Our FTX Deep Dive is finally here. Hats off to our on-chain peers, who provided essential intel revealing the tangled web between FTX and Alameda. From us, you will get all things markets, chronicling the liquidity crunch that precipitated the death spiral of FTT, which triggered the collapse of one of the largest cryptocurrency exchanges in the world.

The FTX Collapse: A Market Analysis

November 10, 2022

By Clara Medalie, Riyad Carey, and the Kaiko Research team

First came the Terra collapse. Then the bankruptcies of the centralized lenders. And now the (almost certain) insolvency of FTX, one of the largest cryptocurrency exchanges in the world.

FTX’s collapse has shaken the industry to its core, in part because it is a fundamentally different type of business than a crypto lender like Celsius. FTX is a cryptocurrency exchange. The service it provides is that of a facilitator of trades: they earn a transaction fee for every trade executed by one of their clients. FTX is neither a trading firm nor a lender, so theoretically, they should at all times have access to the equivalent of 100% of their client’s funds.

But we now know that that was not the case due to a dangerously intertwined relationship with FTX’s sister company, the trading firm Alameda Research, and the improper use of FTX’s native cryptocurrency, FTT.

Following a mass exodus of funds, FTX halted withdrawals shortly before Sam Bankman-Fried (“SBF”) announced a “strategic transaction” from its competitor Binance to ensure “customers are protected.” Binance has since said that it would not go through with the deal (some reports said FTX US would have to be included for Binance to consider it), stating that “the issues are beyond our ability to control or help.” SBF reportedly informed investors on Wednesday that FTX would need to file for bankruptcy, with a hole of up to $8bn.

Ironically, FTX has issued more than $750 million in credit lines to distressed crypto companies that ended up insolvent largely because they misappropriated their client funds. While we still don’t know the extent of the balance sheet hole, or whether an acquisition will materialize, the crypto industry has just undergone an era-defining realignment.

Let’s dive in.

FTT: A Cursed Concoction

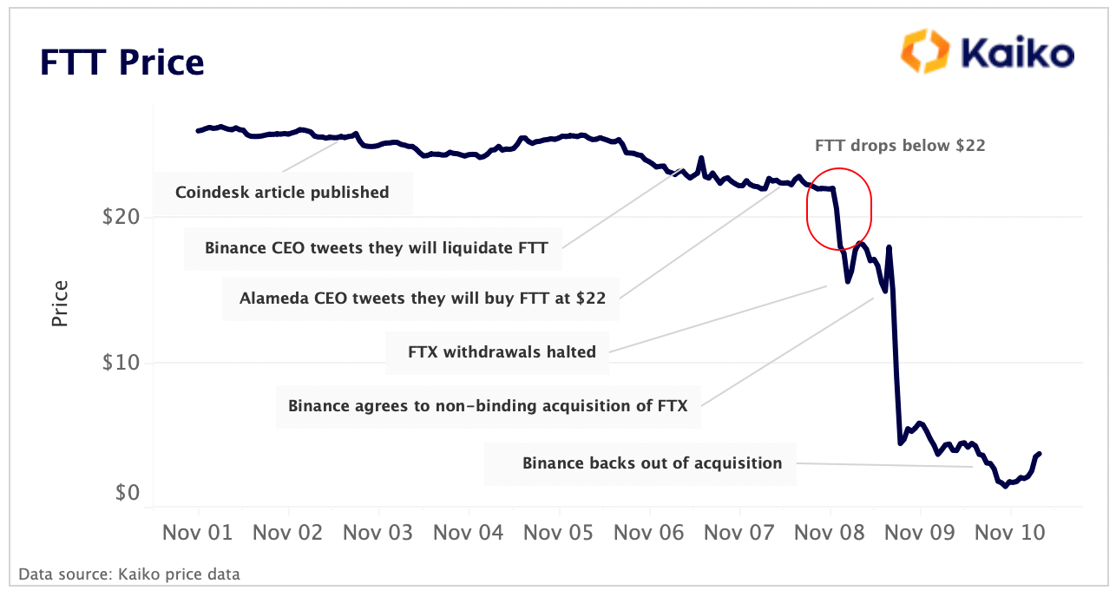

The rapid unwinding of one of the world’s largest exchanges all started with an investigative story from CoinDesk, reporting that Alameda held a significant portion of its balance sheet in FTT, a cryptocurrency created by FTX. This instantly raised questions about FTT, namely: what is its actual purpose?

