The Kaiko Research team is thrilled to introduce our first Quarterly Market Report! Through 20 jam-packed pages, we provide data-driven analysis of Q3's most significant market events. We cover the Ethereum Merge, macro volatility, Nomad bridge exploit, Binance's fee elimination, the crypto credit crisis, stablecoin regulation, and much (much) more. In today's Deep Dive, we provide a sneak peak of the report along with analyst commentary highlighting our favourite trends.

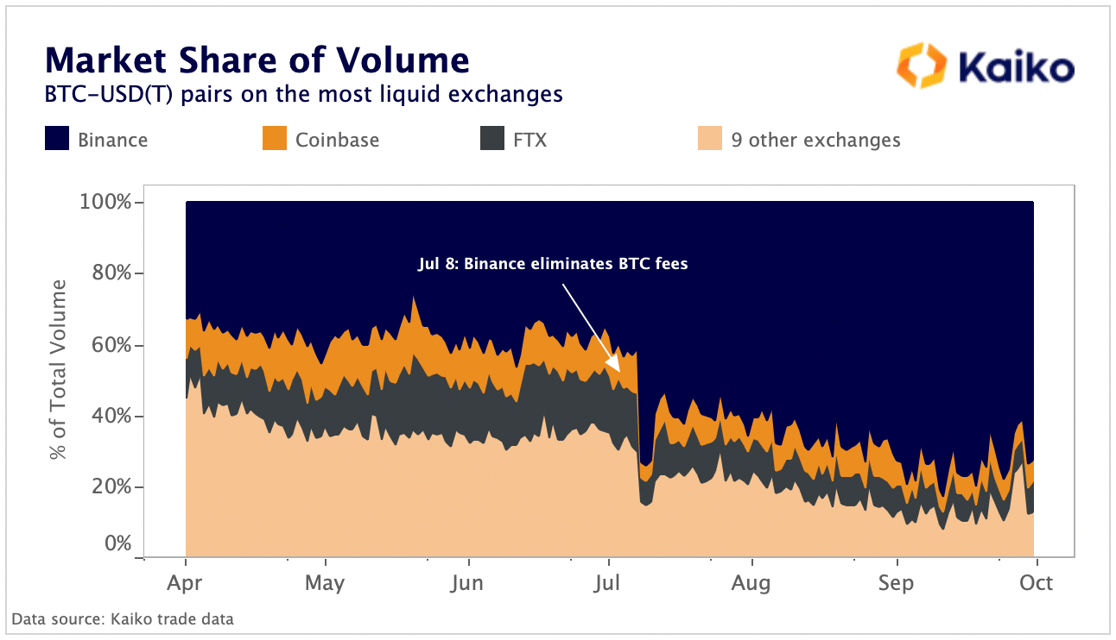

Q3 was a whirlwind dominated by macro volatility, the Merge, and the ongoing fallout from the crypto credit crisis. Yet, one relatively under-the-radar trend caught my attention: Binance’s increasingly bold moves to clinch market supremacy. On July 8th, Binance eliminated trading fees for 13 BTC trading pairs and shortly after removed fees for ETH-BUSD. This action was of near unprecedented scale in the history of cryptocurrency markets, especially considering Binance’s BTC-USDT pair is the most liquid in crypto.

The exchange essentially decided to sacrifice profits earned from ~$5bn in daily volume. Not only that, these 13 pairs + ETH-BUSD accounted for more than half of total volume on the exchange at the time fees were eliminated.

The move has certainly paid off when looking at market share, with Binance steadily climbing to almost unbelievable highs throughout Q3. Binance's BTC volume is now greater than the combined volume of 11 other of the most liquid cryptocurrency exchanges, including Coinbase, FTX, Okex, and Kraken.

Binance has a massive war chest that can handle a sharp drop in revenues and this move is clearly part of a longer-term strategy to siphon traders from its competitors. But the question remains, how long can the exchange maintain zero fees, especially in a bear market? Other exchanges will surely respond with their own promotions and altered fee structures, but will it be too late?

The exchange fee war is just getting started and there's nothing like a bear market to trigger consolidation in a heavily competitive industry.

