Price Movements: USDT continues to trade at a discount to the U.S. Dollar. as outflows surge to $10bn.

Market Liquidity: BTC and ETH market depth have diverged following a spike in ETH liquidity.

Derivatives: BTC funding rates finally broke their neutral trend and dipped negative amid ongoing bearish sentiment.

Macro Trends: Nasdaq's volatility is at its highest level since March 2020.

Special Feature: Introduction to DEX liquidity events and snapshots.

Trend of the Week

Tether outflows surge in aftermath of Terra collapse.

The loss of confidence following the collapse of the Terra ecosystem continued to spur volatility in the rest of the stablecoin market. Since the start of May, Tether's circulating supply has dropped by $10 billion as the stablecoin continues to trade at a discount to the U.S. Dollar after dropping to as low as $.94 on May 12th. Tether's redemption mechanism is reserved for verified users and only executed above a $100k threshold, which leaves market sell orders as the easiest route for smaller traders to cash out, adding to the selling pressure throughout the week. By contrast the second and third largest stablecoins—Circle’s USDC and Binance USD—saw their market capitalisations increase by $4bn and $900mn respectively. All stablecoin prices (charted above) have remained more volatile than average since the start of May.

We can look at buy/sell ratios to understand how traders are reacting to uncertainty in stablecoin markets.

On Bitfinex (the exchange that shares a parent company with Tether), the sell ratio for Tether has soared over the past two weeks, suggesting heavy outflows. For USDC, sell volume surged in the immediate aftermath of UST's collapse, but over the past week buys now far outweigh sells, which reflects current supply metrics. The most interesting buy/sell ratio lies in the USDC-USDT pair, which suggests that traders are profiting off of USDT's persistent discount, which has created a USDC premium of 1.0011 at press.

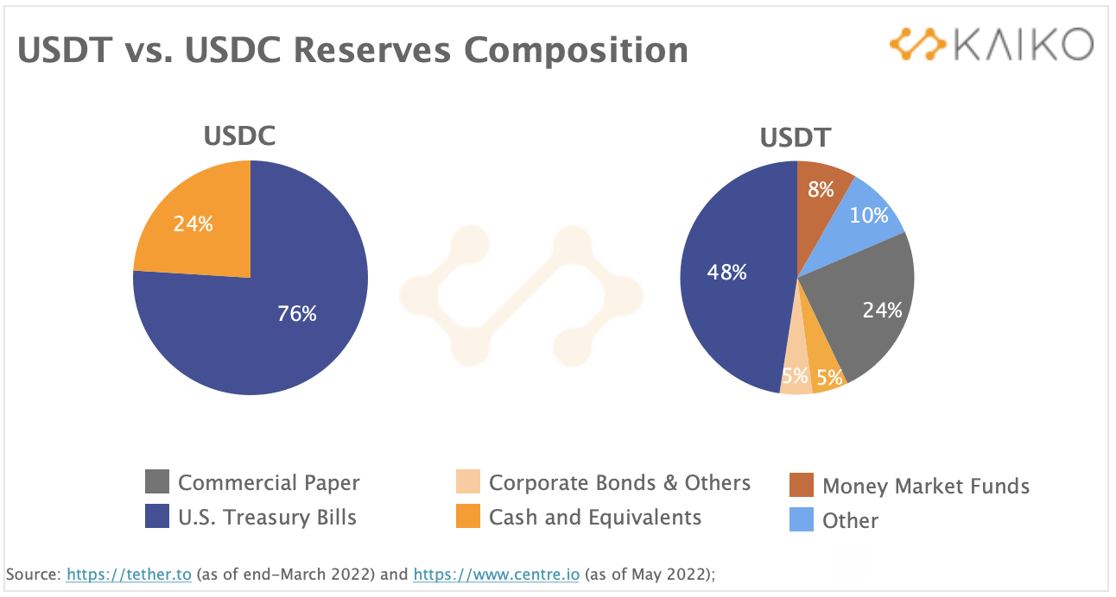

In an attempt to re-assure investors amid strong USDT outflows, Tether’s parent company published the stablecoin’s quarterly reserves, which shows a decline in the share of commercial paper it holds.

Typically, commercial papers, which are short-term unsecured debt issued by corporations, are seen as less liquid and riskier than cash. They now account for 24% of Tether’s reserves, down from over 30% at the end-2021. However, the share of money market funds increased 8%. From a risk and liquidity standpoint, money market funds are very similar to commercial papers. Overall, USDC’s reserves are much more concentrated with 77% held in U.S. Treasury Bills and 22% in cash.

Price Movements

Markets stabilize following extreme volatility.

Market sentiment has stabilized considerably over the past week, with both BTC and ETH trading above major levels of support as of Monday morning. Equities markets, on the other hand, have entered bear market territory, with the S&P 500 suffering its largest single day drop since the start of the pandemic. Despite an increasingly pessimistic global growth outlook, the crypto industry continues moving forward. Last week, FTX.US announced a new stock trading feature, Robinhood launched a DeFi wallet, and mining activity in China showed signs of resurgence despite a ban.

ETH to BTC ratio suggests falling risk appetite.

The Ethereum-to-Bitcoin price ratio has declined sharply in May, suggesting deteriorating risk appetite among crypto investors following Terra’s UST collapse. The ratio can be used as an indicator of Bitcoin’s dominance relative to altcoin markets and has historically served as a gauge for investor sentiment. When it increases, it suggests investors are rotating funds into Ethereum and altcoin markets, and vice versa. After rising in March on the back of a broad improvement in global risk sentiment, the ratio is currently nearing yearly lows.