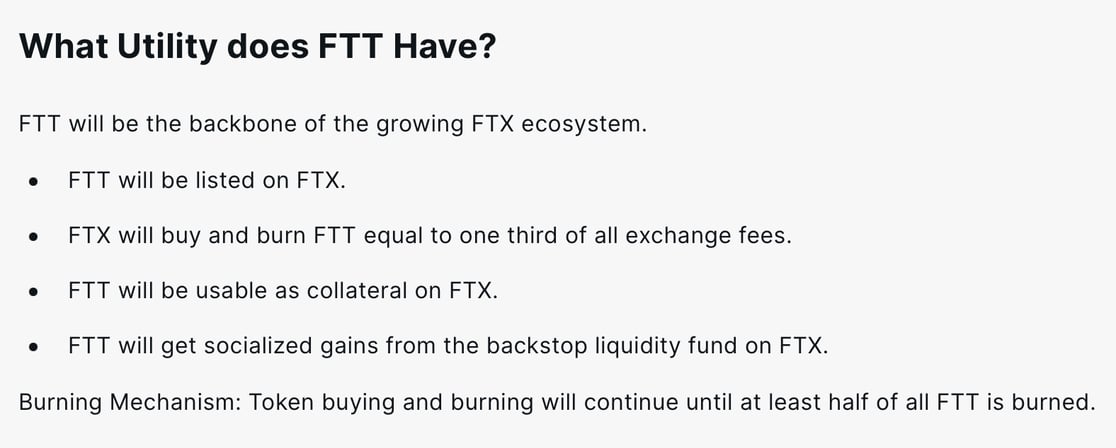

Cryptocurrency exchanges have long issued their own tokens, which generally have few benefits beyond giving holders discounts on trading fees, but have rarely received scrutiny. As described in FTX’s FAQ section, here is FTT’s utility:

The more we learn about FTT, the more it seems that this concocted cryptocurrency underpinned a significant portion of the FTX/Alameda empire. The token has (had?) extremely limited utility, but it is was used extensively as collateral: in DeFi, inside FTX, and on the books of Alameda.

The CoinDesk investigation revealed that Alameda not only had a lot of FTT on its balance sheet, but it also had been using FTT as collateral for loans. This alone should raise alarms, but the bigger question is: who had accepted billions of dollars worth of FTT as collateral? New reports suggest that the lender in question is none other than FTX, which we can deduce thanks to the work of some on-chain sleuths.

Alameda suffered massive losses during the May market crash along with most other cryptocurrency hedge funds, which FTX tried to repair using its own funds in exchange for FTT as collateral. In all likelihood, a portion of these very funds belonged to their clients.

The information on Alamada’s balance sheet was enough to cause Binance CEO Changpeng Zhao (“CZ”) to declare that Binance would liquidate all of its FTT holdings (received as part of its exit from FTX equity), which at the time was worth about $500mn. That’s when things started to unravel.

An Illiquid Token

FTT is a relatively illiquid token, trading actively on just 10 exchanges for a total of 23 spot markets. For comparison, BTC has ~370 spot markets, SOL ~80, and DOGE — a memecoin — more than 130.

Following CZ’s tweet, Alameda CEO Caroline Ellison tweeted that her firm would buy all of Binance’s FTT at $22. If the solvency of the Alameda / FTX empire hinged on FTT, then maintaining its price was likely the number one priority.

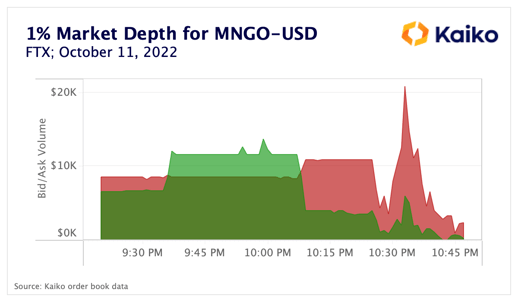

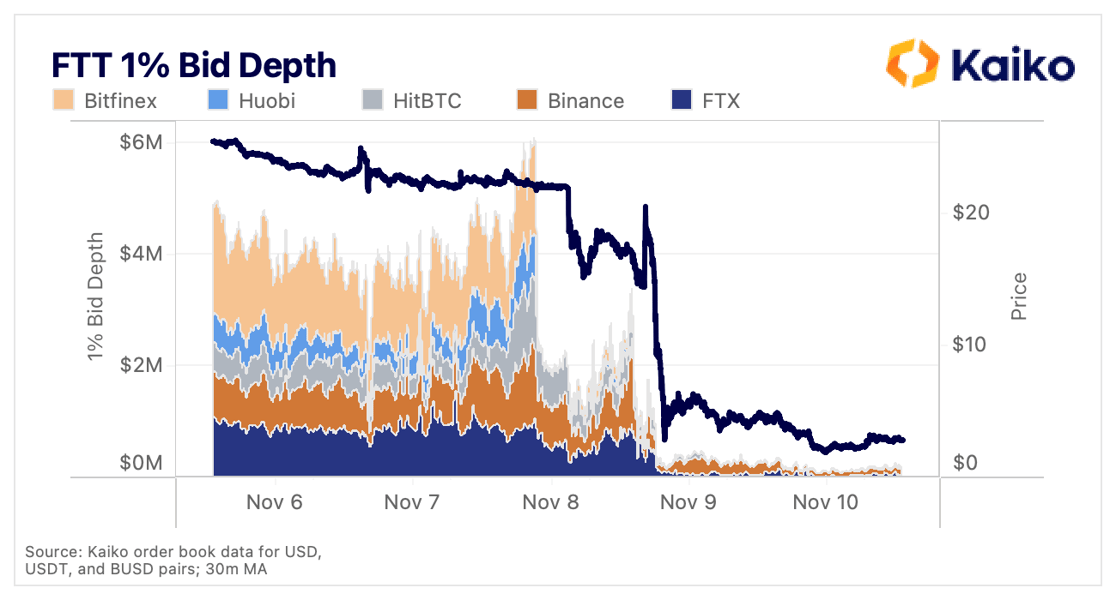

It is unclear whether these OTC discussions progressed, but at 9:15pm UTC on November 7, FTT liquidity was quickly pulled from order books: Bitfinex's 1% bid depth dropped from nearly $2mn to under $250, while Huobi's fell from $1.5mn to just under $3k in a matter of minutes. Depth on Binance and FTX was maintained over the same time interval, which suggests that it could have been a non-Alameda market maker that decided to exit the Bitfinex and Huobi markets, perhaps after getting wind that OTC deal talks between Binance and FTX had broken down.

