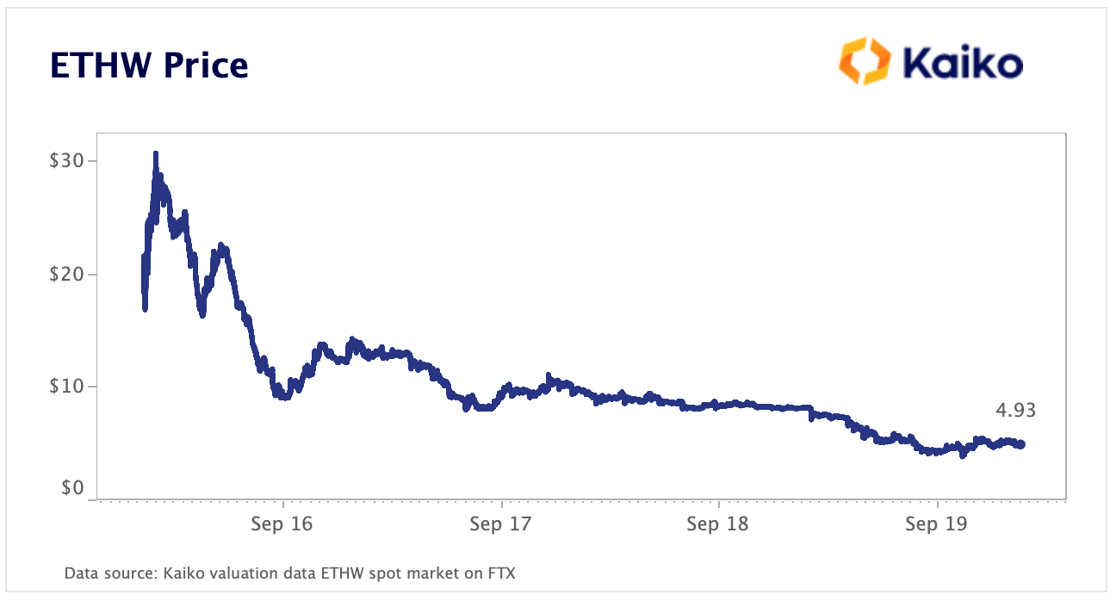

Ethereum Proof-of-Work has gotten off to a rocky start. ETHW, the token representing the new hard-forked Ethereum network, has fallen more than 80% since it listed on FTX. The overall poor rollout of the network was exacerbated by glitches and the emergence of a competitor fork called EthereumFair, which was backed by the exchange Poloniex.

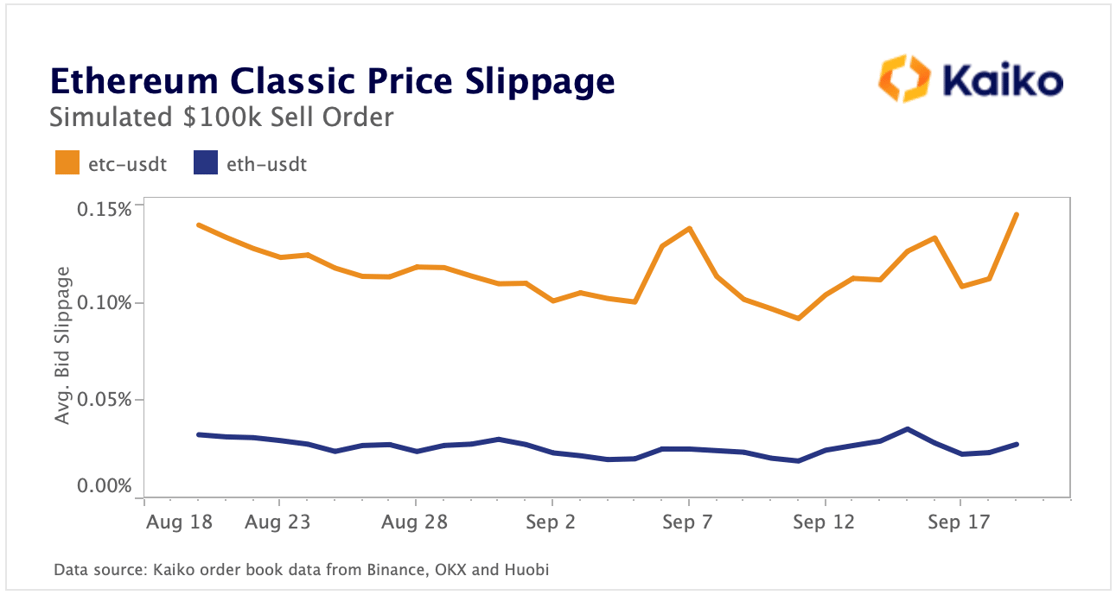

Meanwhile, Ethereum Classic, one of the first hard-forked Ethereum networks, saw a surge in hash rate as miners transitioned to mining ETC following the successful completion of the Merge. Ethereum Classic forked in 2016 but over the years has failed to gain significant market share or usage. ETC is down 25% on the week and and has very poor liquidity on centralized exchanges, which could pose problems for new miners hoping to cash out.

