Welcome to Deep Dive! Last night, Silvergate decided to voluntarily liquidate, leaving the crypto industry scrambling for banking alternatives. Today, we explore the implications of Silvergate's collapse on cryptocurrency markets and the viability of alternative fiat on-ramps for institutions and exchanges.

The research team is thrilled to launch our monthly analyst call: The Current. We'll discuss the most significant crypto market trends with our signature data-driven analysis (using plenty of charts). Submit a question in advance here and register below!

Crypto optimists have said for the last few months that the worst is behind us. Just in the last year we’ve seen the collapse of crypto hedge funds, lenders and exchanges. They say the bad actors have been removed from the space and there’s only good news from here. Well, bad actors or not, there are still plenty of hurdles the industry needs to overcome to escape this bear market and the collapse of Silvergate is the latest banana skin the industry faces.

Last night, Silvergate, crypto’s most amenable bank, made the decision to wind down and voluntarily liquidate. The decision comes a week after they delayed filing their 10k and shut down the SEN network, a crucial piece of infrastructure enabling instant payments between crypto firms. Silvergate fell victim to a classic bank run, taking mark to market losses on their bond investments to cover clients that were pulling their deposits: over $8bn of withdrawals since the collapse of FTX.

As has been the case with every black swan event crypto faces, the question now turns to how the industry will adapt. Will crypto become more reliant on stablecoins if USD payment rails are too burdensome? Will Europe and other regions benefit from greater regulatory clarity and a more attractive banking environment? In this article, I’ll take a look at the implications of the Silvergate meltdown, and discuss the viability of these potential alternatives.

The Fall of Fiat in Crypto

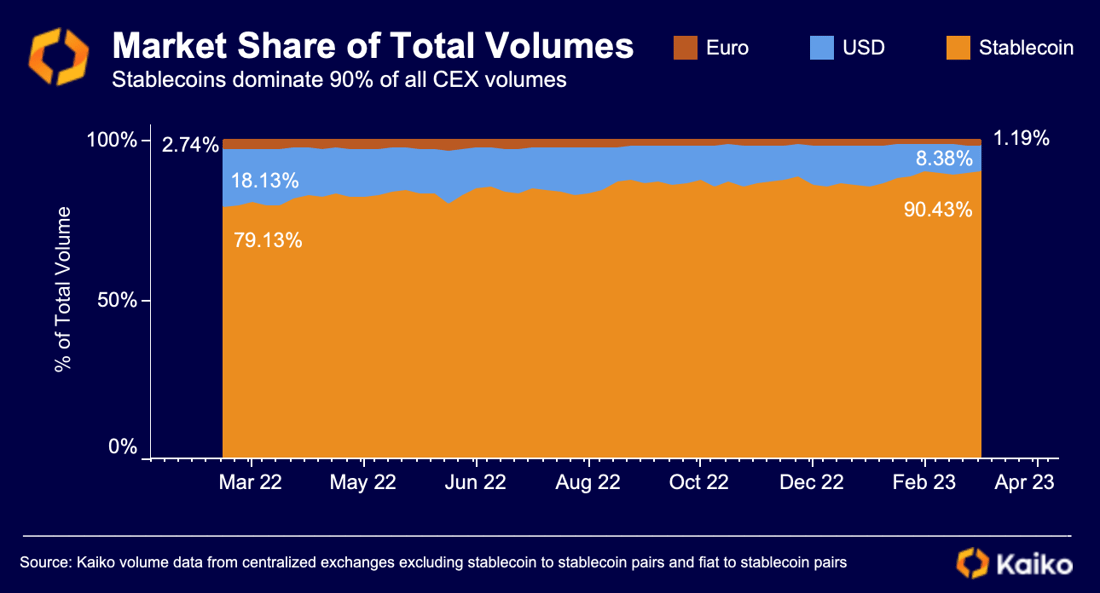

When it comes to trading, the good news for investors is that the crypto industry has become increasingly less reliant on fiat currencies over the past few years. In fact, the percentage market share of all volumes on centralized exchanges for stablecoins just hit an all-time high following the Silvergate troubles last week, as investors continued to prefer stablecoins to traditional fiat. In the last year alone, stablecoins have risen from 79% of volumes to over 90%, commanding the vast majority of volumes on exchanges.