It is likely that Alameda accounted for the vast majority of market making activity for FTT, which explains why it took a few days for FTT’s price to collapse even though selling pressure had already started. On this note, there was a sharp increase in depth preceding the crash, suggesting a bid wall. But the sudden collapse in liquidity does pose questions as to why Alameda didn’t or couldn't do more to maintain bids for FTT if the future of the firm depended on maintaining its price.

Five hours after liquidity collapsed, FTT’s price crashed below $22. Liquidity appeared to be improving as FTT bounced around in the $15-17 range, but again vanished ahead of the announcement that FTX would be acquired by Binance. FTT’s price increased on the news but quickly crashed below $3. Since then, FTT's 1% bid depth across all markets is hovering around $200k, and it is unclear who is still making markets at this point.

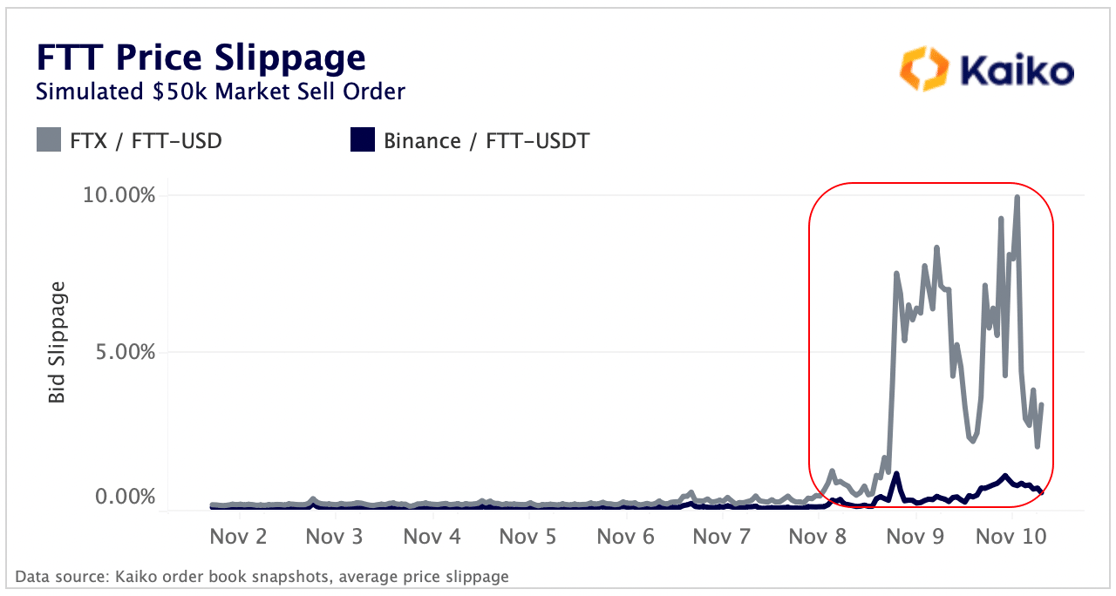

We can see just how quickly FTT liquidity collapsed by looking at price slippage. Using a simulated $50k market sell order, slippage on the two most liquid FTT pairs listed on Binance and FTX surged. By Wednesday, a $50k sell order on FTX would result in a whopping 8% price slippage as FTT’s price continued to plunge.