Were miners to sell their ETC on the spot market, they would be looking at nearly 5x the slippage on a $100k market sell order than they would have when selling ETH. This added cost is the next in a long line of problems for ETH miners going forward as they scramble to remain relevant, and most importantly, profitable.

Price Movements

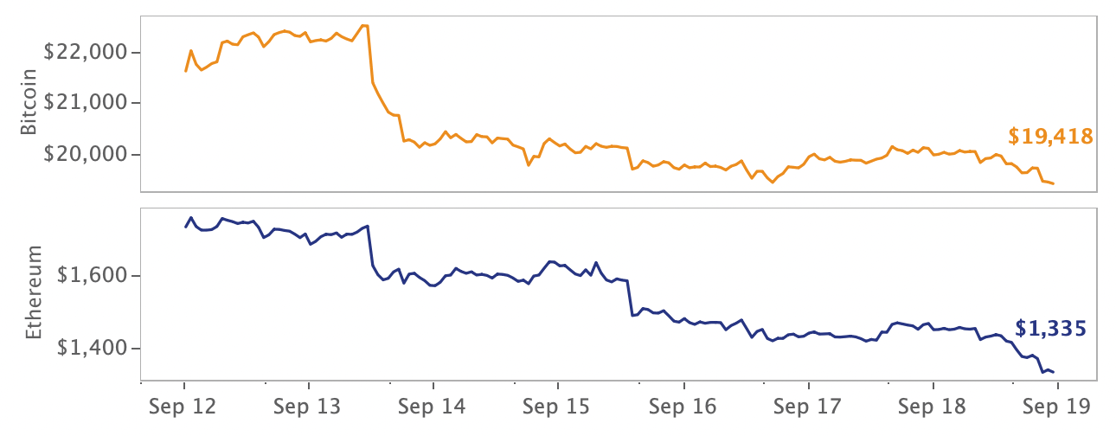

Post-Merge sell-off sweeps markets.

In what many expected to be a positive week for the price of ether, a successful Merge ended up preceding a significant sell off of roughly 25% on the week. ETHW and ETC were also some of the week's worst performers in a sign that old Ethereum miners will struggle to remain profitable. In broader industry news, a South Korean court issued an arrest warrant against Terra founder Do Kwon, the Blockchain Association formed an industry PAC, and Wall Street firms Charles Schwab, Citadel Securities, and Fidelity Digital Assets announced the launch of a new cryptocurrency exchange, EDX Markets.

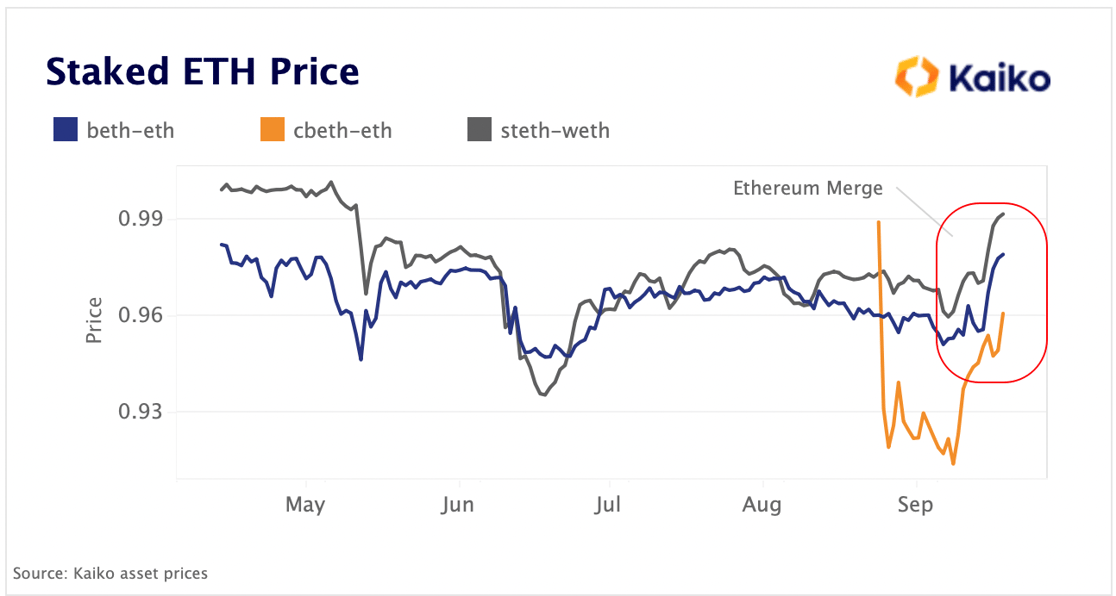

Staked ETH discount narrows to lowest level since May.