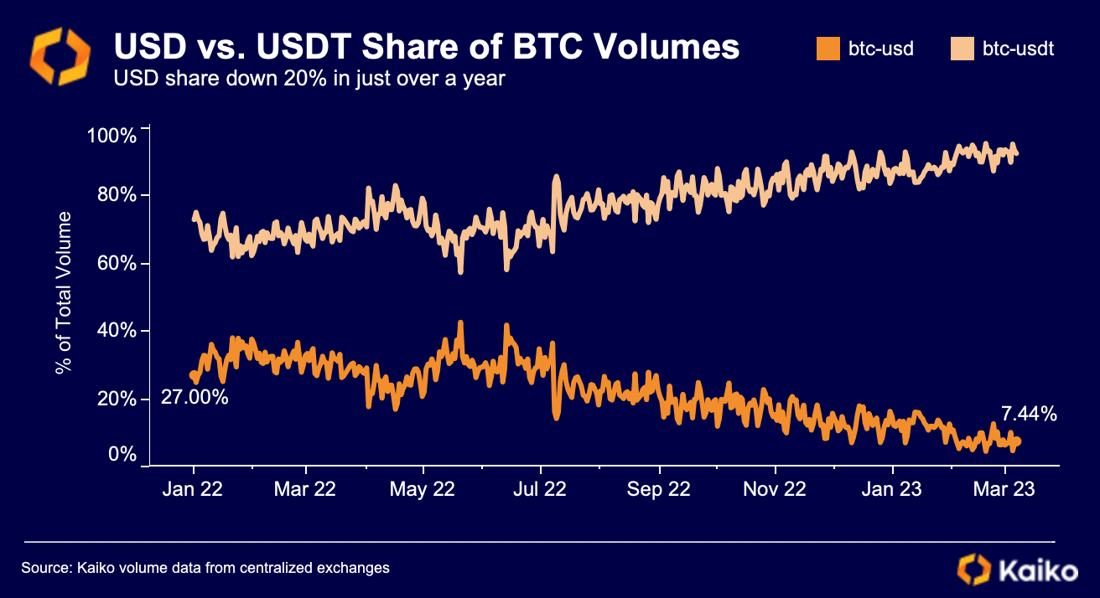

USD pairs in particular have been hardest hit, falling over 10% in share of volumes. Looking at Bitcoin markets, we see that USDT has nearly completely eroded the dominance of USD, also reaching all time-highs last week of 93% of volumes versus the Dollar.

USD pairs fading into irrelevance dampens the impact of the Silvergate news from a trading point of view. However, the brunt of a banking cut off will be felt by the institutions in crypto, who will begin a tough process of looking for suitable alternatives.

Calling it a bank run is generous to Silvergate, who clearly suffered from an over-concentration in crypto deposits relative to non-crypto deposits, while investing in too high duration bonds in an effort to earn some extra yield. Those high duration bonds suffered the most from the regime of rising rates and resulted in huge impairment costs for the bank, who suffered a net loss of $1.05bn in the fourth quarter of last year. This will serve as a stark warning for any banks considering taking on crypto deposits and the next logical step is to look for banks that are already open to deposits from crypto firms.

Alternatives to Silvergate:

The flood of crypto deposits welcomed by Silvergate alongside the crypto boom is evidence of the glaring need for a crypto-friendly bank, and the focus now turns to which bank will accept crypto funds. The next friendliest for crypto is Signature Bank, who has (looking more like had) partnerships with many crypto companies, such as Coinbase and Kraken, but has publicly signaled their intentions to cut back on their crypto exposure. In its mid-quarter update, Signature showed its spot deposit balances through January and February were $826 million lower. However, the bank said the decrease was "driven by the deliberate decline in digital asset client related deposits of $1.51 billion."

In February, Signature extended its pullback and stopped handling transactions under $100,000, which led to Binance temporarily suspending USD transactions to and from the exchange. With Signature pulling back its exposure to the crypto industry, the next best contender will likely be a smaller bank raising their hand to take on the risk of crypto in search of a wave of new deposits.

