Our latest Deep Dive explores the winners and losers of the FTX scandal as the contagion continues full steam ahead. While a lot of the winners and losers will only play out over the course of months or years, there are some important market trends in the immediate aftermath of the FTX collapse which may give us a good insight into what's to come down the road. Using a combination of Kaiko's CeFi and DeFi data, the Kaiko Research team identify some of the key trends to keep an eye on.

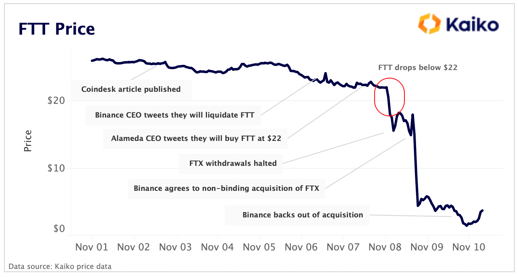

The aftershocks of the FTX fraud continue to ripple through crypto, with entities such as Genesis Trading and the FTX-owned exchange Liquid halting withdrawals over the last couple of days. It’s likely that it will take months or years to determine who the real winners and losers of the biggest scandal in crypto history will be, but there are some interesting market dynamics to be aware of in the immediate aftermath of the collapse of FTX. Using Kaiko’s CeFi and DeFi data, we have identified some important trends that give an indication as to who may stand to win and lose in the future.

DeFi

Winner: Decentralized Exchanges

Loser: DeFi Protocols Relying on Oracles

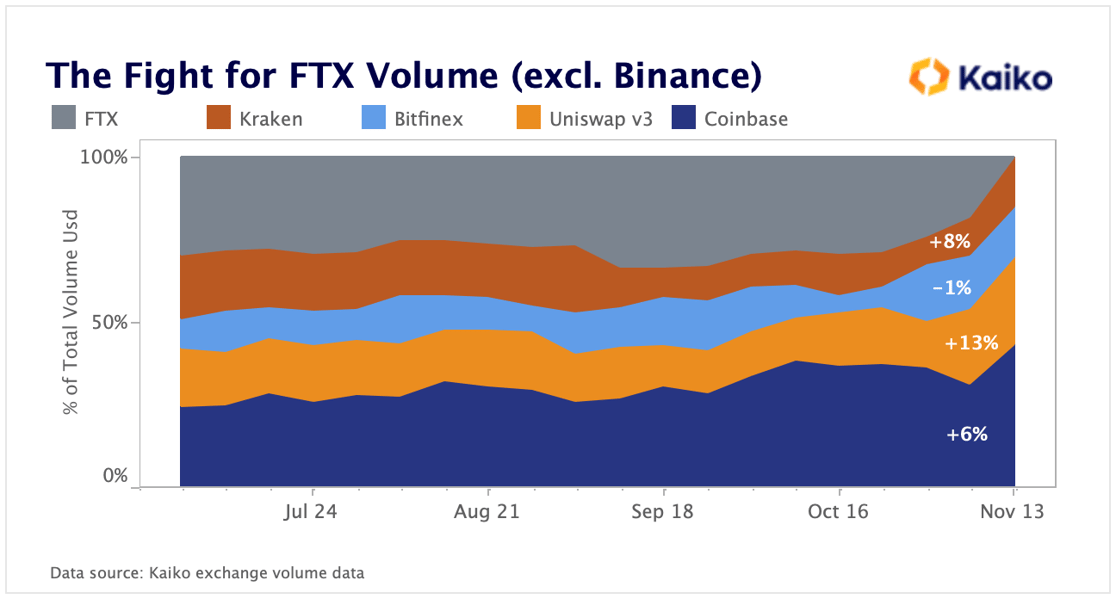

Decentralized exchanges were the immediate beneficiary of FTX’s collapse, as Uniswap V3’s volume surged past many of its centralized peers in the aftermath. Uniswap V3 rose the most in market share compared to its centralized competitors, the 3 other highest volume exchanges since the end of October, gaining 13% in share of volume in the fight for second place to Binance.

It remains to be seen whether this will be an enduring trend, but given the constant stream of bad news, it doesn’t appear that this collapse will leave industry participants’ minds any time soon.