The discount on staked ETH tokens relative to spot ETH has narrowed to its lowest levels since May, a trend which first emerged in the hours after the Ethereum network's successful transition to proof-of-stake. Liquid staking derivative tokens such as Coinbase’s cbETH, Binance’s bETH and Lido’s stETH are wrapped versions of ether staked on Ethereum’s consensus layer - the Beacon chain. They are not pegged to ETH and their market price takes into account a number of regulatory and smart contract risks. For example, if a staker is "slashed", which happens in the event of validator failure, a portion of staked ether could be at risk.

The sharp narrowing of Lido’s stETH discount from 4% to just 1% was supported by increasing liquidity in Curve's stETH pool, which is the largest secondary market for staked ether. cbETH and bETH markets also saw strong buy pressure immediately after the Merge (we discuss the post-Merge market reaction here). While the trend suggests some risk premium has been taken off the table, the staked ETH discount will likely persist until the next Ethereum upgrade enables staking withdrawals sometime next year. However, the opportunity costs of holding ETH has now increased (as staking offers additional rewards) which could provide some tailwinds for staked ETH markets.

Market Liquidity

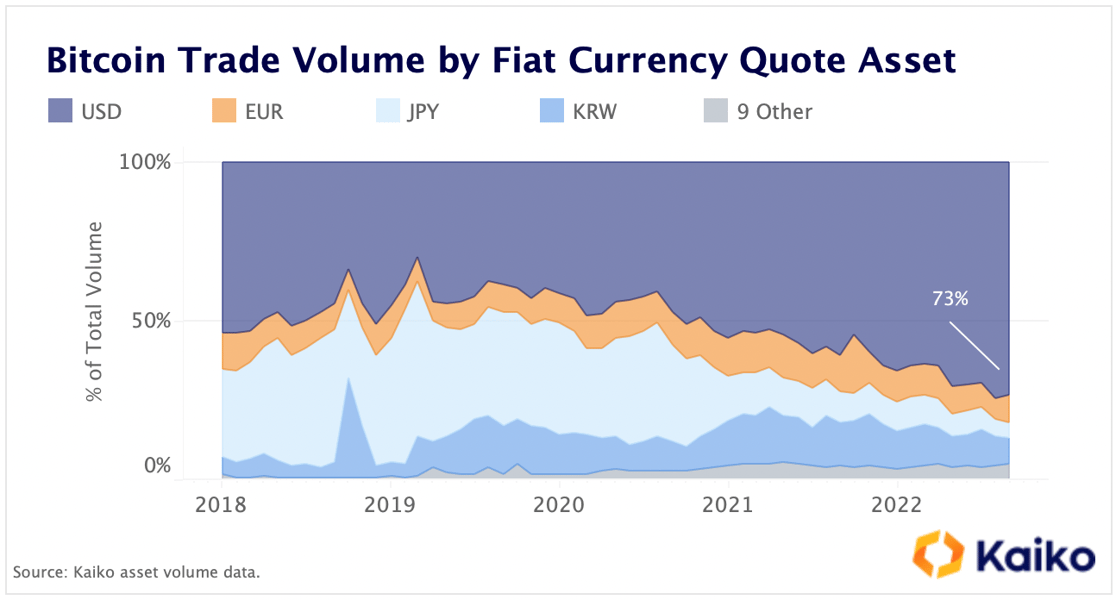

The U.S. Dollar remains the dominant fiat currency in crypto.

While the majority of cryptocurrency transactions are conducted today using stablecoins, fiat currencies still serve as a critical on and off-ramp to markets. Historically, the U.S. dollar has been the most important fiat currency in crypto, but how has its role changed over time? The share of bitcoin traded against the U.S. Dollar has increased significantly since 2018 and currently exceeds 70% of total bitcoin-fiat trading volumes.

The trend could be explained by rising institutionalization of the market, as large investors typically prefer transacting in dollars. However, a closer look at the breakdown by fiat currency suggests that local regulations could have also played a role. Notably, BTC volumes on Japanese markets have declined sharply with Japanese-based exchange Liquid registering a five-fold drop in annual trade volumes between 2018 and 2021 after suffering a $97mn hack and stricter Japanese regulations. For context, the amount of BTC traded on USD markets rose by 30% over the same period.