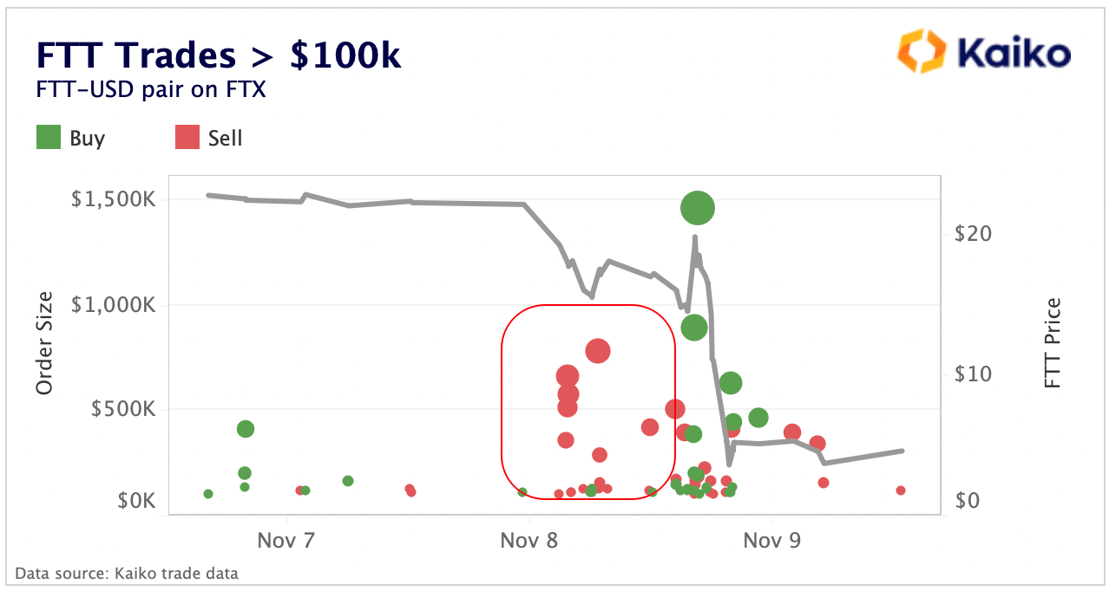

Huge market sell orders were rolling through as price was declining. Further revelations of Multicoin Capital’s exposure to FTT suggest industry participants were rapidly liquidating FTT as it slipped below $22. Typically traders will break up their orders into smaller chunks to avoid slippage, but in times of desperation, firms were taking whatever price they could get, with numerous orders larger than $100k.

As news of Binance’s potential acquisition spread, there was a brief spike in FTT, with a few very large market buy orders placed, possibly by Alameda in an attempt to push up the price. But markets quickly re-priced the seriousness of the move.

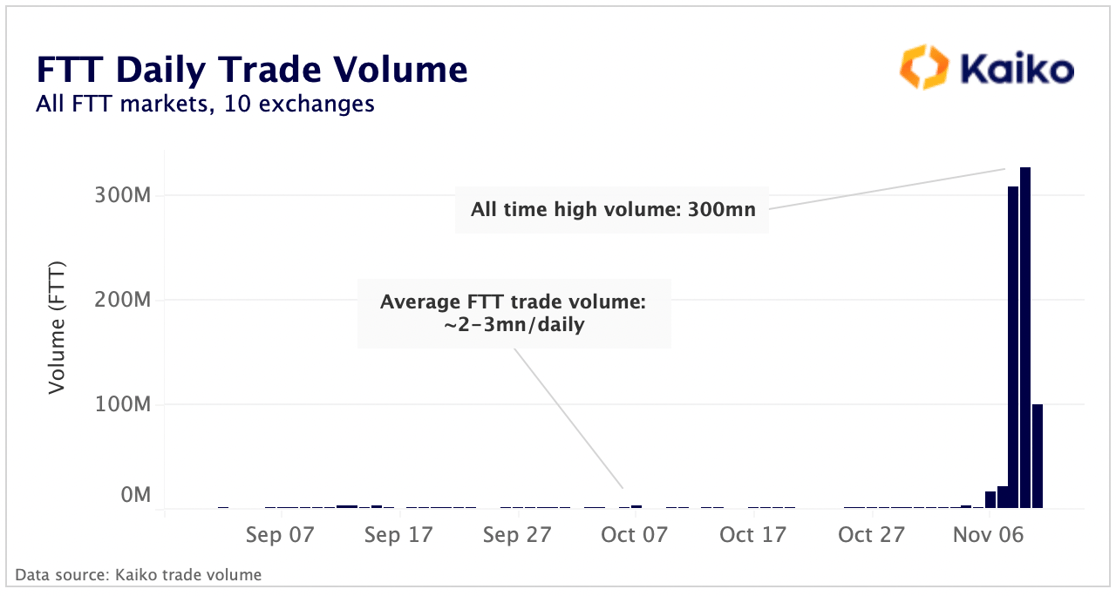

By the end of Tuesday, FTT trade volumes had soared to all time highs, with a whopping 300mn FTT swapped in a single day. On Wednesday, Binance issued a warning to all traders to halt all purchases and sales of FTT due to extreme risk, and volumes have since settled down.

FTT is now virtually worthless, the exchange token for an exchange with a multi-billion dollar hole in its book. The token is down nearly 90% in the past week, now trading at under $3, with a fully diluted valuation of just over $1bn.

Unfortunately, the damage from this market collapse spread far and wide due to the importance of FTX and the tangled web of investments that Alameda Research supported using the FTT token.

The cascading effects of the FTX/Alameda will take months to play out and are too numerous to cover in a newsletter. But let’s start with FTX itself and then expand into Alameda and broader impacts.