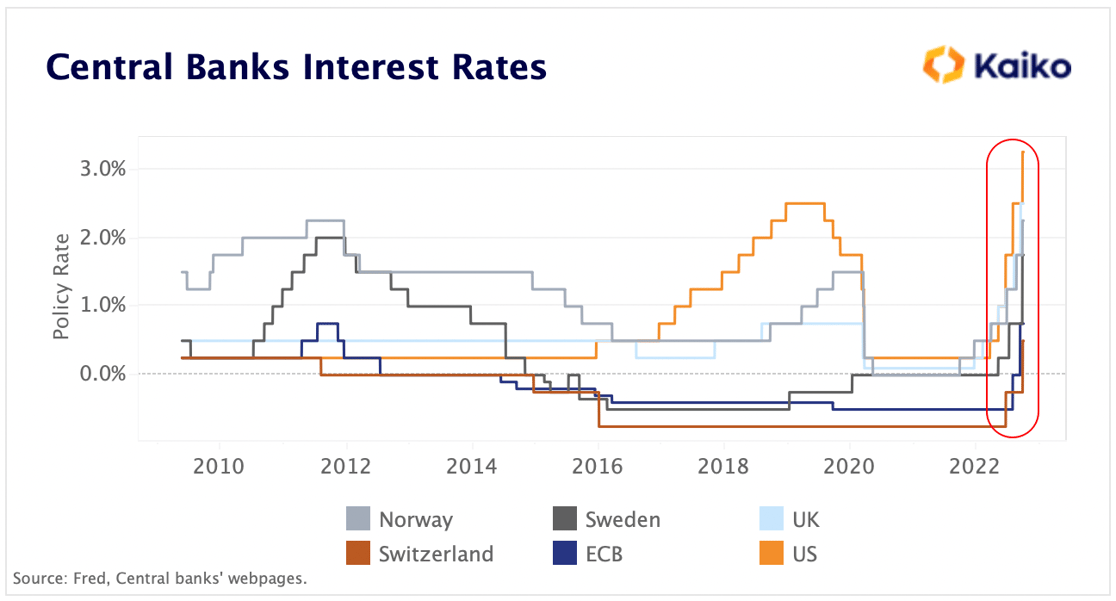

Despite outperforming traditional assets in Q3, crypto markets continued moving in sync with global risk sentiment. This was well-illustrated by the summer’s crypto recovery which coincided with revived expectations for an early dovish pivot in U.S. monetary policy. After U.S. core inflation continued climbing in September, the Fed (as expected) hiked rates while doubling the pace of its quantitative tightening (i.e. balance sheet reduction). Other major central banks followed suit with both the European Central Bank and the Swiss National Bank exiting a multi-year period of negative interest rates.

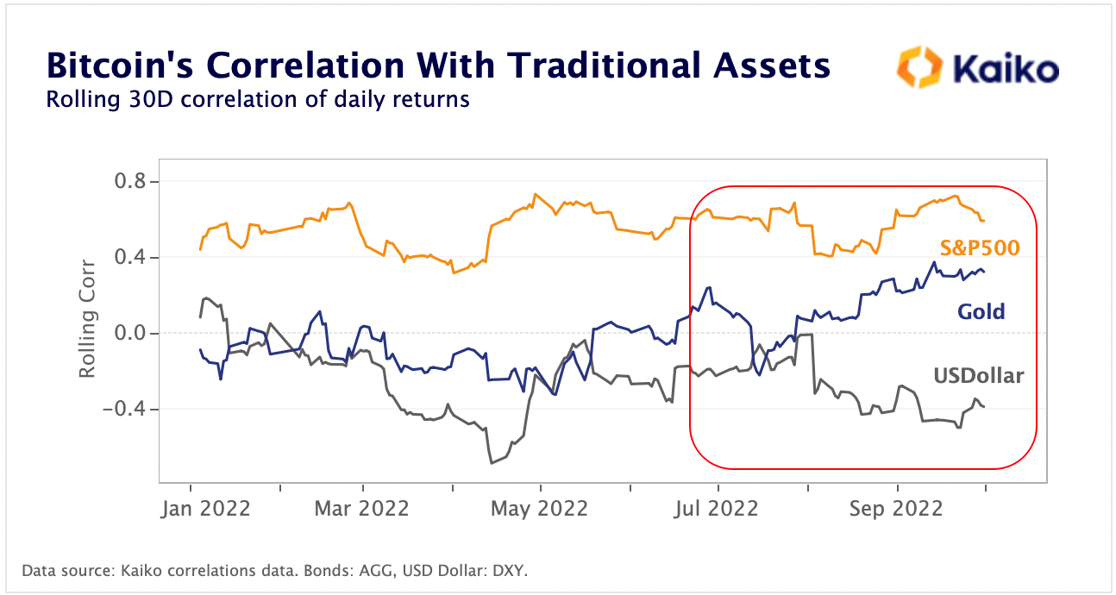

This led to a broad risk-off sell-off across asset classes, including crypto, causing Bitcoin’s correlation with the S&P 500 hit a fresh all-time high in September. BTC's correlation with Gold also hit yearly highs as the traditional safe haven continued its descent.