Fiat market share will likely continue to evolve as regulatory regimes become clearer around the world. For example, Japan is reportedly considering loosening its screening rules for new assets. For now, the dollar still reigns supreme.

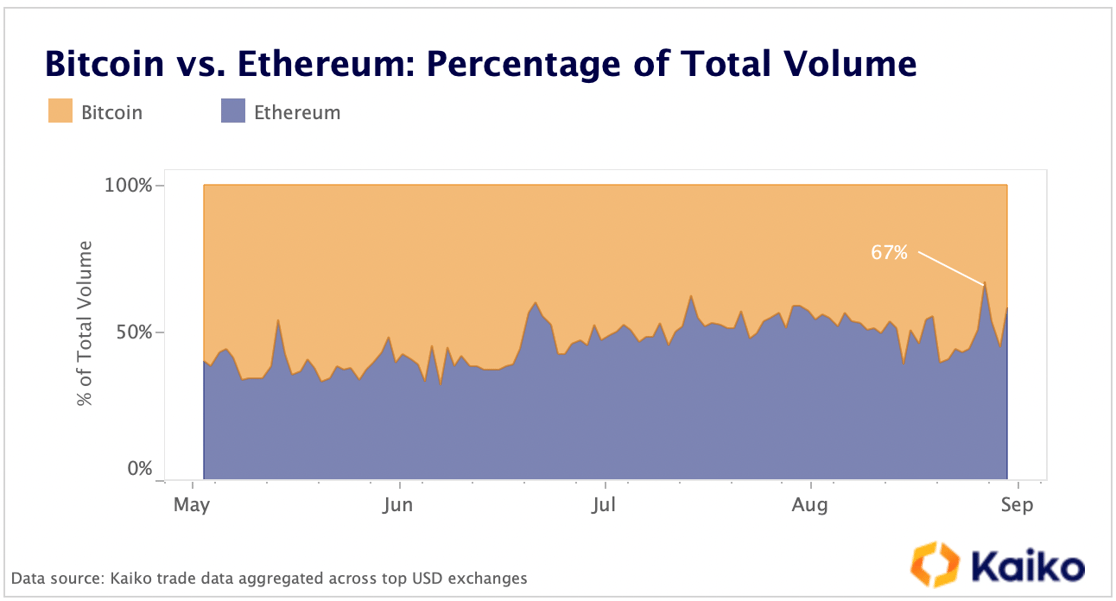

ETH market share hits all time high during post-Merge sell-off.

Ether’s market share of trade volume hit an all-time high of nearly 70% relative to bitcoin’s during the post-Merge selloff last week. Large liquidations of leveraged long positions across derivatives markets exacerbated the drop in spot prices, causing spot volumes to surge. Overall, ETH's market share has more than tripled since 2020, suggesting a durable shift in market structure away from BTC.

