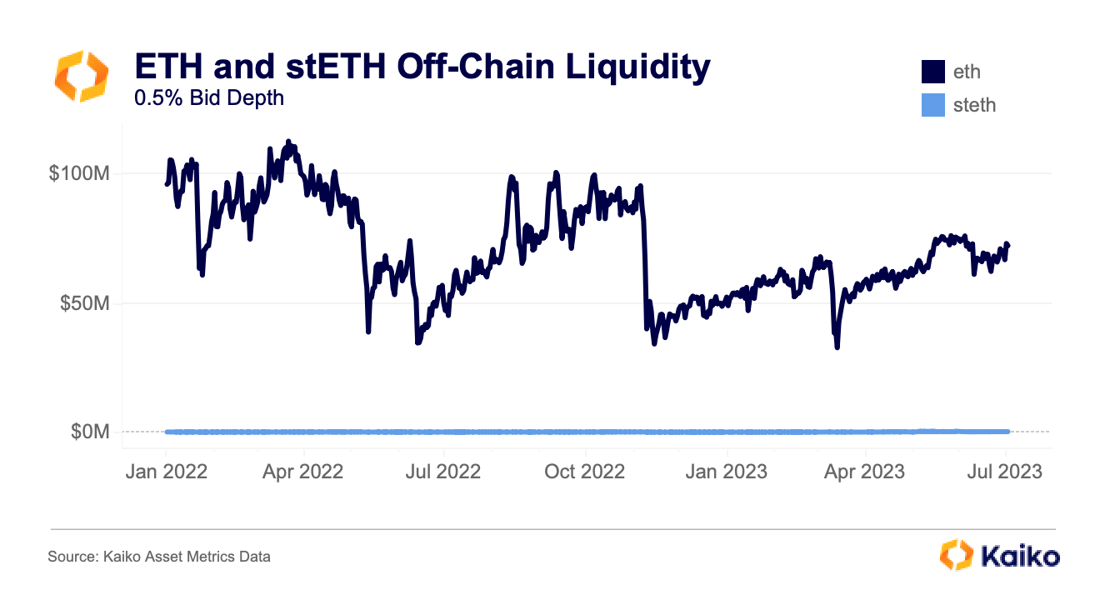

Unfortunately, there’s also a lack of liquidity off-chain. And, contrary to what some DeFi purists might believe, off-chain liquidity does matter for stETH. In fact, last week Bybit facilitated almost exactly the same stETH volume as Curve. This was the first time a CEX registered a significant portion of volume since the fall of FTX.

Despite increasing CEX volumes, stETH’s off-chain liquidity is extremely poor. stETH is the seventh largest token by market cap but its liquidity doesn’t register on a chart with ETH, with just $185k in bids within 0.5% of the mid price, aggregated across all exchanges. It is 400 times less liquid than ETH.

Off-chain liquidity is particularly important for any DeFi protocols that use an oracle, especially for stETH-USD. As I write this, the 19 Chainlink oracles for stETH-USD are reporting prices between $1,906.98 and $1,919.60 and are very likely incorporating CEX prices to generate these prices. The lack of off-chain liquidity makes these oracle prices more volatile, which is especially important when considering our next topic: leverage.

Leverage

As I wrote in a previousDeep Dive, lending and borrowing protocols have shifted from places to deposit ETH and borrow a stablecoin to LSD leverage machines.

About one month after stETH was added to Aave V2 it became the most deposited asset, while ETH borrows skyrocketed from under $200mn to $1.6bn in just two months. This is in large part due to the popularity of manually leveraging stETH: depositing stETH into Aave, borrowing ETH, swapping or staking it for stETH, and repeating as many times as one is comfortable with. This is the process that starts to sound concerningly similar to 3AC’s GBTC trade, where the founders assumed that GBTC would trade closely with BTC. However, just like GBTC and BTC, stETH and ETH are fundamentally different. Deteriorating on-chain liquidity makes these huge leveraged positions appear riskier than ever.

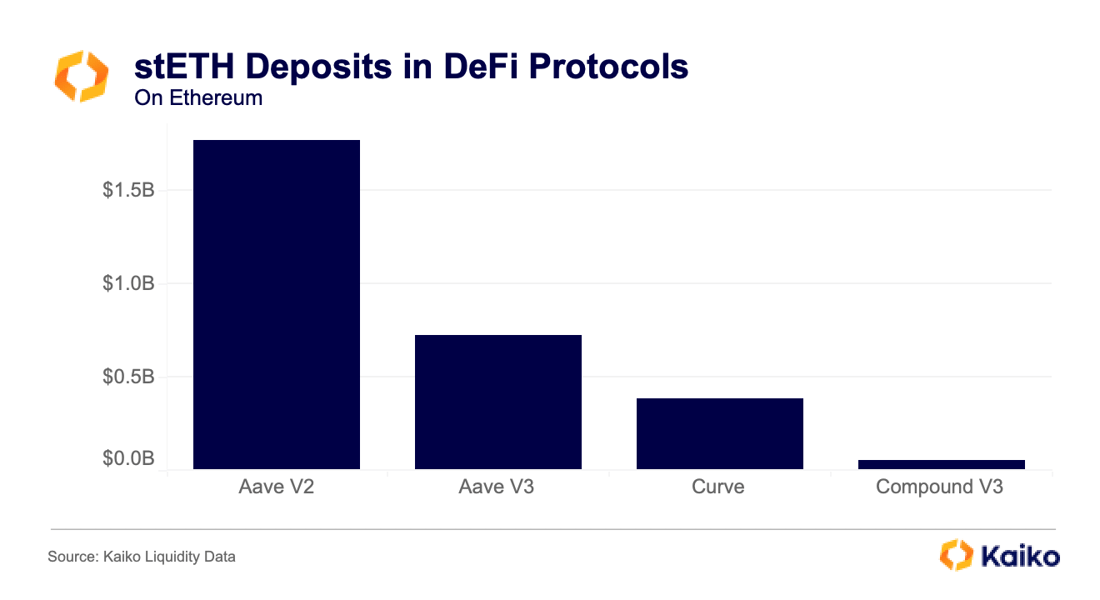

To put this all into perspective I’ve charted the amount of stETH deposited into the major Ethereum DeFi protocols.

There is almost $1.8bn worth of stETH deposited into Aave V2 and a further $750mn deposited on V3. On Curve, $385mn stETH is paired with roughly $385mn ETH. Compound V3 rounds it out with $60mn stETH deposited. This is essentially an amplified version of the problem I wrote about two weeks ago, where there’s insufficient on- or off-chain liquidity to liquidate such a large position, potentially saddling the lending and borrowing protocol with significant bad debt.

Conclusion

The combination of deteriorating liquidity and increasing leverage makes a large liquidation event more likely. Again, this is not a flaw in stETH but rather in how it is being used. In fact, any significant liquidation event that increases the stETH discount could present an incredible opportunity for anyone brave enough to catch the dip. It is important for DeFi protocols and investors to be aware of the increased risks that come with stETH relative to ETH; too many mistakenly assume that stETH’s discount will always be low or that longing stETH and shorting ETH is delta-neutral.

For its part, Lido DAO should continue to be mindful of both on- and off-chain liquidity. The DAO understandably grew tired of providing such large incentives in the Curve pool, but with those incentives eliminated (for now) the DAO should seriously consider paying a market maker to provide liquidity on a variety of centralized and decentralized exchanges, which I suspect would be more cost efficient than the previous method.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-Jul-06-2023-02-13-50-6478-PM.png?upscale=true&width=1100&upscale=true&name=image%20(5)-Jul-06-2023-02-13-50-6478-PM.png)