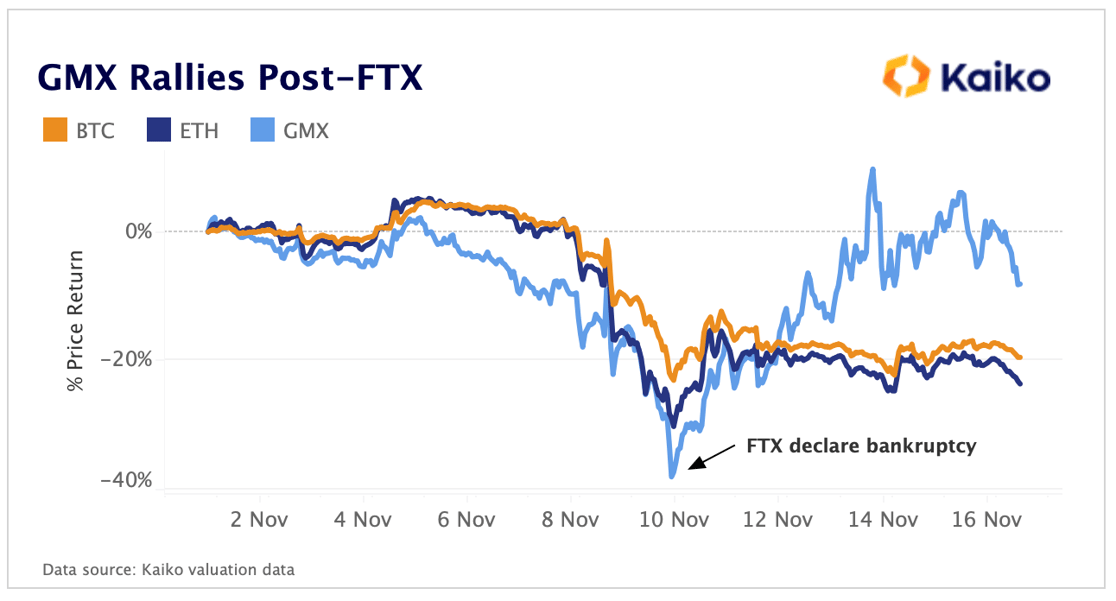

Additionally, GMX, the native token of the decentralized derivatives exchange, rallied over 40% and stands to benefit from decreased trust in centralized derivatives exchanges. As we reported last week, FTX had accounted for 14% of total BTC open interest and 28% of ETH open interest as of early November.

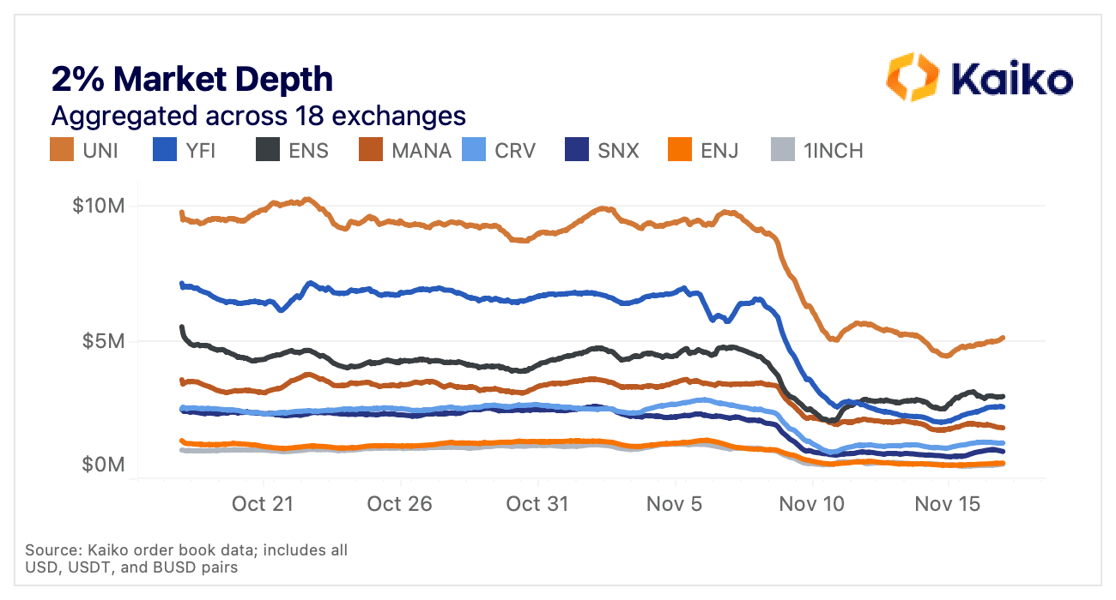

Despite the increase in DEX volume, many DeFi protocols still rely on oracles to supply price data to smart contracts. The vulnerabilities of these protocols had already been exposed recently, first on GMX, then on Mango Markets. Essentially, these protocols need price inputs, and these price inputs come from oracles, which come from data providers (like Kaiko), which come from a mix of centralized and decentralized exchanges. This normally functions well, but when a token is illiquid it can be relatively easy to change its price, which could be picked up by an oracle, triggering liquidations or other chaos.