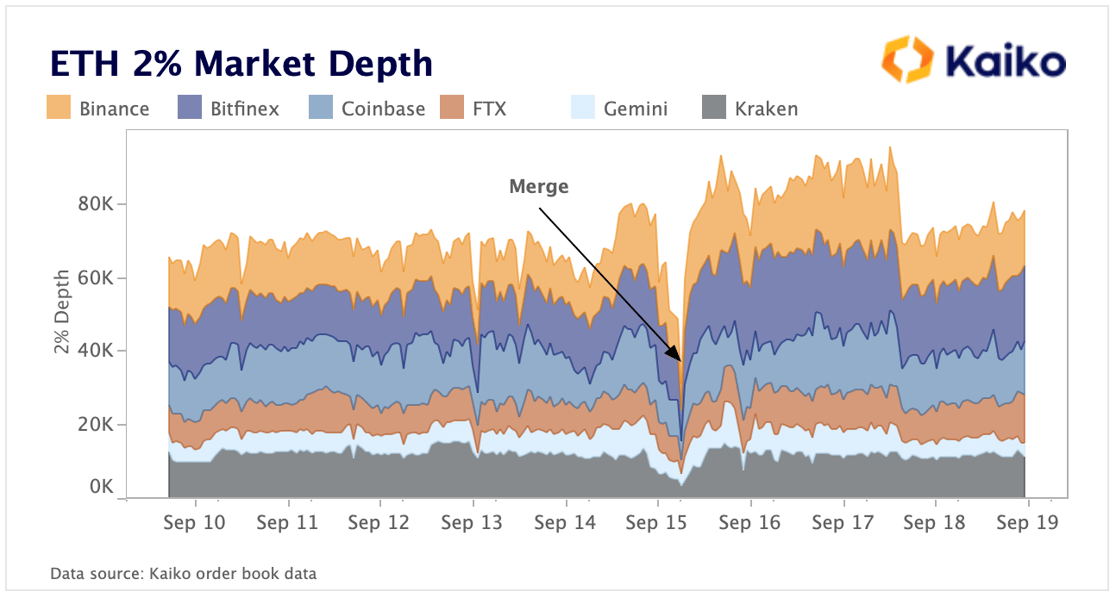

As volumes surged, liquidity evaporated for ETH spot markets, as measured by the quantity of bids and asks within 2% of the mid price on ETH-USD(T) order books. This suggests market makers were apprehensive and removed liquidity to avoid being caught in Merge-related volatility. Liquidity was quickly re-added in the aftermath, and now sits just slightly above the levels we saw pre-Merge.

While ETH continues to slightly underperform Bitcoin YTD, the expected decline in its issuance is likely to provide support to its price despite the challenging macro environment.

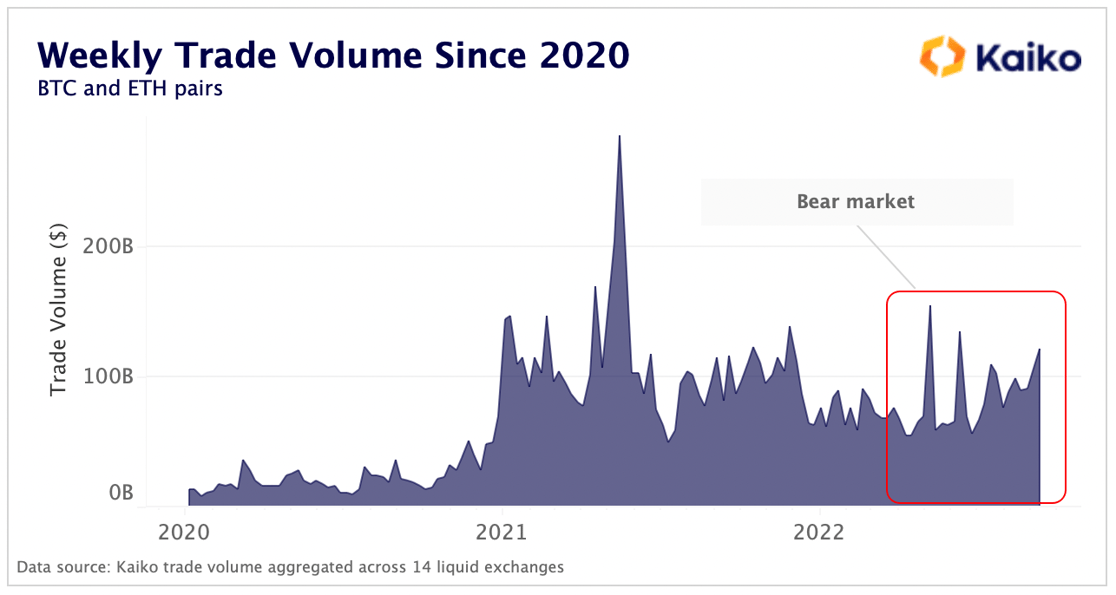

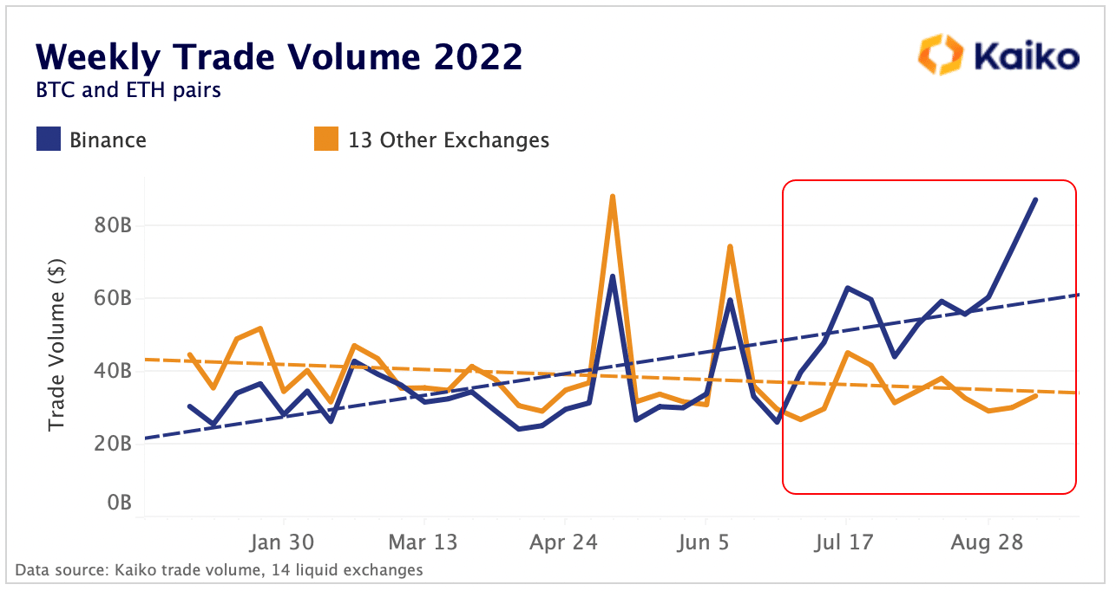

Binance bucks trade volume trend.