Transacting with Stablecoins

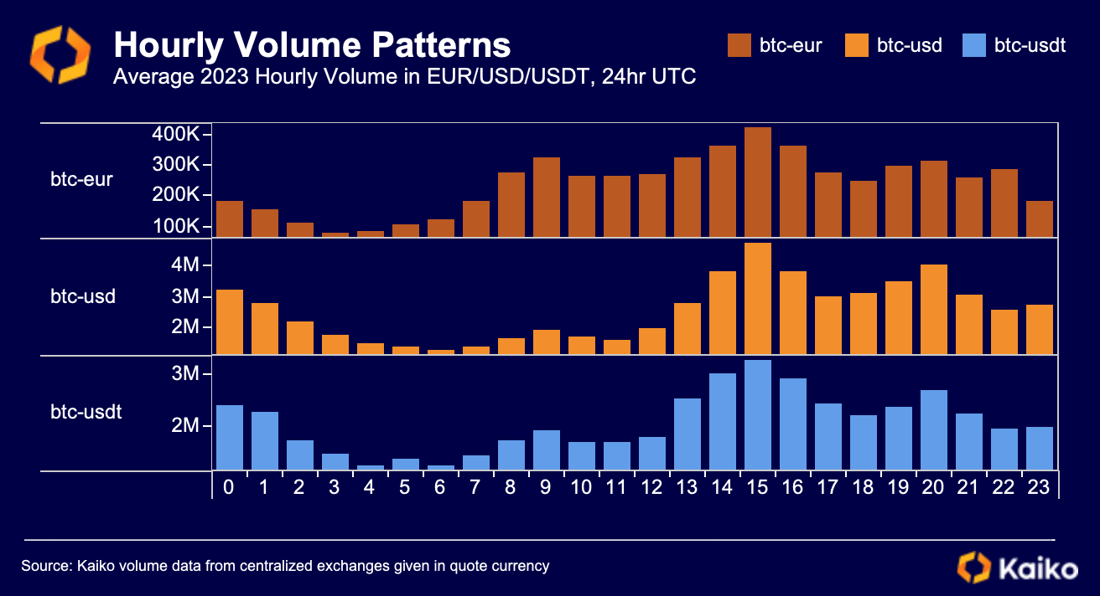

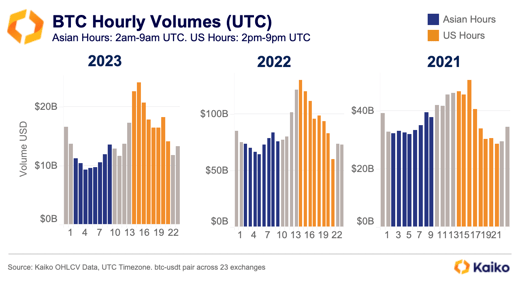

If no bank steps up, both crypto firms and crypto traders may have to look at other alternatives to USD in crypto. Given this worst case scenario, the industry has two options in my opinion. One is to transact via stablecoins. We know that US investors and crypto firms are comfortable using stablecoins, and that’s reflected in the data. When looking at volumes traded for USDT compared to EUR and USD markets, the trend for USDT most closely mirrors USD markets, i.e most high volume hours are during US trading hours.

Time for the Euro to Step Up

The other option provided US firms are cut off from banks is a relocation to avail of other fiat options such as the Euro.