Unfortunately, altcoins are not very liquid right now.

Aave is the flagbearer for DeFi lending and borrowing and it relies heavily on price oracles to automatically manage loans. To mitigate the aforementioned issues, it has paused borrowing of certain tokens, including BAL, BAT, CVX, DPI, REN, and ZRX. However, it still allows for borrowing of 1INCH, CRV, ENJ, ENS, MANA, SNX, UNI, and YFI.

2% market depth for all of these tokens has been cut in half, making them all significantly easier to manipulate and increasing the risk for any DeFi protocol offering lending, borrowing, or leverage on altcoins.

Kaiko’s market depth data aggregates bids and asks across all exchanges that offer these tokens, giving a comprehensive snapshot of liquidity. Learn more about this data type here.

Regulated Exchanges

Winner: U.S. Regulated Exchanges

Loser: Lightly Regulated Exchanges

This is likely the most unpredictable section here, and depends largely on how legislators and regulators react. It makes logical sense that participants, particularly institutions who have seen funds like Multicoin and Galois get trapped on FTX, would now strongly prefer to use exchanges that are regulated and/or licensed in jurisdictions like the U.S. But then again, it doesn’t make logical sense that FTX would lend customer funds to a trading firm that excelled only at losing money, or that SBF would continue to DM with journalists while he’s the subject of numerous investigations, so maybe logic isn’t the best guide.

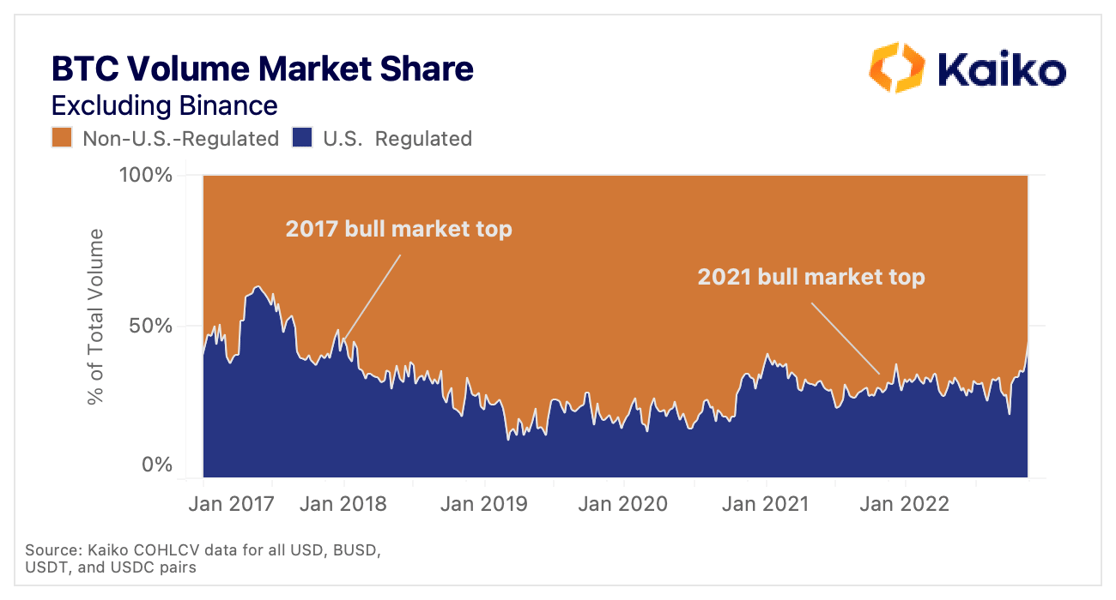

In any case, Coinbase’s long standing frustrations with U.S. federal and state regulators paid off, as CEO Brian Armstrong was able to point to Coinbase’s status as a public company incorporated in the U.S. with public audited financials showing that the exchange holds customer’s funds 1:1.