Trade volume is one of the best indicators of a prolonged bear market. An initial price slump is typically accompanied by a surge in trade volume as traders take advantage of (or suffer) from volatility. However, as days turn into weeks turn into months of depressed prices, volumes start to drop off across most exchanges. Yet, when looking at aggregated volume for the most liquid BTC and ETH pairs, we can observe no such trend since the start of the bear market in May. While weekly volumes remain well below all time highs, there has actually been a slight up-tick in activity over the past few months.

Unfortunately, aggregated data can obfuscate exchange-level trends. When separating Binance from this aggregated dataset, we can a strong divergence in activity between the world's largest exchange and 13 other exchanges. Ever since Binance removed trading fees for BTC/ETH pairs, they've experienced a massive surge in volume. For the first time, Binance market share has climbed well beyond aggregated volumes for 13 other exchanges (including Coinbase, FTX, Huobi, Okex, etc.). Since the start of 2022, volumes have actually trended down on all exchanges except Binance, matching what we would expect of a bear market.

Eliminating trading fees for the most liquid pairs is not something most exchanges can afford to do, so we will likely expect a continuation of this trend until markets correct.

Derivatives

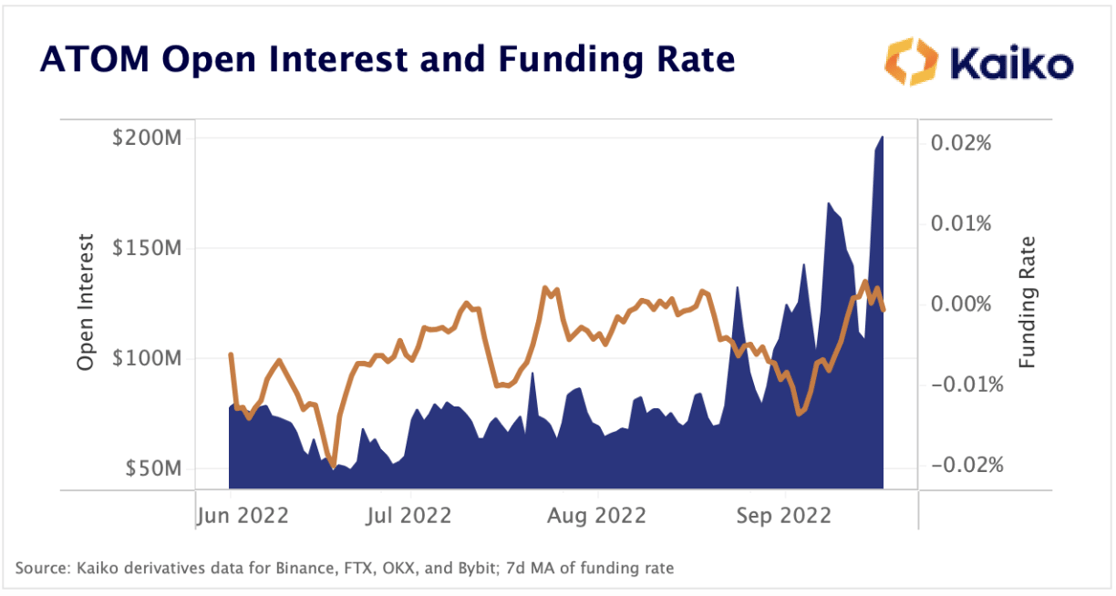

ATOM open interest surges amid bullish streak.

Cosmos’s token ATOM has been one of the few bright spots in a bleak few months for crypto prices. Cosmos is a decentralised network composed of independent and interoperable blockchains which aims to become the “internet of blockchains” enabling them to share data and tokens within its ecosystem.

ATOM is up over 40% in the past four days, though the token is down 54% year-to-date (competitors like SOL and AVAX are down 82% and 85%, respectively). Following the collapse of Terra, which was part of the Cosmos ecosystem, a number of other projects have grown to begin to replace its activity, including Kava, Osmosis, and Thorchain. Additionally, it is widely expected that the team will soon announce new tokenomics for ATOM that will reduce inflation and increase the token’s utility. Amidst these positive catalysts, open interest has surged from under $50mn in mid-June to over $200mn now. The average funding rate has been on an upwards trend since the beginning of September, suggesting this latest surge in open interest is skewed towards the long side.