FTX in Purgatory

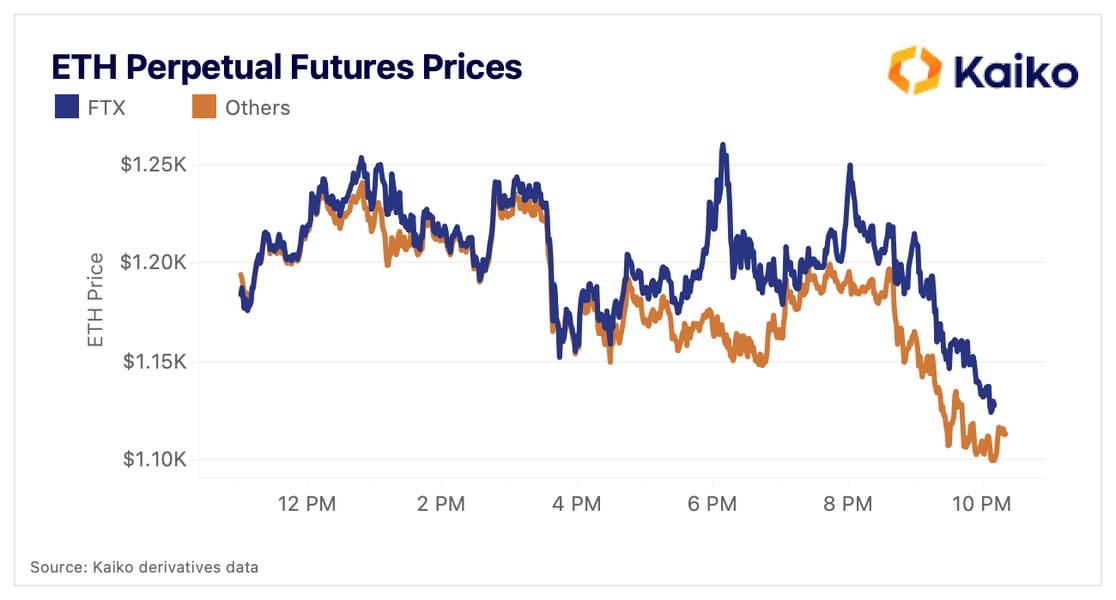

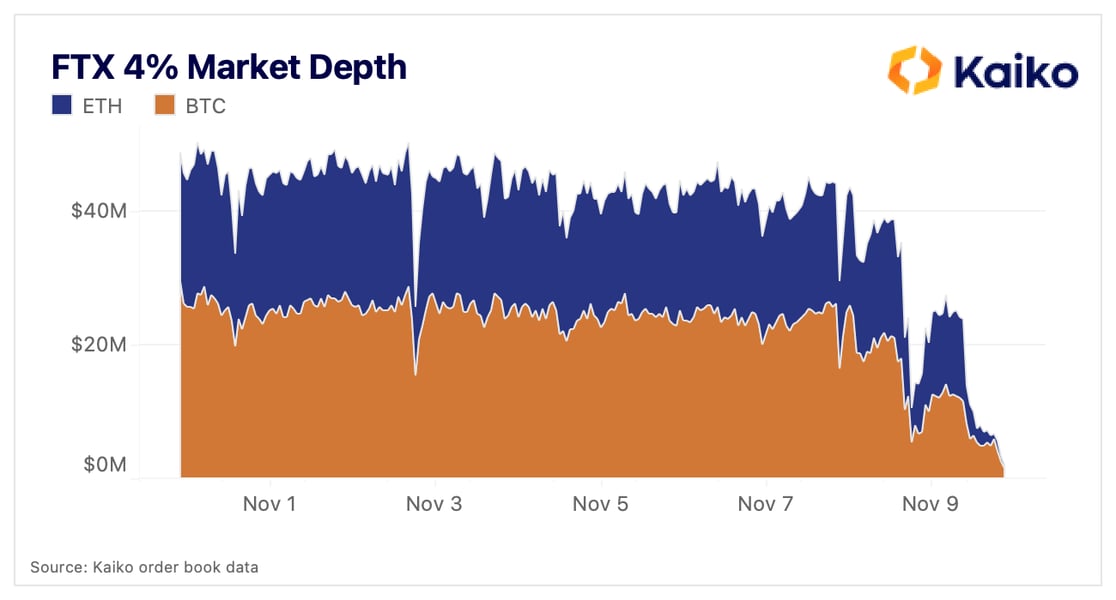

FTX is now purgatory, with all funds on the exchange effectively turned into Monopoly money or legal claims, depending on your time horizon. Market makers and retail users alike are trapped on the exchange, cut off from the rest of markets and left to develop its own biosphere. This is most simply illustrated by the price of ETH perpetual futures, which began to diverge on November 9.