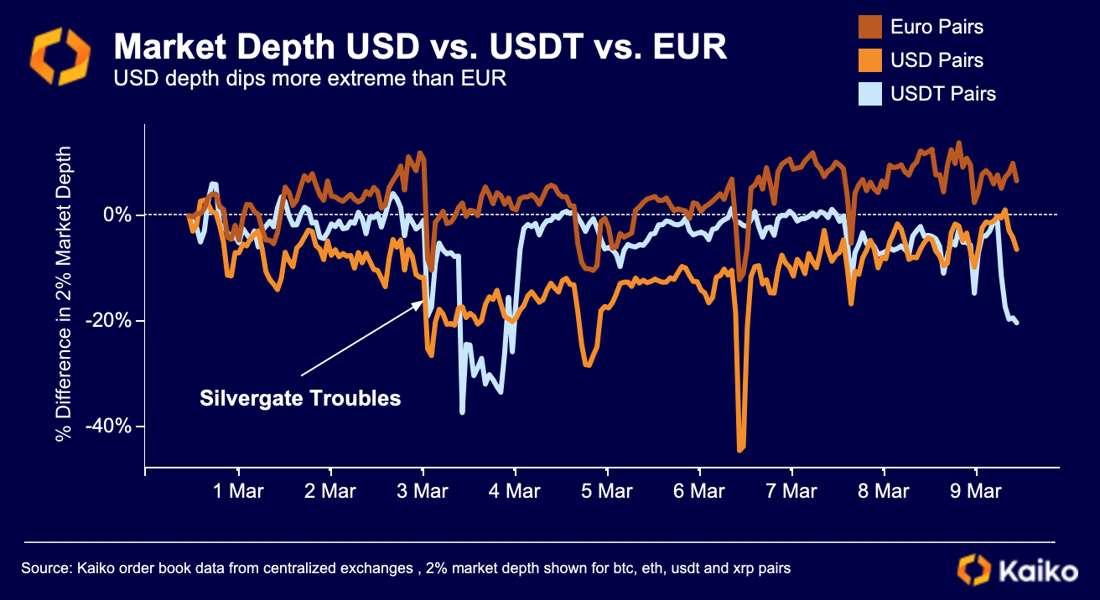

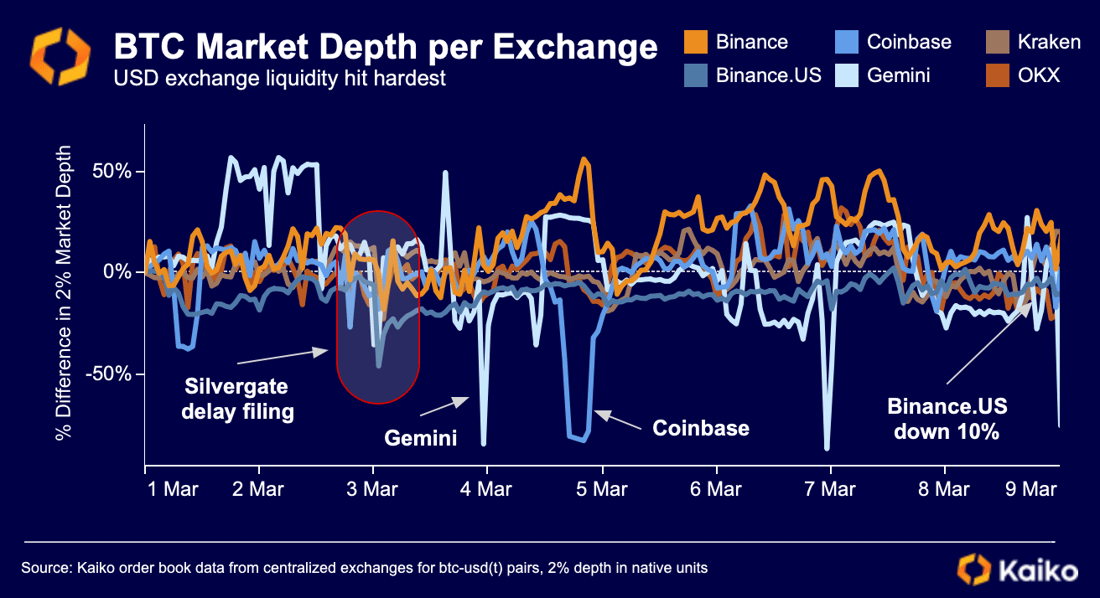

We can see those that provide liquidity to crypto markets were contemplating a USD vs. EUR decision in real time: there was a sudden dip in market depth for USD and USDT pairs, falling as much as 20% on March 3rd as Silvergate news hit the press. Meanwhile, market depth for Euro pairs remained steady as market makers for the Euro were less concerned about a change in market structure.

Liquidity was also hardest hit on some US-centric exchanges such as Binance.US and Gemini, whose market depth for BTC pairs dropped 8% and 19% respectively following the news, before recovering since.