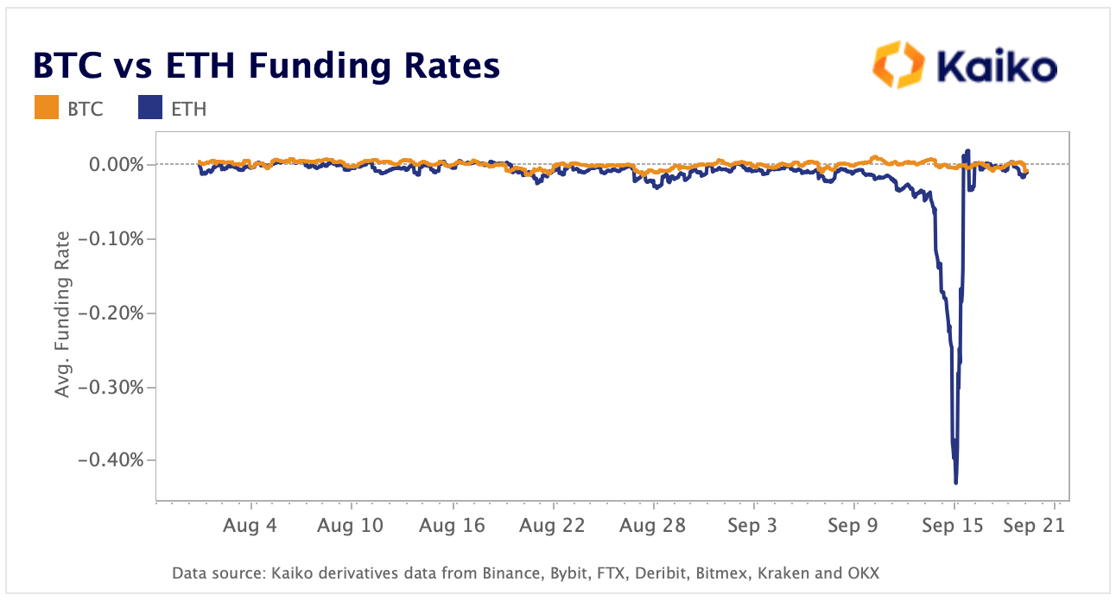

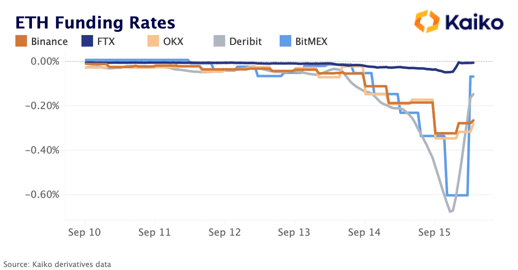

ETH funding rates stage dramatic recovery.

ETH funding rates moved sharply off their all time lows post-Merge as the ETHW airdrops began and futures prices no longer needed to account for a potential arbitrage. Investors were taking advantage of the ETHW airdrop by combining their long ETH spot positions with short ETH futures, eliminating price risk while still being able to collect the ETHW airdrop. Were futures prices not discounted to reflect this strategy, this strategy would have also profited on the short futures side of the trade. Once the Merge was successfully completed and the airdrop of ETHW took place, futures returned closer to spot prices and thus the funding rates moved sharply towards neutral again