By contrast, the crypto asset's correlation with the US Dollar - which was the main beneficiary of the Fed’s hawkishness over the past months – remained firmly negative. Several currencies including the Euro and the Japanese Yen hit historical lows against the greenback. FX volatility reached a boiling point in September when the British pound (GBP) fell to a record low and the Bank of England was forced to intervene.

Data releases are likely to keep generating volatility for crypto markets in the coming months with recession fears on the rise as the global economy shows signs of weakening. The fast-evolving pace of US and EU crypto regulation will be among the major market movers, potentially offering much-needed clarity to the industry in the coming months.

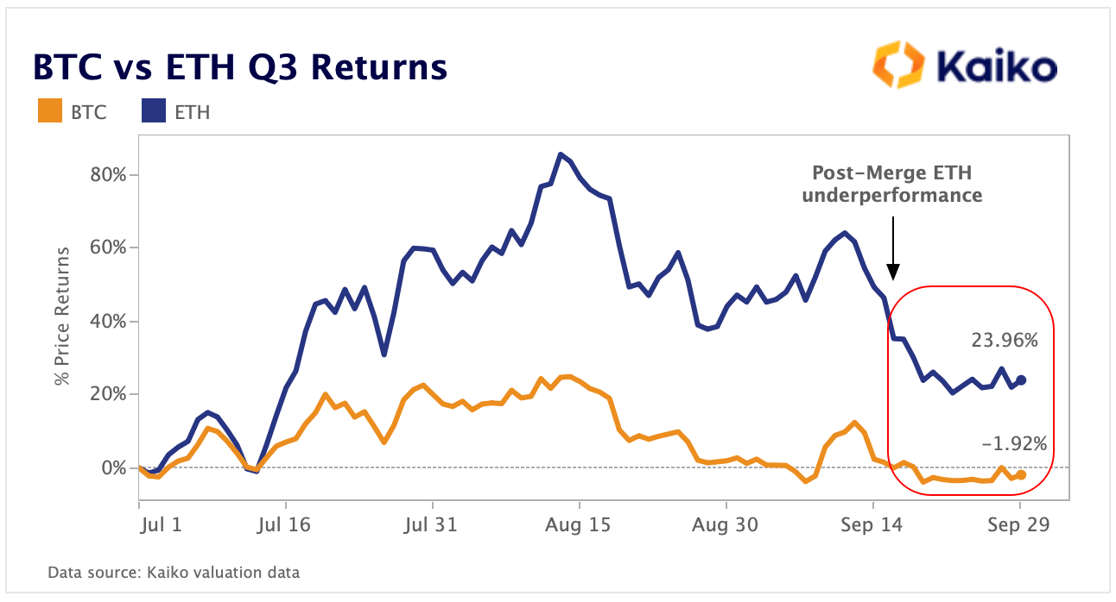

The most interesting thing for me about the Ethereum Merge has been the sheer inability for crypto, or more specifically ETH, to stage a meaningful rally in the face of macro headwinds. No-one would disagree with the fact that the Merge went as well as it could have. Even the test runs in the buildup had some minor glitches, but the main event had virtually none.