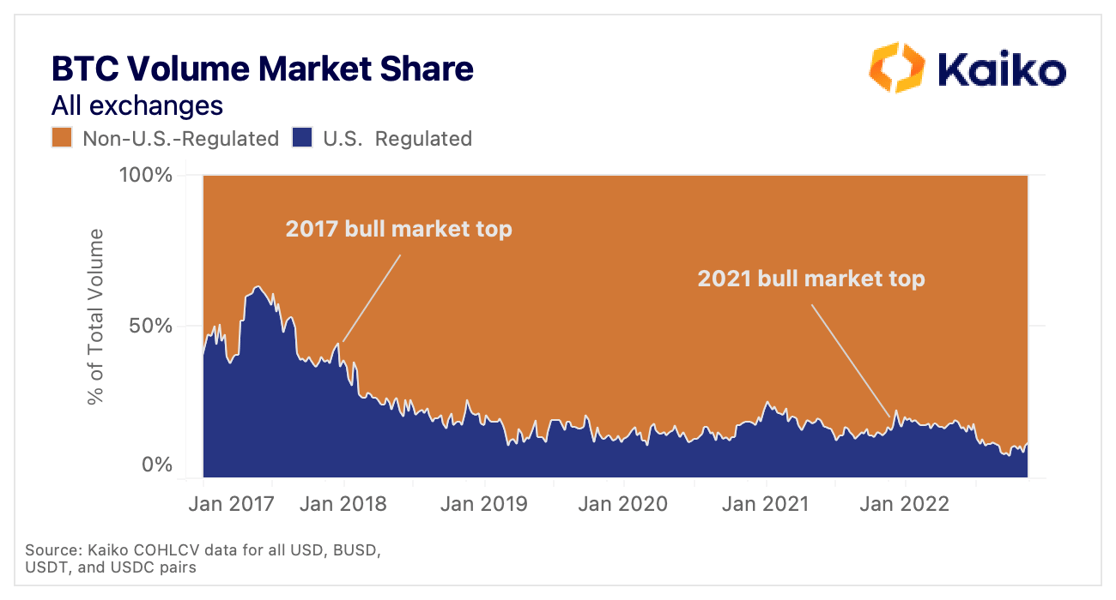

U.S. regulated exchanges lost significant market share after the 2017 bull run, though they surged in late 2020 and have remained flat since early 2021. This week, though, they reached 45%, a high not seen since December 2017. Whether this is indicative of a trend will only become clear in time.

Binance

Winner: Binance

Loser: Competition

Eagle-eyed readers may notice that the above chart doesn’t include Binance. This is for a simple reason: Binance is so much larger than other exchanges that it skews every chart. This is why our assessment of winner vs. loser in terms of regulation gets complicated. Here’s the same chart with Binance included:

This tells an entirely different story, one in which non-U.S.-regulated exchanges are dominant, and increasingly dominant at that. The Kaiko Research team has long struggled with Binance warping axes and distorting charts, especially since Binance removed trading fees for BTC pairs, and this trend seems likely to continue and strengthen. Binance has projected an image of strength and security following the demise of its fastest growing competitor, including setting up an industry recovery fund and publishing proof of reserves.