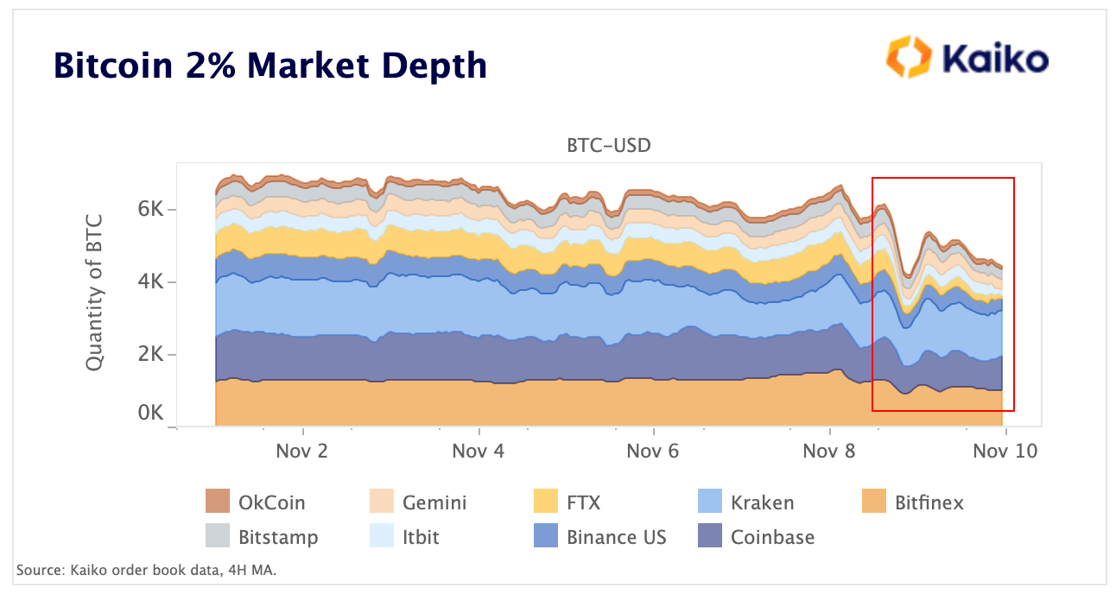

Liquidity on the exchange has understandably evaporated. 4% market depth for BTC is down from $25mn to under $2mn; ETH from $17mn to under $750k.

It’s reasonable to expect that FTX markets will continue to become stranger and less tied to reality the longer that users are trapped.

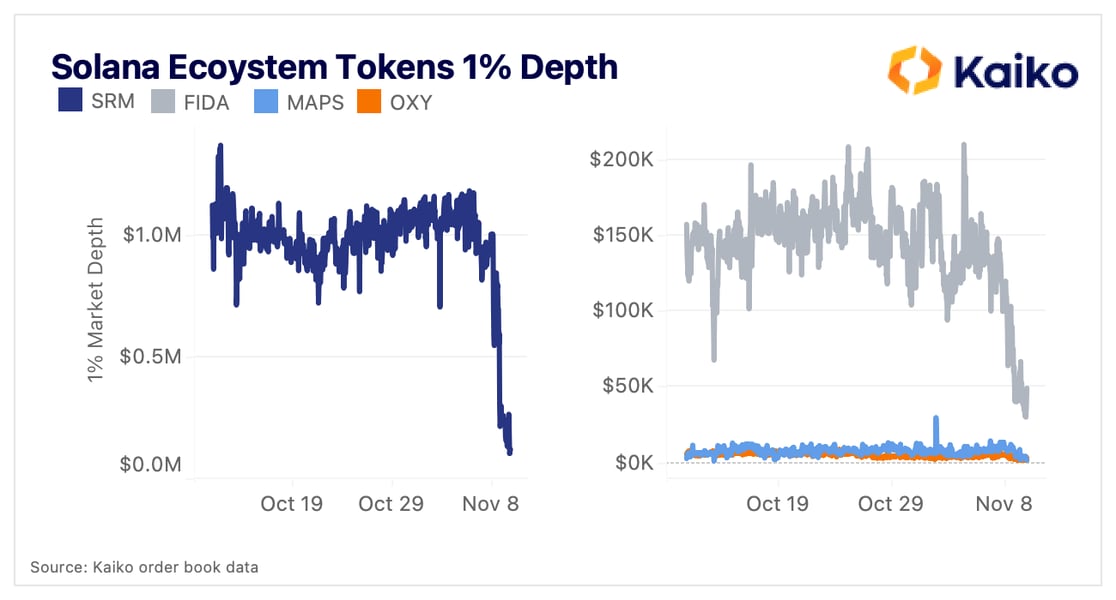

Moving on to Alameda, the company held a significant amount of SOL and Solana ecosystem tokens. FTX had also been an early backer of the project and SBF had frequently spoken highly of the network. SOL’s price has plummeted amidst the collapse, and open interest on FTX is trending towards 0. Open interest has surged on other exchanges, coupled with a funding rate that moved violently downward, suggesting heavy shorting.

Alameda had long been involved in the Solana ecosystem, and had developed a reputation for investing in projects with massive fully diluted valuations and small market caps, which allowed them to profit while early retail investors were crushed. Many of these tokens were already down over 90% from all-time highs (for OXY, all-time high was immediately after launch). However, Alameda still held these tokens, though they have since become too illiquid for the company to unload a significant amount without sending the tokens to 0.

While this is a bleak moment for Solana and its ecosystem, the network will be put to the test now that one of its most significant (and predatory) backers is no more. Ethereum and Bitcoin have undergone similar – and likely tougher – tests, and both were made stronger afterwards. Should Solana survive this test, it could be better for it.

The fallout has spread to Ethereum, too. People quickly realized that FTT was a major backing of MIM, a collateralized stablecoin. On-chain investigation revealed that much of this was Alameda’s position, and it would be liquidated when FTT reached $6. On this news, MIM’s peg started to shake, though the team quickly announced that it was working with Alameda to reduce the size of their loan. MIM then returned to its peg and has not seen strong outflows from its Curve pool. Total burns were only a bit more than mints over the past few days.

On the other hand, the Lido Staked Ether (stETH) Curve pool has seen massive outflows in the past three days, with over $600mn net removed from the pool. The stETH discount has also reappeared, and is currently at around 2%. The exact cause for this removal of liquidity and reemergence of the discount is not entirely clear, though some have speculated that Alameda has a sizable stETH position that will need to be liquidated.

This is just a sample of the myriad ways this collapse is shaking markets, both on centralized and decentralized exchanges. The true and complete fallout of SBF’s hubris will not be fully understood for months.