Macro Trends

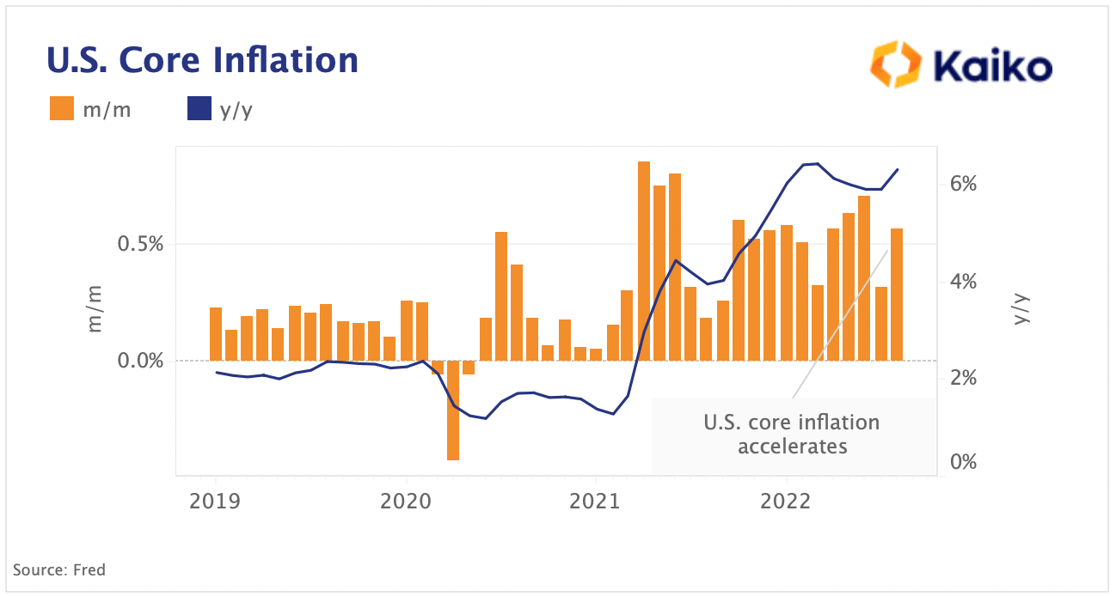

Hotter than expected U.S. inflation boosts Fed hike bets.

Macro headwinds continue to weigh on financial markets after a hotter than expected monthly US inflation print for August caused both crypto and equities to crash. Headline inflation came at 8.3% year-over-year, slightly lower relative to July’s numbers. However, the monthly core inflation went up by .6%, almost double the estimates. The core inflation excludes volatile food and energy prices and is considered stickier and costlier to hedge than headline or energy inflation. Fears that bringing down inflation will be a slower and more painful process than anticipated boosted an aggressive repricing in the Fed peak rate which is now seen above 4%. Markets are widely expecting another large 75bps rate hike at this week’s Fed meeting while bets for a super-sized full percentage move are on the rise.

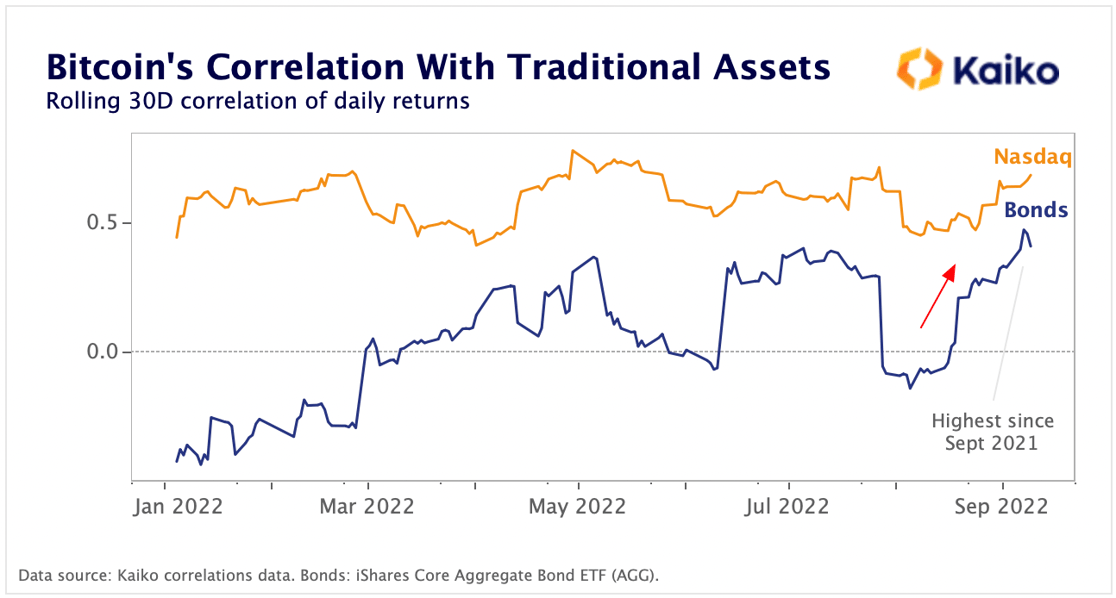

Bitcoin’s correlation with bonds and equities rises in September.

Bitcoin’s correlation with both bonds and equities has resumed its increase in September after declining over the summer. Inflation uncertainty coupled with Fed tightening has resulted in a historical decline in both risk and fixed-income assets, challenging traditional asset allocation approaches. The iShares Aggregate Bonds ETF, which tracks the U.S. investment-grade bond market, declined by 12% YTD, the Nasdaq 100 lost 28% of its value while Bitcoin is down over 50%. Recent research shows that persistently high and more volatile core inflation could be among the explanations for the positive correlation between bonds and risk assets over the past months, as inflation negatively impacts all asset classes.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.