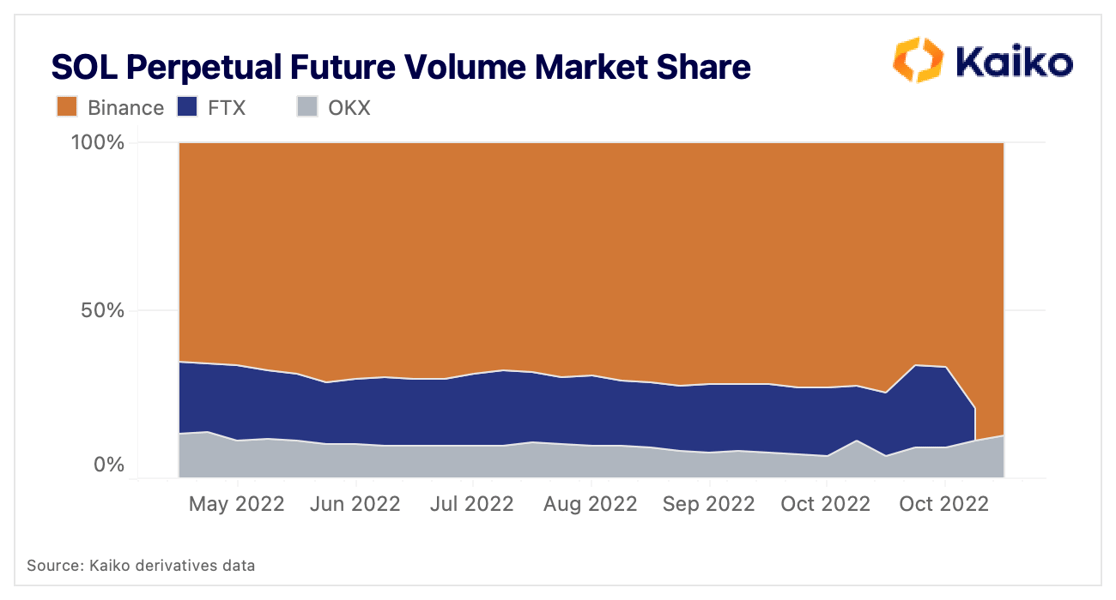

The loss of FTX will be most felt in the perpetual futures market (particularly altcoins), where it was most competitive with Binance. Below is the market share of SOL perpetual futures volume; FTX’s market share has been almost entirely absorbed by Binance.

This should concern everyone in the industry, not because it is Binance specifically, but because any exchange having such immense influence seems to fly in the face of crypto’s ethos. Binance has long been opaque in its operations (for example, it is impossible to nail down an actual headquarters), though its recent moves to increase transparency are an encouraging, if not totally placating, sign.

Liquidity

Winner: None

Loser: Liquidity on CEXs and DEXs

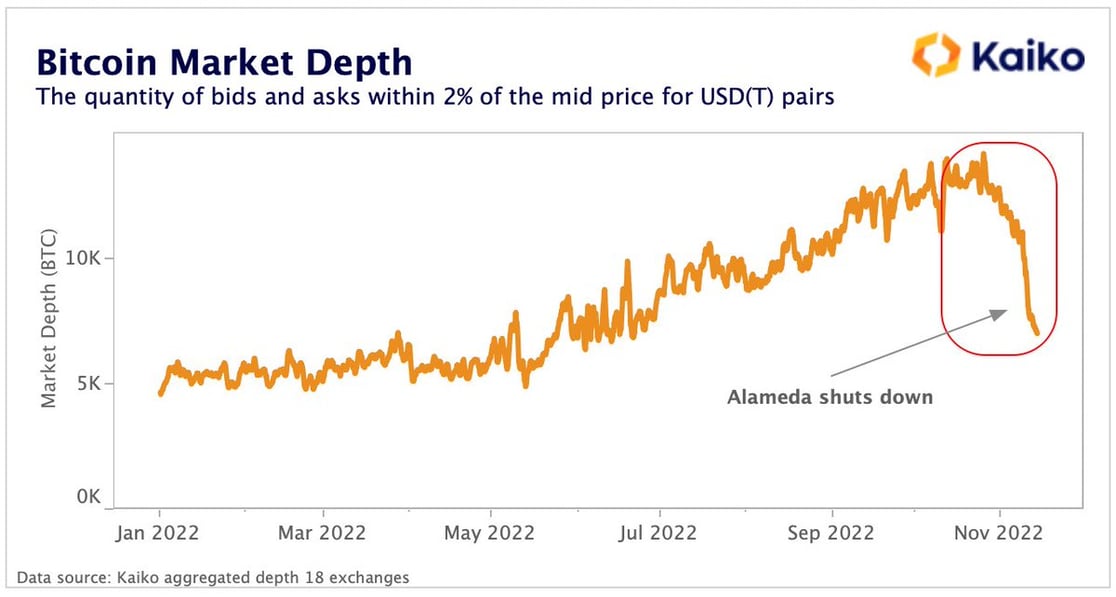

Liquidity has been significantly impacted in the last week and we are seeing an “Alameda gap” forming across markets as one of the biggest market makers shuts down operations (other market makers were impacted by FTX’s collapse, contributing to the gap). Liquidity typically drops during times of volatility as market makers pull bids/asks from order books to manage risk and avoid toxic flow. But the drop in liquidity we have observed over the past week is far larger than any other previous market drawdown, which suggests the Alameda Gap in liquidity could be here to stay, at least in the short term.