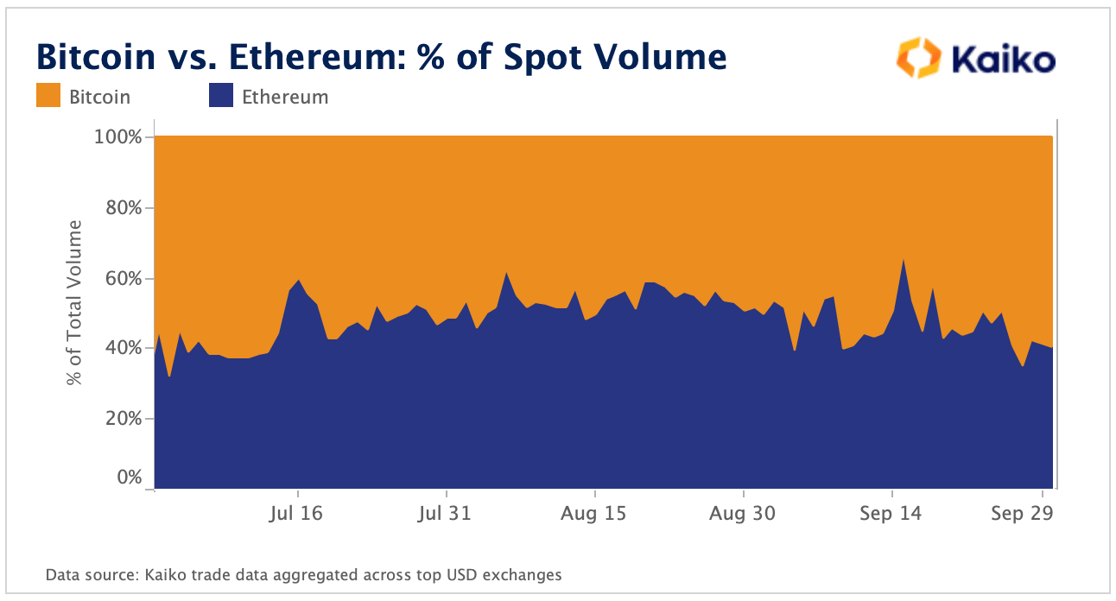

Ethereum now runs away in the background on proof of stake like the whole transition process was no big deal. That’s remarkable in itself, but what’s even more remarkable was that this feat has led to an underperformance vs BTC since the Merge of -12%. However, this starts to makes a bit more sense when you zoom out to pre-Merge and see ETH’s dominance relative to BTC in both price and volumes traded. The ETH Merge trade was a crowded one with ETH commanding equal spot volumes to BTC pre-Merge, which have since reverted to over 60:40 in favour of BTC as investors seem to be unwinding their “long ETH into the Merge” positions.

What’s interesting to me going forward is how soon we’ll see institutional investment in ETH now that it’s got two big pull factors on its side post Merge: 1. Uses 99% less energy, which has been talked about ad nauseam at this stage and 2. Now has a benchmark staking yield. This staking yield could be particularly interesting to newcomers to web3 looking to engage in proper risk management. There is now what could be seen as the first “risk-free” rate in crypto against which all other risk can be assessed. Big caveat there in that there is still ETH price risk if converting back to fiat, which is significant, but even with that it is possible to use derivatives to remove that price risk. The result of this benchmark yield should be a more robust DeFi ecosystem and more transparent risk management - both of which should bolster institutional adoption in the next bull market.

The question now is how long a gap there will be between institutional adoption, which will undoubtedly only happen when prices start going back up, and the more risk-conscious, short term selling we’re seeing at the minute. I think once we get the first sniff of a pivot from the Fed, which could be as early as the end of this year, money will start flooding in to Ethereum and crypto as whole.

Terra’s collapse continued to weigh heavily this quarter, as previously unknown links between CeDeFi companies (i.e., Voyager and Celsius) manifested in balance sheet holes and consumers losing access to their funds. This summer was a constant stream of headlines detailing something breaking. What didn’t break? DeFi.

Through the most stressful period in its short existence, DeFi continued to function as promised. DEXs worked and maintained volumes better than many CEXs. Lending and borrowing continued to operate normally. Liquid staking platforms weathered the storm and generated some nice returns for those who bought when others were panicking. And this happened all while CeDeFi companies were liquidating hundreds of millions of dollars worth of DeFi positions and Ethereum was changing its consensus mechanism. Yes, there were exploits and casualties along the way, but the blue chips proved why they’re blue chips.

Blue chips chugged along, but this was also one of the most exciting quarters in DeFi innovation since summer 2020. Quality layer 2s and alternative layer 1s garnered real adoption that wasn’t based around incentives or airdrop hunting. The lower transaction fees on these networks allow more frequent trading and improvements to UI/UX make some decentralized futures exchanges feel like centralized exchanges without the downtime.

So, DeFi is here to stay and CeDeFi is dead or nearly dead, though no one should be shocked when charlatans resurrect it with new buzzwords and attractive yields in the next bull run.

What happens next? Price-wise, macro is still king. Regulation remains a big unknown, though I’m skeptical of any one government being able to kneecap DeFi. DeFi protocols have now had years to learn from the failed ponzinomics of the past and are well positioned to lead whenever the Fed decides to pivot.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.