A Giant Gets Bigger

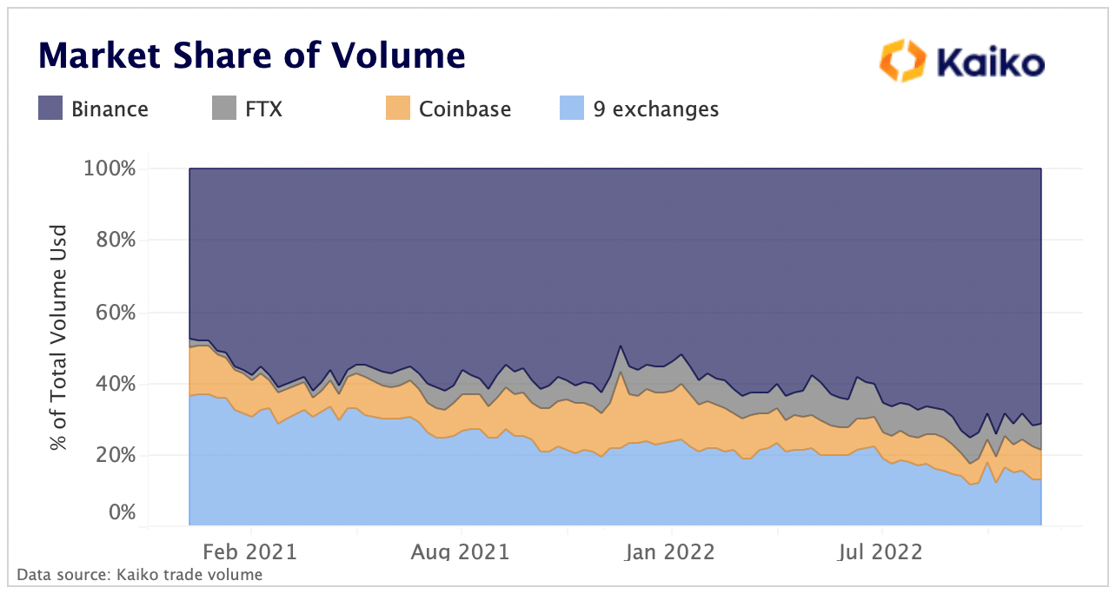

Although the acquisition seems all but dead, what would a Binance + FTX behemoth have actually looked like? Since the start of 2021, Binance’s market share of volume has climbed from 47% to 71% relative to 11 of the most liquid exchanges. Its total trade volume is larger than every other exchange combined.

While FTX’s volumes are just a fraction of Binance’s, the exchange had experienced considerable growth at the expense of others. Over the same time period, FTX’s market share climbed from just 2.5% to 7.5%, positioning the exchange as Binance’s most formidable competitor next to Coinbase.

(Included in the 9 other exchanges are FTX.US—.8%— and Binance.US—1.7%—thus total market share is even greater when factoring in these US entities)

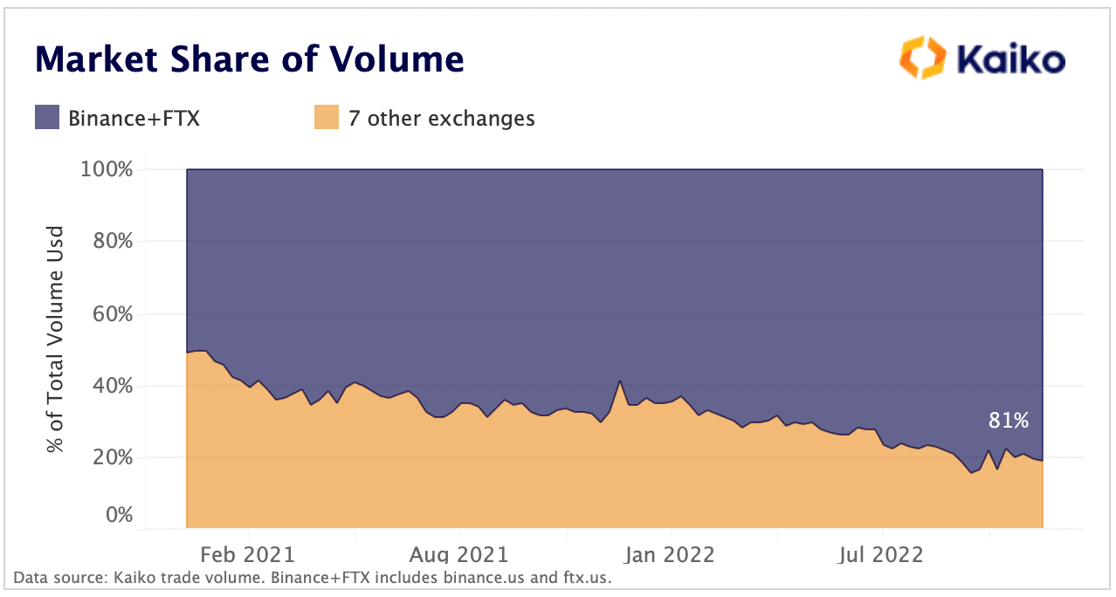

Let’s now take a look at market share post-acquisition, or in all likelihood, post-bankruptcy assuming that Binance claims whatever former traders used FTX.

Folding both Binance.US and FTX US into the new Binance behemoth, the exchange would claim upwards of 80% of total market share. In either scenario — acquisition or bankruptcy — Binance’s market share will almost certainly surge.