With liquidity steady in Euro markets, and the US at a crossroads with regards to crypto banking access, there has never been a more opportune time for Europe to get a stronger foothold in the crypto market. There is also an instant settlement network for crypto firms present in Europe called the BCB Liquidity Interchange Network Consortium, or BLINC, that has served the euro, British Pound and Swiss Francs since mid-2020. Combine the ambiguity surrounding crypto banking in the U.S with the regulatory carpet bomb we’ve seen as of late, and the reasons for a crypto firm to stick in the U.S are becoming less and less compelling.

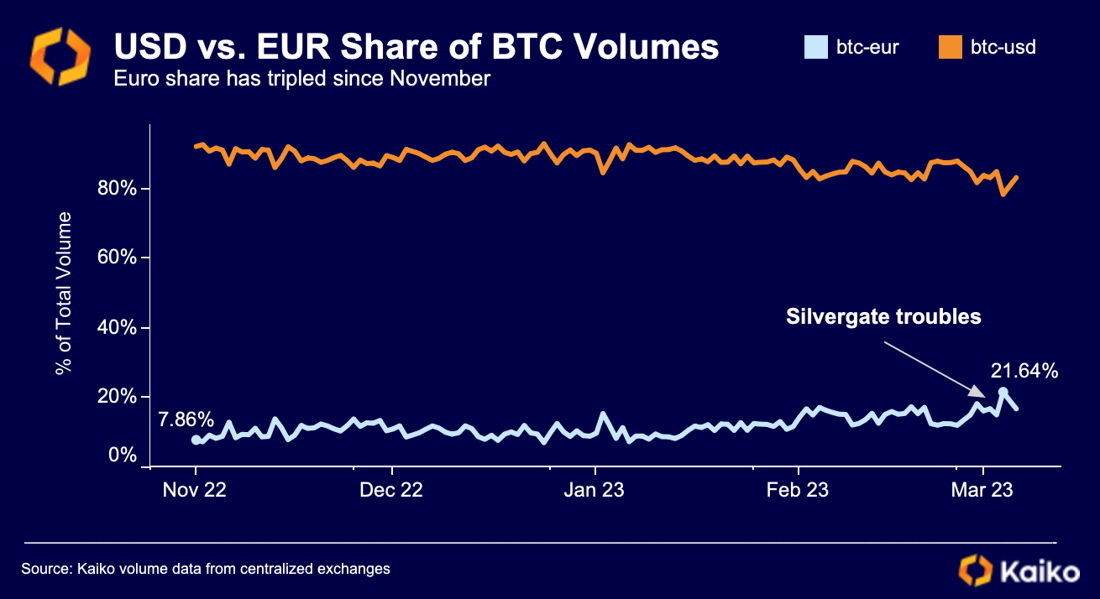

Early indicators are that in terms of trading volume, the Euro may be a big winner of a US crypto banking cutoff, with volumes spiking for the BTC-EUR pair as the Silvergate troubles ensued. The BTC-Euro pair hit its highest level of market share vs. the Dollar ever last week, nearly tripling in market share in the space of a few weeks.

Euro + Stablecoins = Euro Stablecoins?

Not only do Euro fiat pairs in crypto stand to benefit from a potential shift in market structure, but Euro stablecoins could be thrust into relevancy for the first time. For crypto’s almost entire existence, Euro stablecoins have struggled to take off for a couple of reasons. First, almost a decade of negative interest rates made it very unattractive for Euro stablecoin issuers to amass the Euro collateral needed for a top stablecoin, as they would be resigning themselves to losing money on interest. Second, there simply hasn’t been a demand for Euro stablecoins due to the US Dollar’s relative strength. As a European trader, the main reason for choosing a Euro stable would be to avoid FX risk in converting funds into the US Dollar. Well, the Dollar has been on a tear recently and anyone that has held US denominated investments has been thankful for the FX exposure, so the demand for a Euro stable simply hasn’t been there.