For more on on the impact on CEX liquidity you can check out this week's Data Debrief

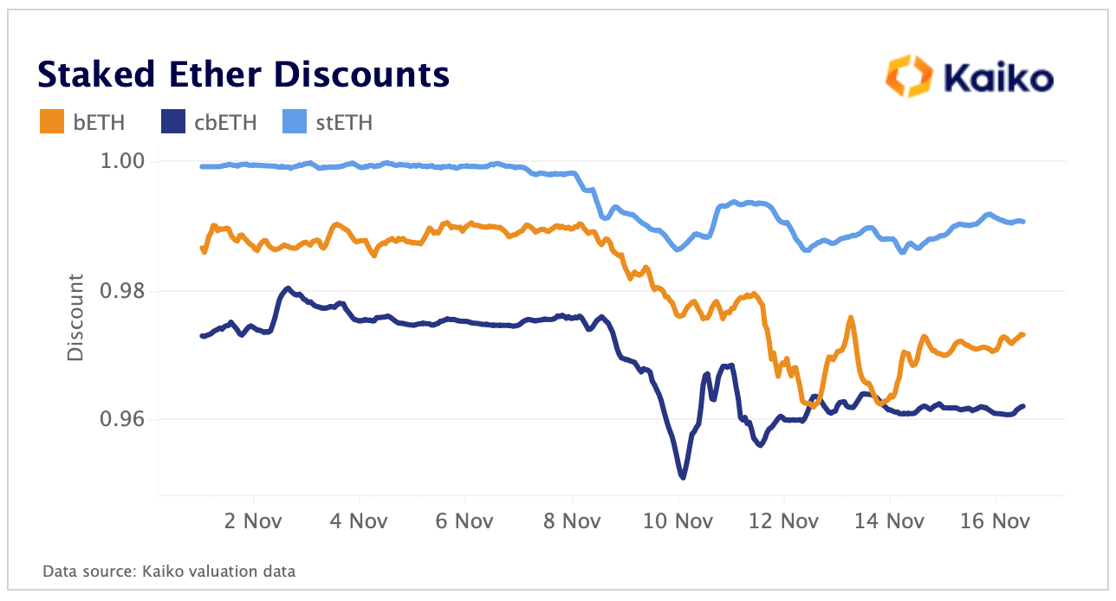

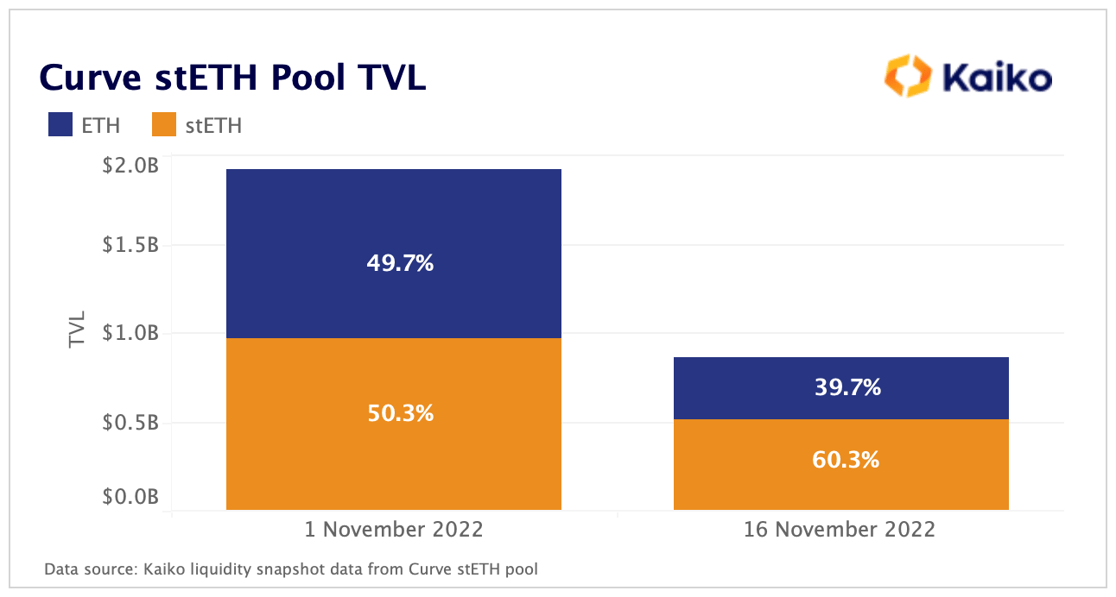

Another victim of worsening liquidity has been liquid staking products. Custody risk is at the forefront of every crypto investor’s mind right now and staking products such as staked ether are no exception. Trusting someone with your crypto seems like a dangerous move in times where contagion spreads like wildfire. Coinbase and Binance offer their own staked ether products, and the discounts for both deepened by over 2% after FTX’s collapse. Lido’s stETH wasn’t spared either despite being significantly more decentralized, likely due to investors placing a premium on liquidity, with ETH being more liquid than stETH.