Special Feature: Intro to DEX Liquidity

Last week, Kaiko launched DEX liquidity pool data, which is the first data feed in the industry that provides tick-level mint/burn events and pool snapshots for the largest decentralized exchanges. Our DEX Data Feed now encompasses both swaps and liquidity events, providing block-by-block historical and live coverage for Uniswap, Sushiswap, Curve, Balancer, and 1Inch.

Liquidity Events

Liquidity events refer to all information on the addition or removal of tokens to/from a liquidity pool. When a user deposits tokens into a liquidity pool, they receive liquidity pool tokens that represent their pool share. Thus this process is referred to as a “mint”, as the user is minting a liquidity pool token by adding tokens to a pool. In the reverse, a user will “burn” their liquidity pool token and receive the underlying tokens in return, plus any transaction fees that they accrued. Kaiko's liquidity events data comprises every individual "mint" and "burn" transaction that happens on a DEX, enabling DeFi investors to analyze how liquidity evolves for a pool over time. We can observe that for Sushiswap's USDC-WETH pair, liquidity events dropped off sharply since the start of the year.

Liquidity Snapshots

Liquidity pool snapshots provide a bird’s eye view of liquidity pools, much in the way order book snapshots provide context to tick-level order book events. Kaiko takes snapshots of liquidity pools at each block (generally every 12-14 seconds). This enables us to analyze the token-level composition of each liquidity pool and calculate measures like "total value locked" by applying a USD conversion to the value of tokens. Look out for more analysis of DEX liquidity from the Kaiko Research team and reach out to us if you are interested in testing the data!

Kaiko Market Reports

Data-driven commentary on April's most significant market events

Curve trading volume reaches all time highs as $CRV token underperforms.

Curve is a decentralized exchange platform offering liquidity pools designed for extremely efficient stablecoin trading. Last week we saw stablecoin trading volumes on Curve reach all time highs as UST collapsed and investors rotated funds into "safer" stablecoins. In the aftermath of UST's collapse, DAI trading volumes on Curve reached all time highs as it quickly regained its spot as the largest decentralized stablecoin, while USDC saw a similar increase in volumes. Despite the surge in activity, Curve's native $CRV token dipped to its lowest price levels since January 2021.

Bitcoin and Ethereum market depth diverges.

Bitcoin and Ethereum market depth expressed in native units moved in the opposite direction during the recent period of market volatility. The trend suggests that market makers provided liquidity asymmetrically following Terra’s collapse. Above we chart the 2% bid and ask depth for BTC-USD and ETH-USD pairs aggregated on nine major centralized exchanges expressed in both U.S. Dollars and native units. We observe that the USD-denominated market depth for both assets followed a similar trend as spot prices remain highly correlated. However, while the price of Ethereum plummeted faster than Bitcoin’s since the start of May, the 2% ETH market depth expressed in native units has increased by nearly 20% from 35k ETH to over 42k ETH. By contrast, Bitcoin’s market depth fell from 3.8k BTC to 3.5k BTC this month as liquidity providers remained cautious amid a surge in volatility and souring risk sentiment.

The spike in Ethereum liquidity on centralized exchanges is also due to a decline in staking demand on Defi applications, following Terra’s implosion. The total value locked on Defi protocols plummeted by 45% since the start of the month to around $111b, suggesting strong capital outflows from the space. Overall, Bitcoin remains more liquid than Ethereum. However, since the start of the year, Ethereum market depth expressed in native units has risen at a faster pace than Bitcoin's and remained more resilient to short term price movements.

Spreads surge on Tether markets following Terra's collapse.

BTC-USDT markets saw a stronger increase in spreads than USD-denominated pairs following Terra’s UST collapse and USDT’s de-pegging on May 12. This is in line with on-chain findings which suggests that most of the Luna Foundation Guard’s (LFG) $3B worth of Bitcoin reserves - which were deployed in defense of Terra’s UST peg - were executed against USDT. The bid-ask spread is a measure of the cost to trade and is a proxy of overall market liquidity. Typically, higher spreads are associated with deteriorating liquidity and market stress.

The chart above shows BTC-USD and BTC-USDT bid-ask spreads on the major markets for both pairs. We observe that on Bitfinex, BTC-USD spreads rose from .3 bps to 2.3 bps between May 8-12 which is significantly less than the nearly nine-fold surge in BTC-USDT spreads over the same period. BTC-USDT spreads on FTX also rose six-fold exceeding 9bps on May 12. By contrast liquidity on the largest USDT market, Binance remained relatively resilient after the exchange saw its BTC-USDT market depth surge to an all-time high starting May 7, mostly on the bid side.

Derivatives

Funding rates break neutral trend and dip negative.

So far this year we have seen a regime of neutral or even slightly positive funding rates across exchanges as rates quite closely mirrored BTC price action. However, last week we finally observed a sharp move away from this trend as funding rates for BTC dipped sharply negative. Funding rates are a useful gauge of sentiment amongst institutions who make up the vast majority of investors in futures markets. That sentiment has been hard to determine so far this year due to the neutral rates, but last week was the first indication in the markets that institutions are becoming increasingly more bearish. However, that being said, as of this morning funding rates moved positive again and back towards the range we’ve been accustomed to this year, so perhaps the fear in futures markets was short lived.

Macro Trends

Nasdaq volatility reaches highest level since March 2020.

Worries about global growth have hit risk assets hard this year, and crypto has been no exception. However, investors that are wary of the volatile nature of crypto have likely been taken by surprise at Nasdaq's volatility this past month, which is at its highest level since March 2020. The Nasdaq and S&P 500 extended their losing streak to 7 consecutive weeks last week, as big U.S retailers such as Walmart and Target warned of companies scrambling to save their customer base in the face of rising prices. Bitcoin and Ethereum volatility also reached yearly highs as contagion fears hit the market after the Terra collapse.

Kaiko's research newsletter is written by Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA with help from the Kaiko team. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.