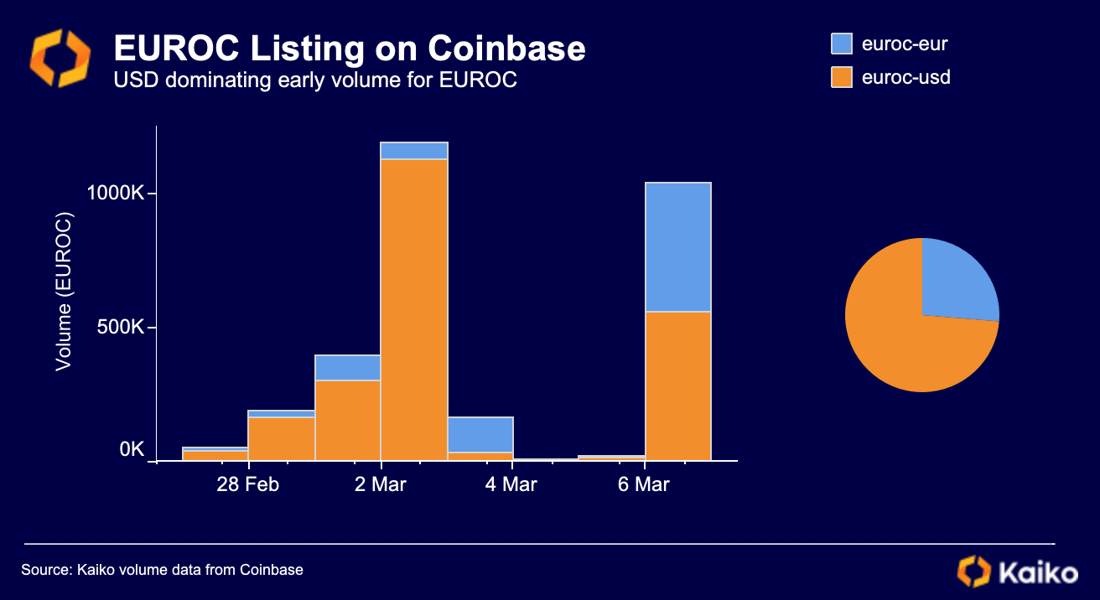

That could all change now as the crypto banking cutoff not only applies to US exchanges, but also stablecoin issuers. These stablecoin issuers will have to find a bank that is willing to take them on as customers or risk losing market share to their new European counterparts across the pond. One of the Euro stables that looks well positioned to capitalize is Euro Coin (EUROC), issued by Circle. EUROC was only launched in June 2022, and more importantly, was just listed by Coinbase at the end of February. Rather interestingly, early volumes for EUROC indicate that it is USD traders that are looking to gain exposure to the European stable, in what is perhaps a sign of things to come.

Conclusion

The problem with crypto banking is that the larger banks have a disincentive to offer services to crypto firms. To them, crypto money brings with it more trouble than it’s worth in the form of black swan events. Silvergate was a relatively small bank that outgrew itself thanks to being the best option for crypto firms and became overly concentrated in a volatile industry. Signature seems reluctant to make the same mistake, making efforts to limit their exposure to digital assets firms, leaving crypto firms scrambling for new alternatives.

Transacting in stablecoins is a very real possibility for some smaller businesses that can’t build a relationship with a bigger bank. Crypto native firms are the most familiar with stablecoins and they satisfy the 24/7 problem that the SEN network solved. The problem here being they require a greater level of trust in the stablecoin issuer than simply using USD. That’s assuming the larger stablecoin issuers won’t have an issue finding a new banking partner.

If crypto firms continue to be cut off from the banking system, for no apparent good reason, it’s highly likely that the more mobile companies will move elsewhere. It seems lately that there is a new headwind every day for US companies in the form of regulatory enforcement, and a struggle to get banked in the US could be the push they need to move elsewhere. With regulatory clarity in the form of MiCA, Europe looks well positioned to capitalize and Euro volumes are starting to show a renewed interest in the region.

Kaiko's research newsletter is written by the Kaiko research team: Clara Medalie, Dessislava Aubert, Riyad Carey, and Conor Ryder, CFA. This content is the property of Kaiko, its affiliates and licensors. Any use, reproduction or distribution is permitted only if ownership and source are expressly attributed to Kaiko. This content is for informational purposes only, does not constitute investment advice, and is not intended as an offer or solicitation for the purchase or sale of any financial instrument. For any questions, please email research@kaiko.com.