The preference for ETH over stETH was evident in the makeup of the Curve pool. Using Kaiko’s DeFi data, we can see the split between ETH and stETH moved from 50:50 at the start of November to 60:40 yesterday in favor of stETH as more ETH was pulled out of the pool. TVL fell significantly, dropping by over $1bn in a matter of a couple of weeks, proving liquidity issues were not exclusive to centralized exchanges.

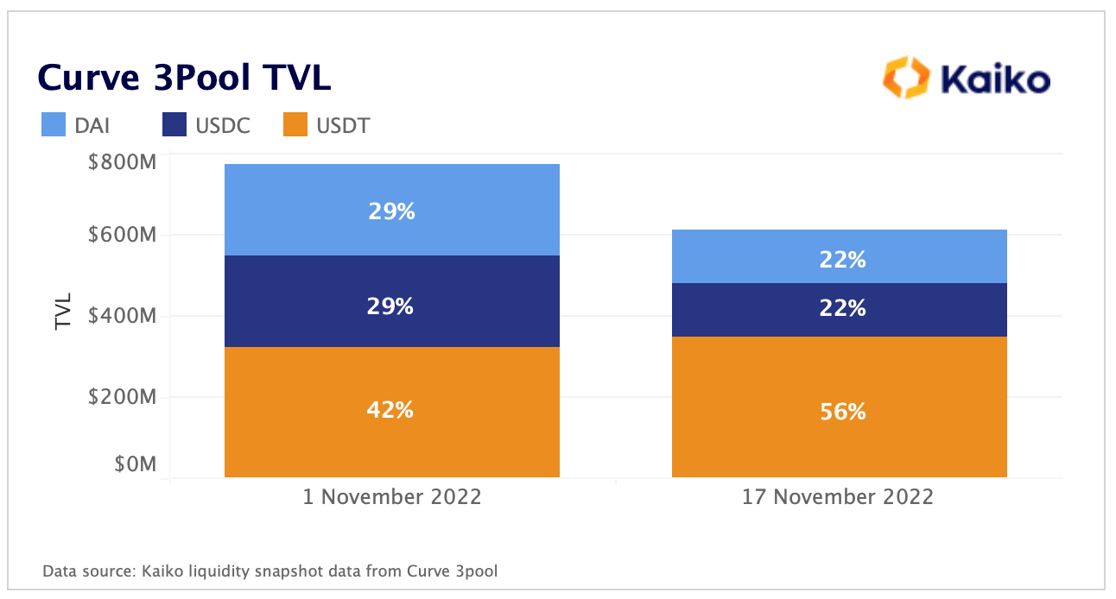

Decreasing liquidity is a trend across Curve pools, with the 3pool TVL falling nearly $200mn since the start of November. The breakdown of the pool was arguably more interesting however, as rumors circulated that Alameda was trying to depeg Tether in a last ditch attempt to earn some much needed cash. Their alleged attempts were unsuccessful, as Tether has returned to its peg, but its share of the 3pool surged to 56%, up 14% from the start of November. While Alameda may have contributed to the imbalance, the larger trend is investors prioritizing transparency after the FTX scandal. Tether are infamously opaque with their reserves compared to DAI’s on-chain transparency and USDC’s comparatively thorough audits.