Liquidity Without Alameda

Alameda is one of the largest market makers in the cryptocurrency industry, along with Wintermute, B2C2, Genesis, and Cumberland. While it is impossible to know how much they contributed to overall market liquidity, their balance sheet makes clear that the firm was a systemically important market maker.

Alameda's insolvency could already be impacting liquidity. Over the past two days, the quantity of bitcoin on BTC-USD order books has fallen from around 6k across all markets to 4k.

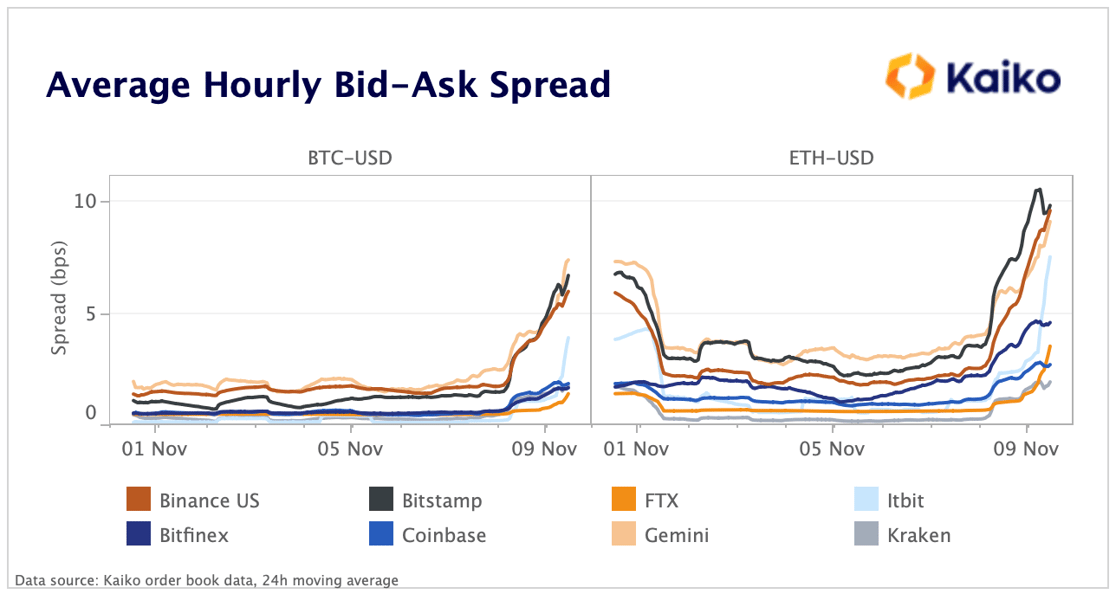

Spreads on every single exchange are at yearly-highs for both BTC and ETH, which suggests market makers across the board are skittish amid extreme volatility.

What Now?

Earlier this month, SBF came under immense flak for proposing regulation of DeFi protocol front-ends. Instead of DeFi, regulators should be squarely focused on centralized entities engaging in gross risk mismanagement at the expense of customers.

A three-prong approach to centralized entity regulation in crypto should involve the following:

Proof of reserves for exchanges and centralized lenders to prove that they can match deposits 1:1, at minimum.

Separation between trading/venture arms of companies and their exchange operations.

Disclosures of significant positions from those trading arms that could lead to market wide contagion à la Alameda’s exposure to FTT.

But even if all three were to be implemented, there are still two major problems: (1) proof of reserves would not show liabilities; and (2) regulatory arbitrage. There is no way to guarantee that institutions will act honestly, even if they are broadcasting assets on the blockchain. There will always be jurisdictions that allow companies to play fast and loose; this is the reason SBF is in the Bahamas while breaking bad news to investors. (As much as it pains people in crypto to admit, U.S. regulations did actually protect customers in this instance, as FTX US has continued to process withdrawals.)

These two problems are incredibly difficult to solve, but what doesn’t face either of these problems? DeFi. This collapse – caused by a tangled, opaque web rife with deception and greed – is the single greatest advertisement ever made for DeFi.

Questions will now naturally turn to Binance. How exposed is Binance to BNB and what would happen if it went to $0? Does Binance invest customer assets and can they match withdrawals on the exchange 1:1 if a similar bank run was to happen? Hopefully, Binance will do everything it can to build transparent, rock-solid financials to avert this type of bank run.

FTX’s collapse was a brutal blow to the industry, and we feel for all the retail users who were harmed. FTX's 7% market share will be replaced, but rebuilding lost trust will be the industry's toughest challenge yet. We are confident though that the industry will recover. Ultimately, crypto has time and time again proved itself resilient, thanks to the countless builders and innovators working to build a decentralized and transparent financial future.

We are pleased to announce the launch of our proprietary implied volatility smiles for BTC and ETH, a fundamental product for cryptocurrency options traders. Our quantitative analytics team constructed a transparent and robust methodology providing IV for any expiry and strike price. Learn more about the product here.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.

-3.png?upscale=true&width=1116&upscale=true&name=image%20(14)-3.png)

-2.png?upscale=true&width=1116&upscale=true&name=unnamed%20(1)-2.png)

.png?upscale=true&width=1116&upscale=true&name=unnamed%20(2).png)