Derivatives

Winner: Leverage flushed out

Loser: Delayed institutional adoption

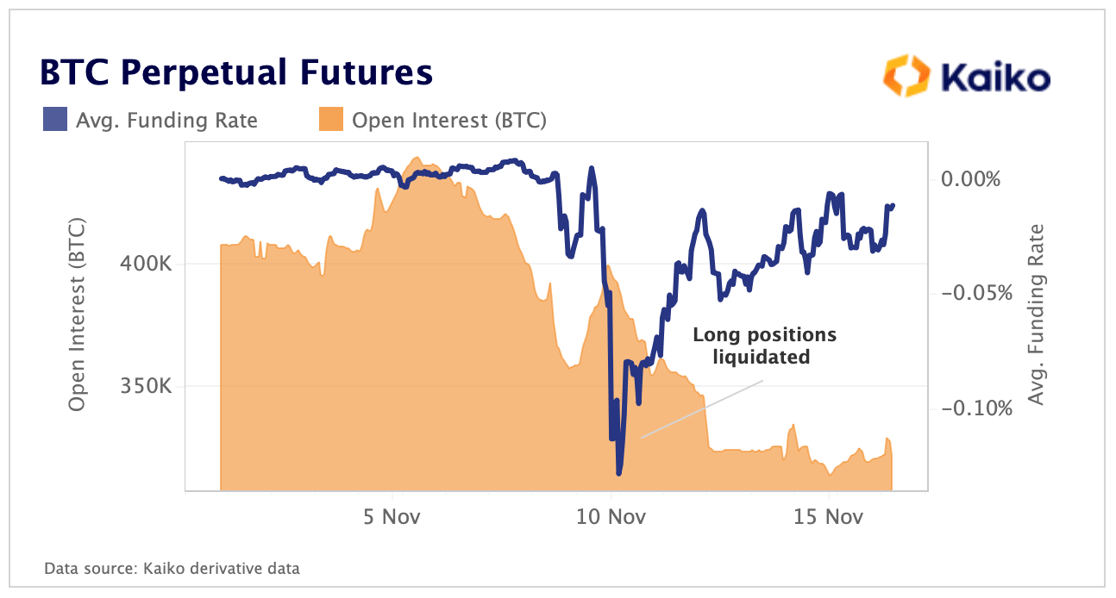

Open interest was on a constant rise this year, leading to perpetual futures volumes rising from 4x to 7x spot volumes this year. Among the increased perpetual futures volumes were some speculative positions on certain tokens, the most ambitious being bets against Tether, which began trading at a discount for 60+ days after the Terra collapse, as investors took to perpetuals to speculate and perhaps depeg the stablecoin. A lot of speculative, leveraged positions were taken up this year as open interest in native units for BTC and ETH hit all time highs.

The latest FTX scandal has been a black eye for crypto’s reputation and the fallout from SBF’s antics will be felt for years. This is particularly true for crypto derivatives markets where institutions are the dominant player. The collapse of FTX has opened the eyes of many institutions who were active in futures markets but used a centralized exchange to route their trades and custody their balances. Even crypto-native hedge funds such as Ikigai revealed they were impacted by the FTX scandal. Now any institutions looking to enter the space using derivatives will have to think twice before trusting a centralized exchange with their funds. Custody risk now warrants serious consideration in the risk management process, particularly for unregulated exchanges. In the short-term this will inevitably lead to less futures trades being placed.

The speculative positions have been flushed out of the market and more conservative traders will be slow to trust centralized exchanges again, meaning we can expect far less leverage in the system as a whole - arguably a good thing if we can reset the foundation to rebuild on minus the excessive leverage. Funding rates dipped sharply negative while open interest fell over 100k BTC, meaning the majority of liquidated positions were long.

Lower derivative market activity should give spot markets a greater role in price discovery. The flipside of this is that centralized exchanges will likely lose derivative volume share to decentralized exchanges offering the same products minus the centralized custody risk.

Conclusion

Once crypto survives this scandal, the overall winner will be a healthier foundation on which we can build upon, minus the excess leverage and fraudulent actors. Cold storage wallets and decentralized exchanges should be the big winners - I say should because history has shown us investors have short memories, repeating the same mistakes over and over. Hopefully this fiasco serves as a learning exercise for the entire ecosystem, an over-reliance on centralized entities is just recreating the traditional financial system and offers nothing unique.

We need to prioritize decentralization and regulation because too many times so far in this space if there’s any opportunity to do evil, evil will be done. The beauty of DeFi is code can’t be evil, all the decentralized platforms such as Uniswap or Aave have functioned perfectly in what is now two contagion crises in six months. Regulation is necessary as these large exchanges do serve as useful onboards for the masses, we just need to endure the masses are protected from scams like this from happening again. Only once we learn these lessons can we start thinking about reinventing a financial system.

We are pleased to announce the launch of our proprietary implied volatility smiles for BTC and ETH, a fundamental product for cryptocurrency options traders. Our quantitative analytics team constructed a transparent and robust methodology providing IV for any expiry and strike price. Learn more about the product here.

This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.